We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Risk off ahead of a big week for data, partly driven mainly by China virus news

https://soundcloud.com/user-291029717/china-flares-up-putin-flexes-more-us-dollar-pushes-higher?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

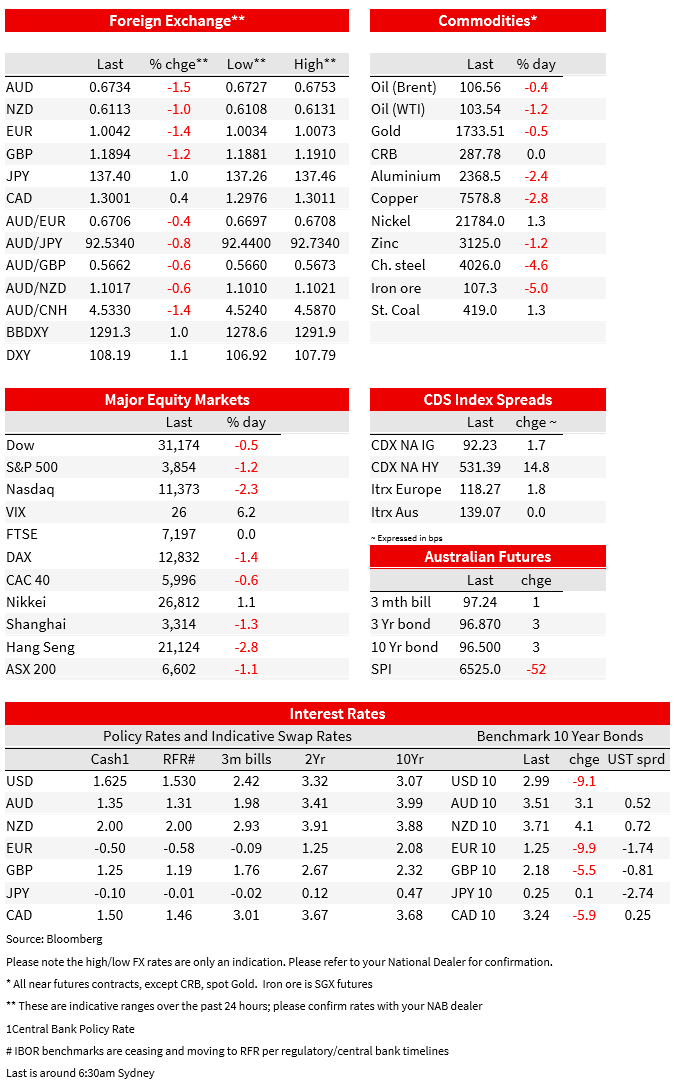

A risk-off start to the week ahead of upcoming key risk events of US CPI (Wednesday) and corporate earnings. The catalyst appears to have been China’s new virus outbreak, dashing hopes of stimulus gaining traction, with some 30m people subject to enhanced virus restrictions covering six cities and counties according to Bloomberg. Worries over the European gas situation and whether Russian gas will resume to the same extent once the maintenance period for the Nord Stream pipeline is finished (11-21 July) also added. Equities fell sharply (S&P500 -1.2%; NASDAQ -2.3%), while the USD DXY rose with the primary driver being a weak EUR which is now close to parity (-1.4% to 1.0045), along with a weak Yen (USD/JPY +1.0% to 137.42). The AUD was the weakest G10 currency at -1.5% to 0.6734 highlighting its proxy for global risk sentiment. Yields moved lower with the US 10yr -9.9bps to 2.99%, giving up its post-payroll rise, and curves a flatter (2s10s -6bps to -8.5bps).

Fed talk has been mixed with George warning moving interest rates too fast risks “oversteering”, while Bullard is content with another 75bp rise. George noted while she is “sympathetic to the view that interest rates need to increase rapidly”, she also is mindful the pace of change also has an impact on sentiment, and that “just four months after beginning to raise rates, there is growing discussion of recession risk… Such projections suggest to me that a rapid pace of rate increases brings about the risk of tightening policy more quickly than the economy and markets can adjust”. (see George: Tightening Monetary Policy in a Tight Economy). While the comments didn’t necessarily see too much movement in Fed pricing, it likely dispels any notions of a 100bp hike should CPI on Wednesday surprise substantially higher. Fed Funds Futures imply a 99% chance of a 75bp hike, and a peak rate of 3.50% in February 2023 which is marginally lower from Friday’s 3.58% in March 2023.

Despite the caution, some optimism may be warranted as far as the inflation outlook is concerned. The NY Fed’s global supply chain pressures index fell over the past month to be at its lowest since March 2021. The fall in the index is consistent with the decline in higher frequency container freight rates. A recent WSJ article contract freight rates have started to follow spot rates lower with one official at a large U.S. importer recently seeing a 15-20% reduction to ocean contract rates relative to several months ago (see WSJ: Freight Rates Are Starting to Fall as Shipping Demand Wavers). The NY Fed’s inflation expectation series also saw a fall in the 3yr expectation to 3.6% from 3.9%, though the 1yr expectation did rise to 6.8%. Finally US gasoline prices have now been falling for 25 consecutive days, suggesting the July CPI report should see some easing in headline inflation at least.

The news out of China remains on the soft side despite talk of stimulus and bumper credit figure last night. Some 30m people subject to enhanced virus restrictions covering six cities and counties according to Bloomberg. On the data front, China credit growth was much stronger than expected (aggregate financing 5170bn vs. 4200 expected) and was one of the highest monthly totals seen over the past five years. Whether this easing in credit conditions feeds through to the economy and gains traction is another matter given China’s zero COVID policy. It is still unclear when China will start to pivot to living with COVID-19, and until it does, the potential for any stimulus ramp to be disrupted and multiplier effects impeded by restrictions remains.

Meanwhile in Germany the fear is all about whether the gas will be turned back on once the Nord Stream pipeline comes out of maintenance. The annual maintenance period is scheduled for 11-21 July, and 21 July will be watched closely for a resumption of gas flows through the pipeline. Ominously French Finance Minister Bruno Le Maire said Europe must prepare for Russian gas deliveries to be shut off entirely. As we noted yesterday, power rationing in Germany is already a feature of the energy market and a prolonged shutdown in the gas supply would be an economic tragedy. EUR has traded down 1.2% to 1.0043 and this could be the week that parity is broken, the question being how far below it goes and for how long. Across the channel GBP has also been weak -1.2% given USD strength and ongoing political uncertainty with a new PM unlikely to be resolved until August/September.

The flight to the safety of the USD has been evident in FX markets, with dollar indices up in the order of 0.9% for the day and most majors trading at fresh multiyear or multi-decade lows. The AUD has been the worst performer, down 1.5% and trading down at a 2-year low of 0.6715. EUR (as above) and JPY have traded at their weakest levels in 20 years and 24 years respectively. In the case of the yen, some in the market are seeing the increased majority of the LDP party in the weekend’s upper house election as a quasi-referendum on the country’s ultra-easy monetary policy. Thus, downside pressure on the yen has continued and USD/JPY has traded as high as 137.75.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.