Online retail sales growth slowed in May following a fairly strong April

Insight

The US Fed has extended its QE shopping list, agreeing to buy junk bonds from corporations suffering the impacts of the coronavirus.

https://soundcloud.com/user-291029717/buying-junk-and-cutting-oil?in=user-291029717/sets/the-morning-call

A 2006 Buzzcocks song, in case you’re wondering, said by songwriter Pete Shelley to have been inspired by watching a business TV channel talking about credit, “people being in debt from buying stuff they don’t want and the ‘video phones with all the latest ring tones.'”

The most influential market news event since Australia broke for the Easter holidays on Thursday has been the Fed’s announcement, prior to Thursday’s NYSE open, that it will be henceforth be willing to buy not only investment grade credit – directly or via ETFs – as part of its unfolding QE bond buying programme, but also high yield or sub-investment grade paper. This is providing that any such paper was investment grade as of March 20 and has not since been downgraded to more than three notches below (i.e., it has to be Ba3/BB- or better versus the Baa3/BBB- lowest investment grade, in Moody’s and S&P parlance respectively). In conjunction with this, the Fed unveiled plans, totalling some $2.3tn., to provide cheap financing for SMEs and to purchase the debt of state and local authorities (‘Munis’) as well as Collateralised Loan Obligations – remember those during the GFC? – and commercial MBS.

The impact of the Fed announcement was to push up the iShares iBoxx $ High Yield ETF by 6.6% and the iShares investment grade bond ETF by 4.7%. The S&P rose by 2.2% in the first hour of NYSE trade following the announcement and held most of the gains through Thursday’s session (stocks were closed Friday). This brought the S&P rally since its 23 March low to 26% and the index to just 17.6% below its 19 February peak. Overnight though, and with the Q1 corporate earnings season about to kick off, a little of last week’s ebullience has worn off, the S&P just closing down 1% and the Dow -1.4% (NASDAQ is up though, by 0.5% thanks to a 6% jump in Amazon).

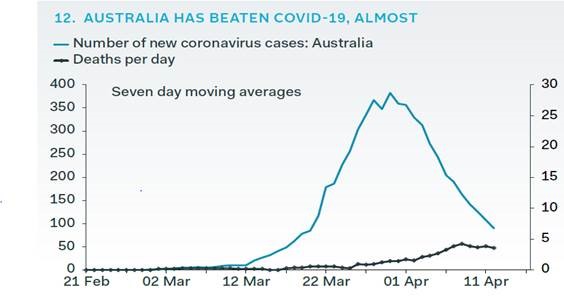

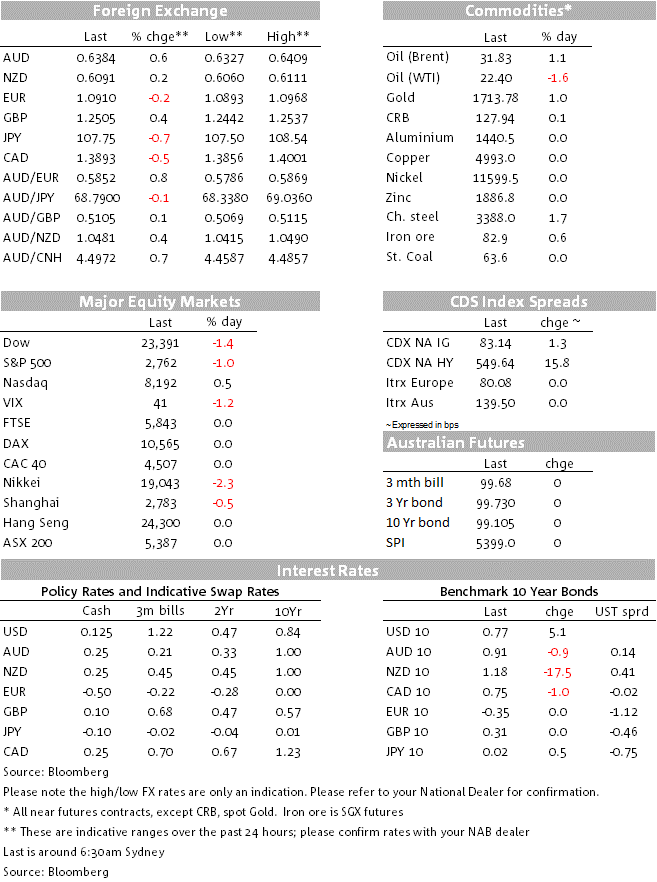

The further boost to risk sentiment brought on by the Fed announcements saw the USD lower and the AUD smartly higher Thursday, initially up to the 0.63 level and later to the 0.6350 area, making it the standout winner in the G10 currency stakes. Gains held through Friday’s holiday-thinned session and have now extended, AUD/USD up another 0.7% to a high of 0.6409 (0.6390 now). As well as being the antipole of the USD – now 4% off its 23 March peak in BBDXY terms – AUD outperformance since late last week arguably also owes something to the fact Australia’s COVID-19 curves have bent downwards more sharply than just about any country outside China and which is getting plenty of international attention (e.g. see Chart of the Day below)

The oil market was, initially, moderately impressed back by the pact struck between the 23-member OPEC+ cartel to withdraw 9.7 million barrels from daily production from 1 May, with the US, Canada , Brazil and other G20 producer nations set to withdraw between 4 and 5 million barrels of daily production, largely through market forces that naturally reduces the amount of oil than can be profitability produced. As part of the broader “market forces” curtailment, the US offered a 300,000 barrel reduction to placate OPEC+ in order to make up for Mexico’s refusal to cut by more than 100,000 barrels, 300,000 barrels short of what Saudi Arabia had wanted.

Saudi’s energy minister yesterday claimed that the effective OPEC+ cuts would be 12.5 million barrels, reflective of the fact Saudi Arabia, Russia, etc al, are currently producing above the benchmark production levels from which the 9.7 million barrels cut have been agreed (e.g. Saudi Arabia is believed to be currently producing around 12.3 million bpd against the 11 million pre-March production quota allotted to both it and Russia ). President Trump has been in the Twittersphere claiming the true cut will be more like 20 million barrels, a view not currently gaining much traction.

In the face of the estimated +/-30 million barrels daily demand destruction since COVID-19 lockdowns came into effect in many of the world’s major oil consuming nations, the oil market was nonplussed at Monday’s open, initially taking prices higher, then sharply lower before recovering to about $2 above Friday’s ~$31 closing price for the Brent benchmark but which is almost exactly where it now sits ($32.04).

Other significant news since last Thursday was the Eurozone rescue deal agreed by EU Finance Ministers late on Friday, but which according to the FT has triggered a political storm as a result of Italian Finance Minister Roberto Gualtieri willingness to sign up to the EUR500bn deal which has its centrepiece the use of the European Stabilisation mechanism (ESM) albeit without the tough macroeconomic conditions earlier demanded by the Netherlands in particular, with no explicit mention of the coronabonds as desired by Italy, Spain, et al. The compromise agreed by Gualtieri has been condemned by the opposition League party of Matteo Salvini who denounced the minister as a traitor, but also the Five Star Movement, which currently shares power with the centre-left Democratic party of which Gualtieri is a member.

The core elements of the package are the Pandemic Crisis Support Fund to be made available from the ESM within two weeks, a boost to the lending capacity of the European Investment Bank (EIB) and a new EUR100bn unemployment insurance scheme as proposed by the European Commission. The higher EUR/USD level since we left work Thursday (or rather shifted to another room at home) is all the result of the weaker USD following the aforementioned Fed news. The single currency has since given back a little of these gains in holiday thinned Monday trade, to 1.0913.

Ahead of this Friday’s China Q1 GDP and March activity readings, the PBoC on Friday reported March credit and money supply data. The broadest Aggregate Financing measures (a combination of bank lending in all its guises and local government bond financing) jumped by CNY5.15tn. after just 855bn in February, well above the 3.14tn. expected with New Yuan Loans up 2.85tn, above the 1.8tn median forecast. M2 money supply growth also jumped, to 10.1% from 8.8% in February and 8.8% expected. These are positive omens in terms of China having sufficient credit to both get back to work and in the case of local government financing, for new infrastructure activity.

Also out Friday were China inflation data showing a fall in headline inflation to 4.3% from 5.3% in February, largely thanks to lower food prices (we estimate a 0.4% seasonally adjusted fall on the month). Core inflation is put at just 1.1%, well beneath the 3% CPI target, and producer price inflation now -1.6% from 0.4% previously. US CPI also undershot expectation on Friday, headline coming in at -0.4% on the month (-0.3% expected) and the core (ex-food and energy) measure -0.1% vs. +0.1% expected. Notwithstanding all manner of measurement challenges with inflation data, given some services simply aren’t being produced, the China and US numbers are telling us that, for now, the pandemic is a disinflationary if not outright deflationary economic force.

The start of the Q1 earnings season and associated forward guidance (if any) and China Q1 GDP and March activity data are the standouts this week, alongside – of course – ongoing COVID-19 curve-watching and analysis

Bank results should be slightly less interesting than non-financial companies this week, though for the record JP Morgan and Wells Fargo report today and BofA, Citigroup, Goldman Sachs and Morgan Stanley on Wednesday. United Airline and Johnson & Johnson are of note today, and names such as Las Vegas Sands and Bed Bath and Beyond (both tomorrow) will be scrutinised, being among the pillars of the gambling and household goods retailing sectors.

China releases March trade data later today (17:00 AET according to Bloomberg) and Friday brings Q1 GDP, expected to have contracted by 11.2% QoQ according to the Bloomberg survey median. The March activity readings should show improvement on February as factories got back into action and shops re-opened, with industrial production seen at -9.9% YTD Y/Y up from -13.5% in February and Retail Sales seen improving to -12.5% YTD Y/Y from -20.5% previously.

Unemployment (Thursday) should rise sharply in March as COVID-19 started to hit the labour market. NAB forecasts the unemployment rate to rise to 5.7% from 5.1%, well above the consensus estimate of 5.4%, with employment falling by 90k. Unemployment should rise much further in April given tougher containment measures were introduced from mid-March. The NAB business survey is published today and will show the impact of COVID-19 restrictions on business confidence and conditions.

Source: Pantheon Economics

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.