Online retail sales growth slowed in May following a fairly strong April

Insight

Bank of England has pledged to buy up to £5bn of longer dated gilts each day for up to 13 days (£65bn total) with a motive of protecting the UK pension industry.

One lesson we have learned overnight, after months during which markets have been forced to realise that there is no such thing as Fed (or other central bank) ‘put’ that will protect risk assets markets from their ‘all in’ mission to slay the (global) inflation dragon, is that when markets become dysfunctional with potential real world economic consequences, central banks’ financial stability obligations can still kick in

Such has been the case in the UK in the last 12 hours, little more than 24 hours after the Bank of England’s chiel economist Huw Pill claimed market were functioning normally and that what we were witnessing was “just an orderly repricing reflecting fundamentals. QT (quantitative tightening) can and should continue.”

As well as delaying the start of QT, the Bank of England has now pledged to buy up to £5bn of longer dated gilts each day for up to 13 days (£65bn total). The motive is to protect the UK pension industry, specifically that section still operating final salary pension schemes who utilise what are called ‘Liability Driven Investment’ (LDI) strategies and who hedge their future liability streams via long dated gilts. These are highly sensitive to large moves in longer dated yields, necessitating margin calls from these pension providers to meet their obligations to operators of such schemes (prompting those without sufficient liquidity on hand to be forced sellers of gilts).The FT quotes one London bankers as saying that ‘at one point on Wednesday morning there were no buyers of long-dated UK gilts’.

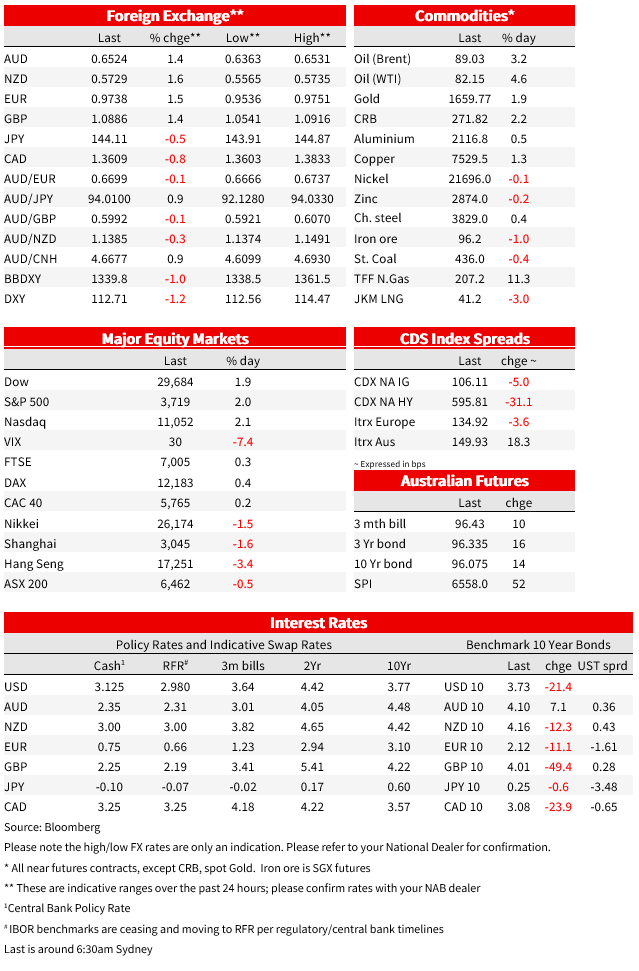

The impact of the BoEs announcement was to see the 30-year gilts yield fall from an earlier high of 5.12% to a low of 3.92% , a quite extraordinarily one-day move, in turn triggering a significant reversal in government bond yields globally. These have of course been under some quite intense pressure in recent days, contributory factors to which had been: 1) Last Thursday’s roughly ~$25bn BoJ FX intervention against USD/JPY (prompting fears of BoJ Treasury sales from FX reserves to fund future actions) and then 2). The market’s scathing response to last Friday’s UK mini-budget and attendant fear, in the absence of more information, for the deficit financing implications of what was described as the ‘biggest tax cuts since 1972’ – at a time when inflation is running in double digits.

Bond markets have seen the global bellwether 10-year US Note, that had punched above 4% in London trading yesterday morning for the first time since April 2010, drop back to around 3.70% (3.73% now) with 10-year gilts currently down 50bps on the day.

The US yield moves have prompted a more than full reversal of the selloff in US equity futures during our time zone yesterday, the latter in large part following news that Apple was abandoning plans to step up iPhone 14 production due to weaker demand. Apple shares have pared a near 5% opening NYSE loss to about -1.5%, both the S&P500 and NASDAQ closing with gains of 2%. Just reading about the potential devastation about to be wreaked on Florida now that Hurricane Ian has made landfall makes me wonder if this is justified? For now, other factors look to be completely subservient to a 25bps drop in 10-year US bond yields, plus a 12bps drop in the implied peak in the Fed Funds rate (now 4.42% in May next year from 4.54% on Tuesday). Fed put, anyone?

European equity markets have been much more restrained in comparison, the UK FTSE 100 up 0.3% on the day and Eurostoxx 50 0.30% Accusations of Russian sabotage of gas pipelines in the Baltic haven’t been helpful to the cause of EU stocks in this regard.

For FX , its been a case of the USD dropping back quite smartly under the combination of lower US yields and improved risk appetite – the two primary drivers of the USD’s almost relentless march higher in recent days (indeed weeks, months, and the past year). All G10 currencies bar CAD (+0.9%) and JPY (0.4%) are more than 1% up on this time yesterday, NZD/USD showing the biggest gain (1.6%) and AUD/USD up 1.4% to be back above 0.65 (high of 0.6522, versus a low of 0.6363 around yesterday’s Sydney close).

Economic news has been scant . The US goods trade deficit narrowed to $87.3b, its lowest in nearly a year, some $2b smaller than expected which will support the net exports contribution to Q3 GDP. Normal service was resumed on US housing market data, following yesterday’s positive surprise to new home sales, with pending home sales down 2% m/m in August, the ninth drop of the past ten months and now down 28% from the peak. Earlier, the GfK German Consumer Confidence reading dropped to -42.4 from -36.8, a record low and far below the prior My 2020) pandemic era low.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.