Long-term signal vs. Short-term noise

Insight

Another big UK fiscal U-turn and positive earnings from BofA boosted global risk appetite last night.

Another big UK fiscal U-turn and positive earnings from BofA boosted global risk appetite last night. The UK’s new Chancellor wasted no time in reversing the ill-fated mini-Budget, scrapping £32bn of unfunded tax cuts, re-designing the energy support package to make it more targeted from April 2023, as well as flagging possible savings measures in the upcoming Budget on 31 October. Given such a wholesale scrapping of PM Truss’ Tory leadership promises, it remains an open question how long PM Truss will remain in power. Latest polls have the Labour opposition leading by a record 36 points and at least five Conversative MPs have publicly called on the PM to resign.

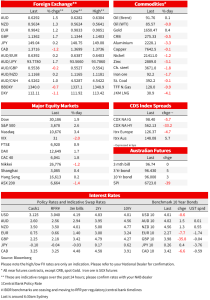

Markets reacted favourably to the U-turn with Gilt yields plunging; the 10yr yield fell -35.6bps to 3.98%. Terminal BoE pricing has also fallen given reduced inflationary pressures and a rising GBP with the peak bank rate now priced at 5.15% from 5.64% on Friday and well down from the 6¼% seen when the mini-Budget was first announced. GBP leaped, up 1.6% to 1.1349, shadowing the move in yields and it is worth noting the 21-day rolling correlation between GBP and Gilt yields is 0.69, its highest since 2020. The next two crucial dates for the UK are 31 October when the Budget is released, the same date as when the BoE was scheduled to start QT which has been already postponed, and then to the BoE MPC meeting on 3 November where markets are nearly fully priced for a 100bp rate hike. As an aside note the temporary expanded repo facility continues until 10 November, and the BoE also intends on resuming its corporate bond sales next week.

Developments in the UK spilled over to other markets with key European 10-year rates down about 8-9bps; the German 10yr yield was -7.7bps to 2.27%. In the US moves in Treasury yields have been volatile, first heading lower on the UK to reach as low as 3.91%, then reversing as the risk-on rally got underway with the US 10yr ending broadly unchanged at 4.01%. US Fed Funds pricing was little changed (peak of 4.9% by March 2023) with much of the reversal due to the surge in US equities with the S&P500 up 2.6% along with an even sharper move of 3.4% for the tech-heavy NASDAQ.

BofA reported better than expected earnings with its stock up 6.1% (EPS 81 cents vs. 77 cents expected), while some equity strategists noted the very bearish positioning in the lead up to the earning season which could lead to another technical rally akin to what we saw during Q2 earnings in the short term with the 200day moving average in the S&P500 a key level (4,155 vs. today’s close of 3,678). As for BofA’s results, they highlighted a resilient consumer with CEO Moynihan noting: “our U.S. consumer clients remained resilient with strong, although slower growing, spending levels and still maintained elevated deposit amounts ”. Credit card delinquencies were also cited as being below pre-pandemic levels, while NIMs widened to 2.06% from 1.86%, and was a little higher than the 2.0% expected.

In FX, positive risk sentiment has seen the USD weaken against most majors apart from JPY. Gains unsurprisingly were led by GBP as noted above, shadowing the move in Gilt yields, with GBP +1.6% to 1.1349, not far off its pre-mini Budget level of 1.15 and well off the lows seen at the height of the drama when it looked like it was going to submerge below parity. USD/Yen was +0.2% to 148.95, a fresh 32-year high with BoJ rhetoric meaning the only way is up until it is interrupted by the next round of FX intervention. Many are noting 150 as a key psychological level that the government will be keen to avoid a sustained break of, for political reasons. Other major FX reflected the more positive sentiment with AUD +1.4% to 0.6285, NZD +1.1% to 0.5625, and EUR +1.2% to 0.9834.

As for economic data it was sparse and not market moving. The US NY Empire Manufacturing Survey disappointed at -9.1 vs. -4.3 expected. There wasn’t much in key developments in the report with details noting little change in new orders, unfilled orders, or shipments. Inventories did inch a little higher and on the prices side, input prices picked up, but selling prices held steady. North of the border the BoC’s latest consumer and business surveys saw still very strong inflation expectations, firming up another 50 or 75bp hike at the next meeting.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.