Coming in for landing in a heavy cross wind

Insight

Against the consensus view for an unchanged outcome, the BoE unexpectedly also raised rates by 15bps to 0.25%.

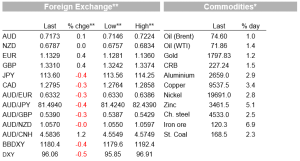

A day after the Fed, US equity investors are having second thoughts on what a gradual Fed tightening plan means for their investments, particularly big tech companies. The NASDAQ is leading the decline with major technology and internet shares under pressure while pro-growth sectors are up on the day. The ECB has an exit plan to avoid a brutal transition, increase the APP buying power first, then taper afterwards, meanwhile the BoE surprises the market, hiking by 15bps. The 5y tenor had lead a decline in UST yields with the USD broadly softer, AUD briefly trades above 72c, NZD tests 68c

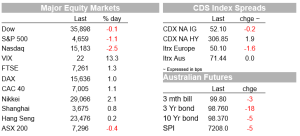

After recording handsome returns in the aftermath of the FOMC announcement yesterday, today we are seeing a big reversal in US big tech companies’ fortunes . As I type the NASDAQ is down -2.36%, more than reversing the 2.15% gains recorded in the previous day. A new Fed tightening cycle aimed at cooling the economy certainly provides food for thought for high growth stocks, then again this could just be related to squaring positions ahead of an end of the year holiday break. Of note, Apple is down close to 2%, Nvidia is -3% while Amazon and Microsoft are down around 1%. The S&P 500 is -1.15% with IT ( -3%) and Consumer Discretionary (-1.92%) more than offsetting gains in Financials (1.32%), Energy (0.89%) and Materials (1.08%). The industrial heavy Dow is flat (0.08%) while main European indices ended the day with gains just over 1%, largely reflecting catch up action from yesterdays post FOMC gains in the US.

It has been a busy night for European Central Banks with the ECB, BoE, Norges and SNB all delivering policy announcements overnight. As expected, the Norges Bank raised rates for the second time this cycle , now to 0.5%, noting that it will most likely hike again in March and there will be a gradual rise in policy in the coming years. Key rate now seen at 0.7% in Q2, 2022 and 0.92% in Q3, 2022. Meanwhile against the consensus view for an unchanged outcome, the BoE unexpectedly also raised rates by 15bps to 0.25%. Markets were only 33% or so priced for this outcome given concerning warnings from the UK government and scientific community on the spread of Omicron and the possible overwhelming of the NHS. In justifying the rate hike, Governor Bailey noted the UK had “a very tight labour market and…more persistent inflation pressures”, with inflation set to reach around 6% next year, much higher than the BoE’s previous 5% forecast. The Bank said further “modest” tightening was likely to be required over the coming years to hit its inflation target, although it acknowledged there were risks on both sides.

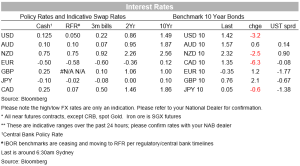

After a volatile session, UK gilts ended the day a couple of bps higher (10y @ 0.757%) with the market now pricing a UK cash rate just over 1% by November next year. GBP is currently at 1.3314, up 0.42% on the day, reversing earlier gains that saw the pair trade to an overnight high of 1.3374.

The ECB also surprised the market delivering news on the hawkish side . Ending PEPP in March was well expected, but the ECB also spelt out details of what happens to the APP QE program. While the amounts involved mesh with our own thoughts, we had suspected this detail could wait until the March meeting next year when there should be greater clarity on major uncertainties besieging the Europe, namely Omicron, Energy crisis and inflation outlook. In the event the APP (currently EUR20bn per month), will be raised to EUR40bn per month for Q1, dialled back to EUR30bn for Q3 and then back to EUR20bn for Q4 and continue until just before rate hikes become a consideration. In rationalising the temporary boost to the APP QE program before tapering, ECB President Lagarde justified the move as a step to avoid “a brutal transition.”

Notably for markets, the fact the ECB plans will be buying bonds throughout the whole of next year is a strong signal that it doesn’t expect to raise rates in 2022, as markets had recently been speculating. The ECB also said it would be more flexible with reinvestments of its pandemic bond holdings (i.e. giving it the option to skew reinvestments towards vulnerable countries like Greece) if markets came under stress again. European bond rates are higher overnight, by between 1bps for Germany and 5bps for Italy, although most of these moves occurred in response to the Bank of England’s surprise rate hike rather than the ECB’s announcements. Italian 10-year bonds, which have been a key beneficiary of the ECB’s bond buying, are trading around 130bps above Germany, which is close to its highest spread in 18 months. The EUR initially jumped after the ECB decision, before reversing those gains to be back at 1.1320.

Looking at the FX market over the past 24 hours, the USD has extended its post FOMC decline with European currencies the main beneficiaries. ECB and BoE hawkish tilts helping, but it hard to see these moves extending too far. The US economy continues to perform strongly and concerns over the Europe and UK energy supply are a big headwind, in addition to political uncertainties including UK-EU post Brexit and EU-Russia. On the latter worth noting that overnight the German regulator repeated that no decision will be made on Nordstream 2 in 1h ’22, just as the European weather is set to turn colder, there is no letup in Europe’s energy crisis. Nat Gas pushed on to new all-time highs again overnight.

The lift to EU currencies helped the AUD briefly trade above the 72c while NZD also spent a little bit of time above 68c. Later in the NY session, however, with big tech weighing on US equity indices, both antipodean currencies have lost some altitude, AUD now trades at 0.7169 and NZD is at 0.6785.

UST yields are lower across the curve with the 5y tenor leading the declines, down 7bps to 1.173%, the 2-year rate is down about 4bps from its levels yesterday morning, at 0.62%, while the 10-year rate is down 4bps, to 1.42%.

US data releases overnight were mixed and do not necessarily justified the decline in UST yields. November housing starts jumped by 11.8% to 1,679K from 1,502K, well above the consensus, 1,567K. Building permits rose 3.6% to 1,712K from 1,653K, above the consensus, 1,661K. But in contrast, the December Philly Fed index fell to 15.4 from 39.0, well below the consensus, 29.1 and jobless claims remained at very low levels ( 200k) with firms reluctant to let go of staff amidst an extremely tight labour market.

In Europe, the reimposition of Covid-related restrictions saw the Services PMI fall by more than expected, to an 8-month low of 53.3. Manufacturing remains a bright spot (being less affected by Covid restrictions), with the Manufacturing PMI sitting at a still lofty 58. Pricing gauges in the PMIs eased, albeit to still very high levels, indicating continued inflation pressures

Finally, after approving the largest US military budget in history, nearly $770 billion on Wednesday, Senate Democrats are abandoning efforts to pass President Joe Biden’s $2 trillion economic agenda this year, delivering a political blow to the White House, exposing the intra-party divide on the legislation, which many Democrats consider key heading into the 2022 mid-term elections.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.