Total spending grew 0.9% in June.

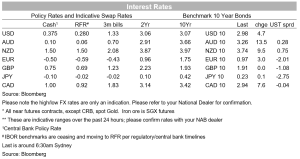

US 10-year Treasuries have just breached the psychological 3% barrier for the first time since late November 2018 in what has been a further bear steepening of the US curve

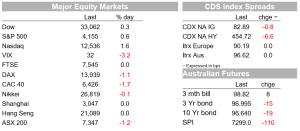

Markets have been holiday-impacted at the start of the new week (China, Hong Kong and the UK out Monday – and China and Japan again today and tomorrow). Continental Europe has played some catch up to Friday’s sharp US equity market falls most of which came after the European market close. Losses were exaggerated early in the day by an 8% ‘flash crash’ in the Sweden, for which a major US bank has been fingered as being responsible, but losses in Sweden and their spill-over impacts on broader European market has been fully reversed. US 10-year Treasuries have just breached the psychological 3% barrier for the first time since late November 2018 in what has been a further bear steepening of the US curve. US stocks have pulled up in the last ‘hour of power’ to finish in the green, while the USD has risen but remains just below last Thursday’s highs in DXY terms. AUD is little changed. The US manufacturing ISM shows the first signs of weakness emanating from earlier falls in China’s PMIs and related supply chain disruptions.

Ahead of the RBA this afternoon and a generally expected fifteen basis point rise in the Cash Rate to 0.25% in what would be the first tightening of RBA policy since 2010, offshore markets have started the week in mixed fashion. London has been out for the May Day bank holiday but continental European bourses all finished lower, by between 1.5% and 2%. Losses earlier in the day were compounded by an 8% ‘flash crash’ in the Swedish stock market , for which Bloomberg has named a major US bank as being responsible. The loss was quickly reversed, but of some note to this scribe is that the move followed the first lift in the Swedish Riksbank’ s policy rate since before the pandemic, last Thursday. Most of the ‘flash’ crashes in years past, be it (in currency markets) GBP, CHF, NZD or JPY, have had some prior fundamental catalyst that has pointed in the same direction as the ‘flash’ moves (e.g. Brexit referendum, SNB break of the CHF peg, an Apple profits warning that triggered a safe haven bid for the JPY, etc). Then the proverbial ‘fat finger’ has kept the buy/sell button stock down longer than intended, or buying/selling has hit a liquidity flat spot.

I digress. Of note, the last ‘hour of power’ has seen US market turn an early-day ~2% loss for the S&P500 transformed into a 0.6% gains, and a 1% loss for the NASDAQ into a 1.6% rise. There is no obvious news flow behind the turnaround. In fact, one might have expected the breach of the 3% level for 10-year Treasuries in the last hour of NYSE trade (high of 3.01%) to have had its biggest impact on the tech.sector/growth stocks. That has evidently not been the case.

There is also no obvious ‘new news’ reason behind the further ‘bear steepening’ of the US yield curve (2-year Treasuries currently +2bps and 10s +5bps. Certainly the incoming US data if anything pointed the other way. The US ISM manufacturing Index came in well below expectations at 55.4 from 57.1 (57.6 expected) with both the Prices Paid (84.6 from 87.1) and Employment (50.9 from 56.3) sub-series weaker. Of note here is that regional PMIs, which pointed to a steady-to-firmer ISM reading do not, as our friends at Pantheon Economics point out, capture that part of the United States west of the Rocky Mountains. This is where the rubber first hits the road as far as China-US seaborne trade is concerned (in both directions) offering the first hint that the sharp slowing in China PMI readings in March and April due to the lockdowns in Shanghai and other parts of China before that are (just) starting to bite, consistent with the historical 2-3 months lag from China to US/global manufacturing PMIs. Other US data included weaker than expected Construction Spending, up just 0.1% against 0.8% expected.

In Europe , we had some eye-opening weakness in German retail sales to kick off their day (-5.4% year-on-year in March from +6.8% in February) followed by across-the board slippage in the various European Commission sentiment surveys covering Economic, Industrial, Services and Consumer Confidence, albeit lesser falls than we saw in March and which captured the first full month of the Ukraine war. On the latter, it is evident that EU countries are still struggling to form a (unanimous) consensus about embargoing energy supplies from Russa. Hungary is currently opposed to any embargo, while Germany is reportedly opposed to any gas embargo while supportive of plans to phase out dependence on Russian oil before year-end. Oil and gas prices haven’t moved a whole lot in Europe or the US markets. Final Eurozone manufacturing PMIs saw the pan-Eurozone index revised to 55,.5 from 55.3.

In FX, the USD has edged ahead once more but at 103.7 is still just shy of last Thursday’s 103.9 high. Losses for the EUR (-0.4%), JPY (-0.4%) and GBP (-0.7%) the latter giving back Friday’s somewhat curious rally, have driven the USD gains. AUD/USD has fared better than all other G10 currencies, albeit it is still down on Friday night’s close, at about 0.7050, playing to the view there may have been a month-end rebalancing impact slightly exaggerating the scale of Friday’s losses.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.