Total spending grew 0.9% in June.

The US dollar has fallen again with rises in the Euro and a shift up in the Yuan, but will it stick?

https://soundcloud.com/user-291029717/china-gets-yuan-up-on-the-dollar?in=user-291029717/sets/the-morning-call

They say that breaking up is hard to do, Now I know, I know that it’s true – Neil Sedaka

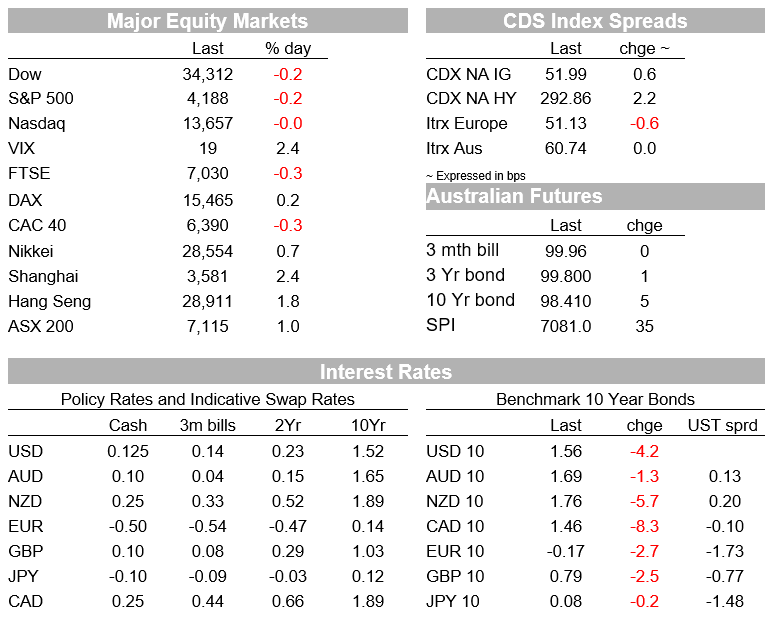

It hasn’t been a big night for markets, though the USD is weaker with indices at their lowest levels since 6 Jan, US (and indeed global) benchmark bonds yields are lower amid more incoming soothing words on inflation from Fed officials, and equities have given back only a tiny portion of Tuesday’s strong gains seen globally. USD/CNH dropped below the psychologically important 6.40 level late in our day yesterday for the first time since mid-June 2018 – but not as yet USD/CNY – while EUR/USD has poked it’s head above 1.2250 for the first time since 8 Jan and is the main reason the USD is lower. AUD/USD meanwhile remains mired near 0.7750 (sigh – at least from your currency research scribe). Breaking up closer to our ~0.80 fair value estimates remains hard to do.

Incoming US and European data sees the German IFO Business Climate survey lifting to an above-expectations 99.2 from 96.9 (99.0 expected) with the Current Assessment up to 95.7 from 94.1, better than the 95.5 consensus. US data was mixed with April New Home sales falling back 5.9% after the 20.7% March jump but which was a little less weak than feared, while the Conference Board’s Consumer Confidence survey slipped a little more than expected – to 117.2 against 118.8 expected, but off an exceptionally strong 121.7 April reading. The ‘present situation’ reading, up to 144.3 from 139.6 and fuelled by stimulus cheque still not yet spent and jobs evidently very easy to get – contrasts with a setback in the expectations reading to 99.1 from 109.8. Maybe we have now reached peak consumer confidence, though there is doubtless still plenty of pent-up demand still to be sated as the US economy continues to more fully re-open. The Richmond Fed

Manufacturing Index rose to 18 from 17, just below the 19 expected.

The most significant Fed speak overnight came from Fed Vice chair Rich Clarida Clarida in a Yahoo Finance interview , who repeated that he believed recent inflation pressures would “prove to be largely transitory,” arguing that the details of the report were consistent with that view, but also said “It may well be” that “in upcoming meetings, we’ll be at the point where we can begin discuss scaling back the pace of asset purchases…I think it’s going to depend on the flow of data that we get.” So a bob each way from him, and something of a sop to the minority of FOMC meetings who, last week’s April meeting minutes revealed, were starting to agitate in favour of a tapering discussion before too many more meetings (subject to the intervening flow of data of course)

In contrast and also notable were the comments from Chicago Fed president Charles Evans – a current FOMC voter – who said that “The recent increase in inflation does not appear to be the precursor of a persistent movement to undesirably high levels of inflation….I have not seen anything yet to persuade me to change my full support of our accommodative stance for monetary policy or our forward guidance about the path for policy.”

Elsewhere Fed Vice chair for financial supervision Randal Quarles in testimony says the Fed will wait to see jobs data before acting, while Atlanta Fed president Raphael Bostic – also a 2021 FOMC voter – said “I am not seeing that it (inflation) is going to be enduring”

Bond markets on net liked what they heard from Fed officials, which together with tailwinds from lower European yields (German 10 year Bunds down 3bp and French OATS -4bps) sees US 10-year Treasuries ending the US session down 4bps at 1.56%, so very much near the bottom than the top end of the 1.53-1.75% effective range in place since the start of April.

Equity markets have ended a touch softer on Wall Street, but with the more interest-rate sensitive NASDAQ outperforming the S&P 500 and the Dow, off just 0.03% against -02% for the latter two indices. This followed a narrowly mixed performance by European bourses.

In currencies, the news as we were shutting shop Tuesday was that the offshore Renminbi (CNH) had dropped below 6.40 for the first time since mid-June 2018 (to a low of 6.3922) though it is currently back near 6.41 and USD/CNY only managed an overnight low of 6.4021. The significance of the 6.40 level is that it was the springboard from which China orchestrated the move up to 7.00 from June 2018 (and later in 2019 to as high as 7.20) initially in response to the Trump administration announcement of 10% tariffs on additional $200bn worth of Chinese imports (even though the trade war had kicked off at the start of the year with solar panels/washing machines, and USD/CNY had been as low as 6.25 before June). Amid conflicting reports from Chinese officials in recent days about their attitude to the currency, our read here is that 6.40 is not a hard line in the sand, and that in the context of further downward pressure on the USD more generally, it will be ‘allowed’ to trade lower. Our long standing forecast for USD/CNY at end Q2 2021 is 6.35.

The DXY and BBDXY USD indices both fell to their lowest level since January 6 (the day before the Georgia Senate election results were known). When considering that USD/JPY has a big weight in both these indices (13.6% and 14.6% for DXY and BBDXY respectively) and USD/JPY is a currency that has been marching to its own drum this year (ultra-sensitive to US treasury yields and some 6% higher YTD as a result) it is fair to say that the USD is for the most part already well through its beginning of year lows. EUR/USD has led the latest move down in the indices, rising to above 1.2250 yesterday (a significant technical level) though the air above here is so far proving thin – we think only temporarily. GBP is not faring so well having been the strong May outperformer, and where the vibe in the UK is that the currently planned fuller economic reopening from June 21 may well not proceed given the (so far localised) outbreaks of the Indian covid variant.

Finally, AUD greets us this morning stuck very close to 0.7750, after a fleeting rally attempt early in the European day and in the context of the rising CNH and falling USD, ran out of steam around 0.7775.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.