On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

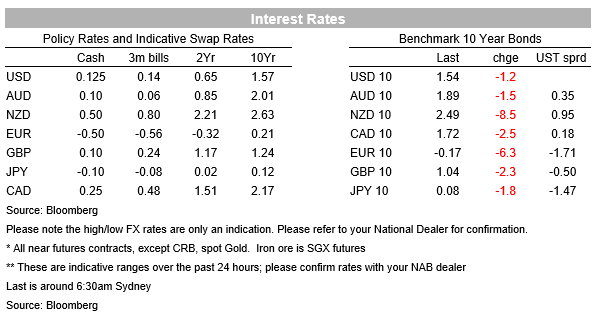

Global yields fall at the short end in the wake of the RBA’s dovishness yesterday.

The RBA tried to be dovish yesterday. At some level that worked with the implied yield on 3yr futures down 17.5bps since 2.30pm yesterday. However, markets still price around four hikes in 2022 with the Dec-22 cash rate future having a yield of 1.06%, only marginally down from 1.14% on Monday. That of course is in sharp contrast with Governor Lowe’s remarks of hikes in 2022 being “extremely unlikely ” with the next wages print on November 17 likely key to a further unwind in market pricing. As for moves overnight it was relatively quiet. There was a rally at the global front end which many attributed to flow through from the dovish RBA sentiment ahead of the US Fed tonight and BoE tomorrow – could they be not as hawkish as markets had feared? The US 2yr yield fell -4.5bps to 0.45% while the 10yr has been little changed at -0.7bps to 1.55%. The rally has been more pronounced in Europe with Italian 2yr yields -16.6bps to -0.21% and German 2yr yields -6.2bps to -0.68%. Fed Funds pricing has pushed back a little with a rate hike now fully priced in July 2022 and two hikes priced by the end of 2022. A taper announcement is widely expected of $15bn a month ($10bn Treasuries / $5bn MBS) but the focus is likely to be more on concerns around inflation.

Global risk sentiment overall continues to be supported despite more concerning headlines in China (more on that below). The S&P500 rose 0.3% with a stellar earnings season again supporting. Across the pond the Eurostoxx50 was up 0.4%. Strong earnings continue to sustain the rally with notable names overnight including Under Armour (+17%) with very strong earnings beat and DuPont (+8.8%) reporting strong demand and pricing power with plans to increase prices in Q4 in line with costs. Du Pont’s CEO though does note they are starting to see “a deceleration in order patterns stemming from the ongoing global semiconductor chip shortage” which plays into the view of the US ISM on Monday which saw a decline in the new orders index. The potential for supply chain disruptions to impact on manufacturing activity is starting to be felt and it is worth noting overnight the details of the German Manufacturing PMI which had the output index at its lowest reading in 16 months and was only slightly above the 50.0 no-change mark – the headline PMI was 57.8 from 58.4.

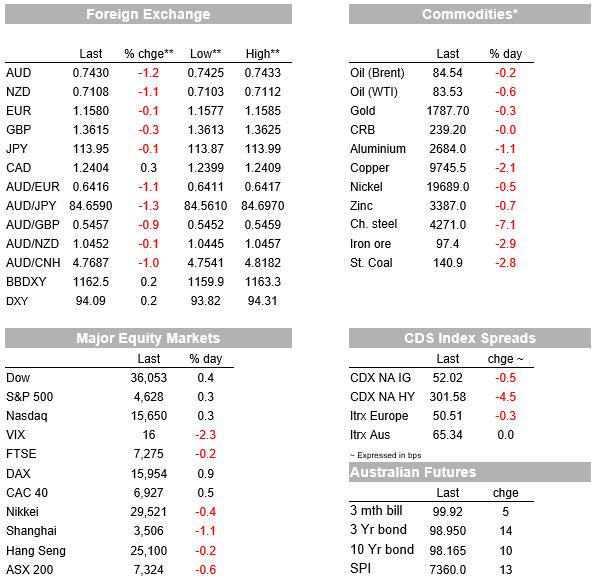

FX markets were dominated by the fallout from the RBA with the AUD -1.2% to 0.7430 and the NZD moving in sympathy to be down -1.1% to 0.7108. Adding to the downside pressure, safe-haven currencies have outperformed, with broad USD (BBDXY +0.2%) and JPY strength (USD/JPY -0.1% to 113.95). Other major pairs were less moves with GBP -0.3% and EUR -0.1%. Weakness in the AUD also came amid headlines of sharp falls in iron ore futures with the iron ore futures on the Dalian exchange limit down -9.95% yesterday. Those moves were also reflected in Singapore futures (-8.6%) with reports steel production curbs weighing on steel production with such curbs extending into Q1 for the blue skies policy for the Winter Olympics. Other headlines in China have also not been pretty with Premier Li Keqiang stating the Chinese economy faced new downward pressures and has to cut taxes and fees to address the problems faced by SMEs.

While Premier Li did not say what was driving the ‘downward pressure’ the regulatory crackdown and the woes in the property sector are prime candidates, as is China’s zero-COVID policy which is seeing restrictions put back in place in many provinces with the latest virus flare-up spilling over to more than half of Chinese provincial-level regions according to the Global Times. Flights in/out of Beijing have been significantly curtailed, while many cities have closed indoor entertainment and cultural venues. An editorial in the Global Times suggests China is not intending on backing away from zero-COVID, meaning the potential for supply chain disruptions persisting for longer remains. Highlighting potentially how dire the situation could be, the Ministry of Commerce put out a press release urging local authorities to ensure there was adequate food supply during winter and encouraging people to stock up on some essentials.

As for the RBA yesterday, at the meeting the RBA formally abandoned the YCC target which it failed to support last week, with the Governor noting he exercised his discretion given the balance of probabilities on rates had shifted with it now being “plausible that a lift in the cash rate could be appropriate in 2023 ” and thus no longer aligned with the April 2024 YCC target. Part of that shift was the higher than expected Q3 CPI figures with the RBA consequently revising up their core trimmed mean by 50bps in 2022 to 2¼% and 25bps in 2023 to 2½% inflation track. Backing out the implied quarterlies suggests the RBA sees core prints of around 0.6% q/q a quarter until mid-2022. Wages growth forecasts though were only upgraded marginally with WPI at 3% at the end of 2023. The RBA noted that inflation at 2.5% and being forecast to track above, along with wages growth at 3% plus remain key to hiking and that their central scenario is still consistent with a 2024 hike, notwithstanding they can also see 2023. This puts the focus on wages with the WPI print on November 17 key for a further unwind in market pricing.

Governor Lowe tried to push back against market pricing in his post-Meeting Speech, noting hikes as early as 2022 were “extremely unlikely”. Nevertheless, market scepticism remains high around the RBA’s guidance and is likely centred on three things: (1) the RBA continues to downplay global inflation trends with Governor Lowe still thinking Australia will lag the global inflation/rate hike cycle which exposes the RBA to considerable upside risks; (2) the RBA has consistently been too dovish coming out of the pandemic on its forecasts; and (3) Governor Lowe continues to show little tolerance for inflation being above the mid-point of the target with the inference being that the RBA is operating something closer to an inflation cap around 2.5% rather than seeking to average the mid-point of the band over the cycle. This last bit is particularly relevant given the potential for global inflation spillovers as well as wages growth to pick up due to re-opening frictions amid the still largely closed international border. NAB’s view is that the RBA hike rates from mid-2023 with a relatively aggressive series of hikes thereafter to bring the cash rate to 1.75-2.00% by end 2024. NAB also expects QE to end in February 2022.

Finally across the ditch in NZ RBNZ Governor Orr’s speech on “Housing Matters” didn’t rattle the market and didn’t offer anything new in the way of policy response. Orr suggested that the role of the RBNZ was a “bit part” and “with regard to using interest rates to target house prices, this is not in our mandate – nor does it make sense”. The Bank’s role is “more about limiting damage to bank’s balance sheets, rather than altering overall demand”. In terms of increasing its macro prudential policy toolbox, Orr confirmed that the Bank was well advanced in work to commence consulting on additional “debt servicing ratio” tools.

Only Building Approvals domestically which shouldn’t trouble the scorers. Across ditch in NZ key labour market data and the RBNZ Financial Stability Report are out. Offshore there will be passing interest in China’s Caixin Services PMI, while in the US attention will be squarely on the FOMC meeting for confirmation of the taper and whether the Fed is becoming more worried on the inflation outlook. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.