Our monthly transaction data suggest spending ticked up in April after a stagnant performance last month

Insight

Risk appetite soared on Friday as Chinese whispers swept markets last week that China had put together a ‘conditional re-opening plan’, reportedly mapping out a material re-opening by March 2023.

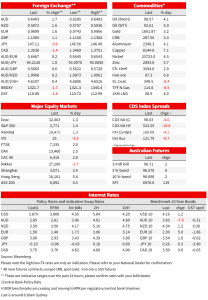

Risk appetite soared on Friday as Chinese whispers swept markets last week that China had put together a ‘conditional re-opening plan’, reportedly mapping out a material re-opening by March 2023. Those rumours were denied on the weekend, leaving markets facing some disappointment as trade opens. In early morning trade the AUD has fallen -0.8% to 0.6412, after having soared almost 3% on Friday to 0.6483. Despite the denial, notions that China will pivot to living with Covid in the new year are unlikely to be quashed given the very real toll that zero-Covid is having on the economy. The two other major developments on Friday were a mixed US Payrolls report (headline payrolls beat at 261k vs. 193k expected, but unemployment rose two tenths), and Fed speak that was noticeably less hawkish than Chair Powell’s post-FOMC press conference. Notably Boston Fed President Collins remarked: “The pathway in which we’re able to bring inflation down…without a significant downturn—it’s important for that pathway to be recognized”.

Markets pared terminal US Fed pricing slightly to 5.10% from 5.15% on Thursday, while the probability of a repeat 75bp hike in December has fallen to 22%. The US 2yr yield spiked as high as 4.80% post payrolls, but more than reversed all of that to close down -5.5bps to 4.65%. Moves in 10yr were less volatile and closed at 4.16%, though TIP yields did fall -6.7bps to 1.68% with the implied inflation breakeven lifting to 7.5bps to 2.48%. The Chinese re-opening whispers saw a pronounced reflation trade in risk assets with commodities soaring: Brent oil +4.1%, Copper +7.1% (biggest one day increase since 2009), Gold +3.2%. Equities also lifted, though that was also partly on the back of Fed talk being less hawkish and payrolls being ok, with the S&P500 closing up 1.4%. EM equities rose sharply with HangSeng +5.4%. One summary of EM equities is the iShares MSCI Emerging Markets ETF which soared 4.2%.

FX also saw sizeable moves with USD/CNH -2.1% to 7.1796, with the AUD quickly following up some 3% at one point to 0.6483. Note AUD gains have been pared, with the AUD falling this morning by -0.8% to 0.6412 given the denial of those re-opening rumours. NZD was also lifted sharply by 2.8% to 0.5936 and has also fallen in early trade by -0.7% to 0.5889. With equities soaring, and noticeably less hawkish Fed remarks, the USD was on the backfoot with the DXY -1.9%. Gains were seen across most pares with EUR +1.6%, GBP +1.1%. USD/JPY though did lag at -0.8% to 147.11. Meanwhile the CAD was 2% higher on Friday, helped by a robust Canadian labour market report which showed much stronger-than-expected job growth (108k vs. 10k expected) and a lower-than-expected unemployment rate, a warning that the Bank of Canada might have more work to do with its tightening cycle.

First to the China re-opening rumours that were subsequently denied on the weekend. Rumours had been circulating early last week based on WeChat messages but stepped up a notch on Friday after a former senior official at China’s Centre for Disease Control reportedly told a Citi conference that China would reopen to HK early next year, progressively followed by other areas. Adding weight to the rumours, Bloomberg reported that China was looking at dropping penalties for airlines which carried Covid-positive passengers and part of a three-step plan to revive the aviation industry. While German Chancellor Scholz announced that the Pfizer-BioNTech mRNA vaccine would be made available to expats living in China. China to date has chosen not to use imported mRNA vaccines, instead relying on domestically produced vaccines. Rumours of a pivot were denied on the weekend with the National Health Commission said it would “unswervingly” stick by its current Covid approach.

Still notions that China will pivot to living with Covid in the new year are likely to remain given the significant economic cost of zero-Covid. Such an easing would more likely come after the winter (many cite Spring, with March/April being pegged as one possible date) given the lower vaccination levels in China for people over 60 years and the potential of a re-opening wave to overwhelm the health system. Bloomberg noted that China’s official Xinhua News Agency last month cited a study saying that an uncontrolled omicron wave could overwhelm the hospital system and lead to nearly 1.6m deaths — about 50% more than the US has recorded so far. That scenario would undermine Xi’s approach both at home and abroad, and risk making him look weak at a time when the Communist Party leadership is facing criticism over a slowing economy.

As for US Payrolls, it was a mixed report with a strong headline print, but the unemployment rate ticked up two-tenths to 3.7% against 3.6% expected. As for the headline, payrolls printed at 261k vs. 193k expected and 263k previously. There were also upward revisions to the prior two months’ worth 29k. Some analysists have also pointed to a large divergence developing between payrolls in the establishment survey and employment adjusted to a payrolls concept in the household survey – the gap is now 2.0m jobs and the largest since the early days of the pandemic in July 2020, though it is unclear which way it will close. As for average hourly earnings it was close enough to consensus at 0.37% against 0.3% expected and the y/y was as expected at 4.7%. Importantly the 3-month annualised for average hourly earnings is now running at 3.8%, well down on the 6% rates seen last year. It seemed markets were primed for a blowout print given JOLTS and ADP, with an ok payrolls report taken positively.

Fed speak was generally supportive for risk assets with some divergence starting to develop at the FOMC it seems. Comments by Collins, Barkin and Evans were less hawkish than Chair Powell in his FOMC press conference. Kashkari though remained very hawkish, while former-Treasury Secretary Summers said, “it would not surprise me if the terminal rate reached 6 or more”. Boston Fed President Collins made two interesting remarks which played to the view of the Fed downshifting the size of hikes, as well as looking closely at the activity side as well as the inflation side. Collins said: “It is time to shift focus from how rapidly to raise rates, or the pace, to how high.” And perhaps more importantly on whether a recession is necessary: “The pathway in which we’re able to bring inflation down…without a significant downturn—it’s important for that pathway to be recognized,” … “I do worry that the presumption by some that a recession is almost inevitable is not helpful because I truly do not see it that way.” (See WSJ: Fed’s Collins Signals Support for Slowing Pace of Interest Rate Increases).

As for the Fed’s Barkin, he was supportive of a downshift (“When you get your foot on the brake, you think about steering in a very different way. You pump the brakes, sometimes you act a little bit more deliberatively, and I’m ready to do that”) as was the Fed’s Evans (“From here on out, I don’t think it’s front-loading anymore, I think it’s looking for the right level of restrictiveness”). (See CNBC: Fed officials Barkin and Collins see possibility for slower rate hikes ahead). Kashkari though was very hawkish, noting in re-action to the payrolls report: “That tells me we have more work to do to try to cool down the economy and bring demand and supply into balance” and that he was going to revise his dot point to above 4.9% which he had at the September FOMC (“Given what I know right now, I would expect to go higher than that. How much higher than that, I don’t know”).

Finally wrapping up central bank talk, the BoE continued to push back on market pricing. Chief Economist Huw Pill told CNBC on Friday: “We don’t think interest rates would need to rise as high as the market has been pricing, precisely because that would induce a slowdown in the economy that is bigger than is required to get these inflationary dynamics under control”. Notably on the depth of the recession needed to bring inflation under control: “What we are seeking to do, we’re always seeking to do this, is to find that balance that gets us back to our 2% inflation target without generating unnecessary and costly problems in the real side of the economy” (see CNBC: Markets need to ‘re-anchor their thinking’: Bank of England chief economist hints that traders have it wrong). Markets are currently pricing a BoE terminal rate of around 4.7%.

NAB Markets Research Disclaimer

Our monthly transaction data suggest spending ticked up in April after a stagnant performance last month

Insight

Conditions, employment fall back to long-run average

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.