On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

There’s more caution in the markets today, even though numbers out of Australia, the US and China were better than expected. There’s a bit of battle fatigue hitting the market says NAB’s David de Garis.

https://soundcloud.com/user-291029717/cautious-for-no-clear-reason?in=user-291029717/sets/the-morning-call

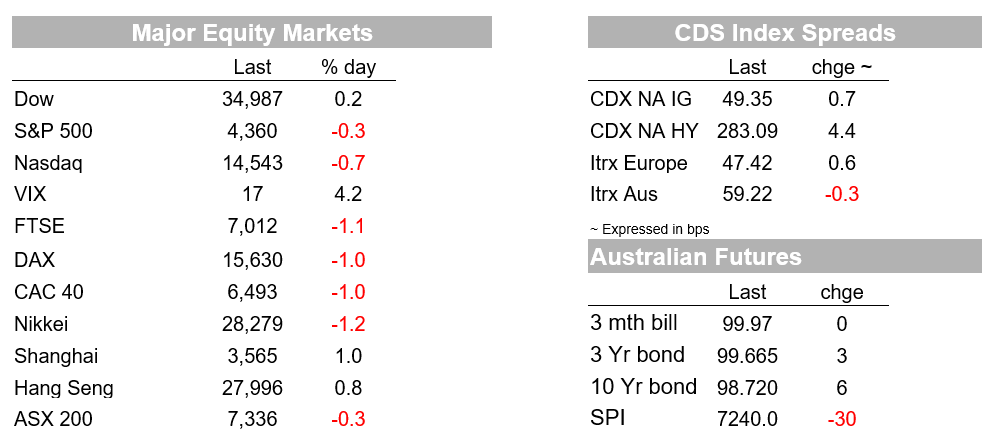

A risk-off tone in markets overnight with no obvious catalyst to explain the fall in equities (S&P500 -0.3%), or the fall in yields. The US 10yr yield fell 5bps and broke through 1.30% to a low of 1.2906 and trades at 1.3006. There was no top-tier data with US Jobless Claims broadly in line (360k v. 350 expected), while the regional manufacturing surveys gave contrasting views with the NY Empire at a record high (43.0 v. 18 expected) and the Philly Fed dipping back (21.9 v. 28.0 expected). There was some very large corporate issuance flows following the US banks’ profit reporting with Morgan Stanley ($8.5bn) and BofAML ($7.75bn) headlining and coming after Goldman’s $5.5bn on Wednesday – such issuance may have contributed to the move in yields via hedging flows. Chair Powell also spoke to the Senate, but was a repeat his dovish testimony to the House.

Outside of issuance and Powell, three cautious narratives also appear to be getting some airplay. The first is that the delta variant may push back the global recovery, secondly global growth is slowing as we move into the recovery phase, and lastly some central banks may mistakenly tighten policy too early. Your scribe can also add to that more evidence that the lift in inflation is likely to prove transitory. TMSC, the world’s largest contract chip marker, expects chip shortages in the auto industry to ease in the next few months as it ramps up its production. These narratives of course can’t be linked to any specific market move, but it is worth noting that a softening of the positive narrative has occurred since mid-2021 after the re-opening/reflation theme since late 2020. One area where this is evident is the Russell 2000 which is down 7.2% since its peak in mid-March.

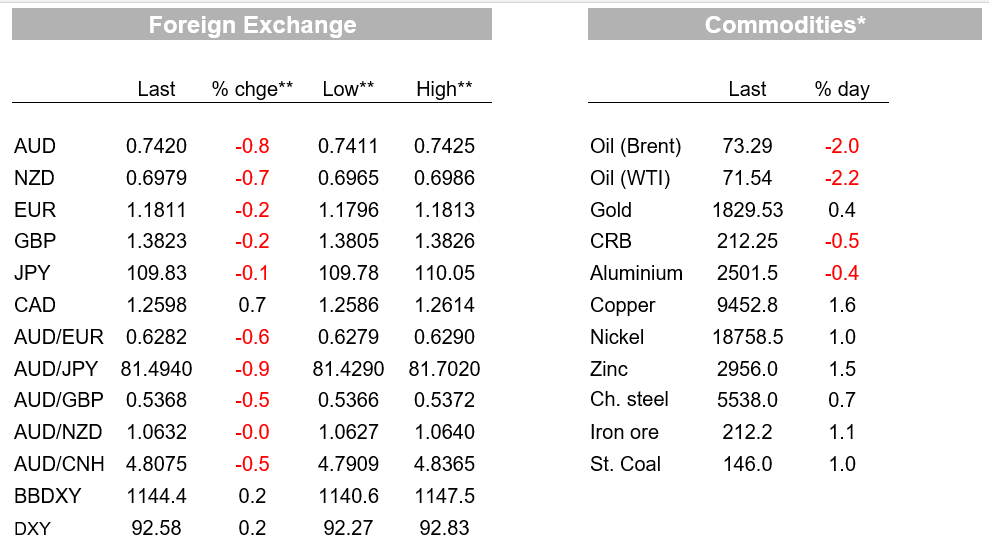

The risk off tone was evident in FX with commodity currencies coming under pressure. A 2% fall in Brent Oil was also a factor coming on the back of renewed OPEC uncertainty. The AUD is currently trading at 74.22, having fallen 0.8% overnight and the technical are not pretty with not much air between 74 and 73 on the charts. The Aussie ignored the better than expected jobs figures yesterday with an eye towards the Sydney lockdown extending to Melbourne. Tellingly of the tone AUD/YEN was down a more sharp -1.0% with JPY rallying (USD/YEN -0.2%). The NZD also felt the chill, down a similar 0.8% to trade close to where it was prior to the hawkish RBNZ meeting earlier in the week, and coming ahead of NZ’s Q2 CPI later today. The largest underperformer overnight though was USD/NOK which rose 1.1%. In contrast the USD was more steady with BBDXY up a more mild 0.3% with EUR -0.2%, GBP -0.2%.

Central bank speak was mixed, but reinforced the dovish messaging from the Fed. US Fed Chair Powell gave his second round of Testimony, this time to the Senate. As you would expect, most of the commentary was pretty similar to that given to the House. Instead, the most insightful commentary came from the Fed’s Evans who said it will take “more than a couple of months” to sort out the timing on tapering and that “given the more recent months of lower employment growth than I was expecting, I would say that there are still things to assess in terms of substantial further progress that needs to be met for us to make adjustments in our monetary policy stance”. Both Powell and Evans noted the Fed was monitoring inflation, including the risk that it could prove longer lasting and seep into inflation expectations, though both repeated the transitory line.

On the ‘transitory’ theme, your scribe thought the statements by TSMC of chip shortages abating this quarter particularly interesting. TSMC is the world’s largest contract chip maker and stated yesterday on an earnings call that it expects chip shortages that have hampered car production to ease in the next few months after it ramps up its production of chips. The broader semi-conductor shortage though could persist until 2022 (see WSJ article for details). If new car production comes back online, then that should see the significant ramp up in used car prices starting to ease, and could potentially weigh sharply on US CPI in the coming quarters given used car prices accounting for around half of the increase in core CPI in June.

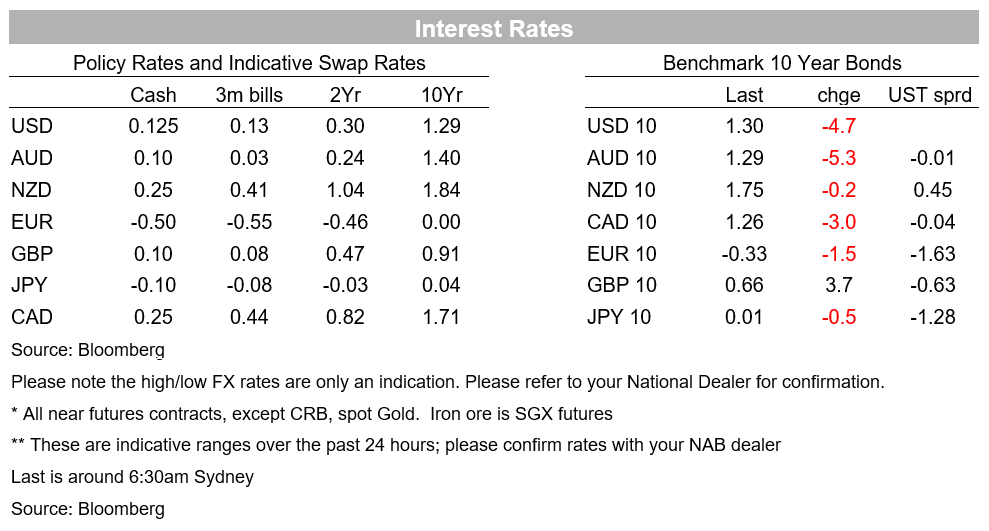

Across the pond in the UK, BoE MPC member Saunders came out on the hawkish side, supporting an earlier tightening of monetary policy. It is worth noting that Saunders had been one of the more dovish voices on the MPC and this time switched hawkish: “For me, the question of whether to curtail our current asset purchase program early will be under consideration at our forthcoming meetings” and beyond that rate rises next year (“and/or further monetary policy action next year.”). Saunders characterised such tightening as “ more akin to easing off the accelerator rather than applying the brakes”. His remarks came in the wake of UK CPI on Wednesday printing at 2.3% for core, which is above the 2% target. Saunders comments echo similar messages from fellow MPC member Ramsden yesterday, though Governor Bailey remains more dovish.

Saunders comments led to a sharp repricing of BoE rate hike expectations, with the market bringing forward the expected timing of the first 25bp rate hike to mid next year. The UK 2-year bond yield increased 6bps, to 0.13%, while the GBP immediately gained 0.5% in the wake of the comments, before later reversing. The market ignored a weaker than expected UK labour market report for May, which revealed slower than expected job growth and a tick up in the unemployment rate, to 4.8%.

Chinese annual GDP growth came in slightly lower than expected, at 7.9% (8% expected), although quarterly growth increased to 1.3% in Q2 from a revised 0.4% in Q1. Monthly Chinese activity data for June was also better than expected, with upside surprises across industrial production, fixed asset investment and retail sales data, the latter an encouraging sign as the economy starts to rotate towards a consumption-led recovery. Still, markets appear wary of a slowdown in Chinese growth, with the recent RRR cut by the PBoC seen by some market participants as validating this theory.

As for the Delta strain, the UK is being watched closely to see whether the link between new cases and hospitalisations has been broken due to higher vaccination rates. So far the evidence does suggests there has been a severe weakening, though there is likely to be a re-opening wave of hospitalisations amongst those who are not vaccinated (so far 67.1% of the population is fully vaccinated) and amongst those who are fully vaccinated but have severe underlying health problems. The recovery in emerging markets though may need to be pushed back with the Delta variant sweeping through populations with low vaccination penetration.

In Australia, Melbourne has followed Sydney into a lockdown after Victorian Premier Andrew declared a 5 day lockdown following a number of COVID-19 cases. With Sydney in lockdown until at least July 30 and now Melbourne in lockdown for at least 5 days, Q3 GDP is shaping up to be firmly negative. NAB’s base case remains that given government support, activity should rebound sharply once virus control is achieved and lockdown restrictions are eased. Unfortunately the risk of lockdowns will remain a feature of the near-term given Australia’s relatively low vaccination rate (9.4% of the adult population are fully vaccinated) with state premiers nominating a 70-80% vaccination rate as being required for Australia to move from aggressive suppression of the virus to living with it. On NAB’s calculations, we think it is plausible 80% vaccination can be achieved by late November. More specific vaccination thresholds are currently being calibrated by the Federal Government.

Finally, yesterday’s Australian employment numbers were not market moving despite the upward surprise given the virus news. The data though does confirm the labour market continued to improve ahead of Sydney’s protracted lockdown, even with Melbourne’s two week lockdown weighing. Headline employment was +29k after last month’s incredibly strong +115.2k (consensus +20k), and the level of employment is now 1.2% above pre-pandemic February 2020 levels. Unemployment also fell to 4.9% from 5.1% (consensus 5.1%) and is at its lowest level since December 2010. Beneath the surface, Melbourne’s two week lockdown clearly weighed with hours worked falling a sharp 8.4% m/m in Victoria compared to a 0.5% rise nationally when excluding Victoria. Victorian employment fell just 0.3%, considerably less than the fall in hours worked.

There is no data domestically, but eyes will still be on developments across the ditch with NZ having their Q2 CPI figures. Some of the NZ CPI components map directly to Australian CPI given many companies operate on both sides of the Tasman with similar pricing strategies. Offshore the focus will be first on the BoJ meeting (no change) and then to the US with Retail Sales and Consumer Confidence. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.