NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

A switch of market focus from Ukraine to China (and Hong Kong)

https://soundcloud.com/user-291029717/china-hit-by-covid-and-russian-relationship?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

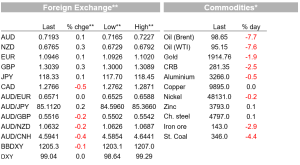

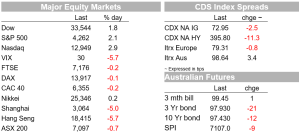

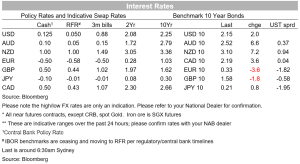

After a flat to small down day for European stocks, US equities are closing with gains of 2.1% for the S&P500 and 2.9% for the NASDAQ, oil falling back below $100 one factor. US Treasury yields have held on to Mondays push up to 2.15% at 10-years, the front end of the curve also little changed, with a degree of inertia evident in front of tomorrow morning’s FOMC decisions. The USD is a touch firmer, helping keep AUD languishing beneath 72 cents, alongside weaker commodity prices, yesterday’s sharply weaker China and Hong Kong stock markets and now a weakening Chinese Yuan. Nothing substantial regarding Ukraine-Russia peace talks, though at least the two sides are still talking.

It was hard not to snigger at a headline that crossed the wires an hour ago trumpeting ‘Oil enters a bear market’. True, prices are now more than 20% of their recent highs for both WTI and Brent crude, but it’s doubtful anyone anywhere in the world is about to start a conversation with their local servo attendant that starts ‘Now, about that oil bear market….’

While its tempting to attribute the fall-back in oil to optimism towards an early cessation of hostilities in Ukraine – but which even if it were to occur would not lead to an immediate lifting of sanctions, self-imposed or otherwise, on Russian oil, it more likely reflects a combination of some speculative froth being blown off, alongside fears of weaker China demand as more Chinese cities are put into lockdown amid record high Covid case numbers – as tiny as these are relative to most other parts of the world.

Certainly the latter is having a hand in the under-performance of Chines stocks, the CSI 300 off another 4.6% yesterday. In Hong Kong, which is suffering the worse fatality rates per million of any country in the world since the start of the pandemic amid startlingly low vaccination rates amongst the elderly population – as well as concerns over vaccine efficacy in both China and HK versus the west – the Hang Seng fell by 5.7% yesterday to be 21% down year-to-date and more than 40% off its February 2021 highs.

Yesterday’s China activity data , covering the Jan-Feb period for industrial production, retail sales and fixed asset investment, all comfortably exceeded expectations at up 7.5%, 6.7% and 12.2% respectively on the corresponding period of last year. But the numbers largely predate the city lockdowns arising from last covid outbreaks and look to have been partially flattered by base effects (weak numbers in Jan-Feb last year). The ‘invisible hand’ of government support measures, not just in infrastructure but also services spending, which is not all done by the private sector. And in absolute terms, the numbers still reflect a slowing in growth, highlighting the challenge, admitted by Premier Li last week, in meeting the 5.5% 2022 GDP growth target.

Yesterday, against expectations, there was no immediate further easing in monetary policy from the PBoC, the MLF rate held steady at 2.85%. As one form of easing though, the PBoC did set the USD/CNY fixing more than one Yuan above expectations (and on Monday,1.5 yuan above the market-implied rate). This represents a clear protest at Yuan strength and we suspect there is more to come on this front, removing one recent support factor for the AUD.

The Yuan has received a temporary boost overnight (USD/CNH down from above 6.40 to 638) on reports that Saudi Arabia is looking to receive payment for some of its oil exports to China in Yuan . ‘Some’ is the operative word here (China imports about a quarter of Saudi’s exports) and this has been talked about for years. Certainly it could play with the grain of reserve manager diversification desires to hold more yuan (why receive dollars for oil from China only to then sell some of them for Yuan?). A subject to keep tabs on, but probably of limited immediate significance.

Last week, AUD/USD was hard to find above 0.74, this week it is quite easy to give away below 0.72. After a period where the uplift from soaring commodity prices was clearly countering the downdraft from risk sentiment, both forces have been working in the same direction in recent days, pulling AUD/USD down to a low of 0.7165 overnight, albeit now back flirting with the 0.72 handle and so up on Monday’s close. The JPY and CHF meanwhile continue to show none of the safe haven attributes for which they have been famous, USD/JPY up to an overnight high of Y118.45 (and AUD/JPY to 85.36) while USD/CHF is up 0.25%, making CHF the weakest G10 currency on the day. EUR/USD is a smidge higher at 1.0945, GBP more so (+0.3%) after a set of very good labour market numbers.

In key US economic data released overnight saw annual PPI inflation crack the 10% mark for the first time this cycle, but the core measure was 0.3 percentage points weaker than expected at 8.4% y/y. The Empire State manufacturing index fell into negative territory, to reach minus 11.8, its lowest level in almost two years, indicative of some weaker economic momentum before the Fed even begins to raise rates.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB specialists and clients from across the bank’s Fund Sponsors, Strategic Investors and Alternative Assets (FSA) business gathered over lunch recently to share career stories and advice on promoting greater diversity and inclusion.

Hybrid issuance is becoming an ever more relevant funding instrument and capital management tool for corporate issuers today, attracting strong investor demand, write Tabitha Chang and Stefan Visser from the NAB Capital Markets Origination team.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.