Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

The rising Yuan is clearly a concern for the PBoC who announced measures to tackle it, whilst Chinese authorities are now permitting families to have three children.

https://soundcloud.com/user-291029717/china-wants-to-curb-the-yuan-and-grow-the-family

“If we took a holiday; Took some time to celebrate; Just one day out of life; It would be, it would be so nice”, Madonna 1983

Markets were very quiet overnight with both the US and UK out on holidays. Global headlines though were interesting with the UK reporting just one virus death and zero deaths in England for the first time since the pandemic began. The UK’s sharp fall in deaths suggests markets can remain confident on the efficacy of vaccines and of a broader pickup in services consumption and travel. On the back of vaccine optimism and US fiscal stimulus the OECD upgraded its forecasts for global growth to 5.8% this year and 4.4% next year from 5.6% and 4.0% respectively back in March. The other notable development was the PBoC pushing back on the pace of Yuan strength, while China is now allowing people to have three children instead of two in an attempt to boost population growth.

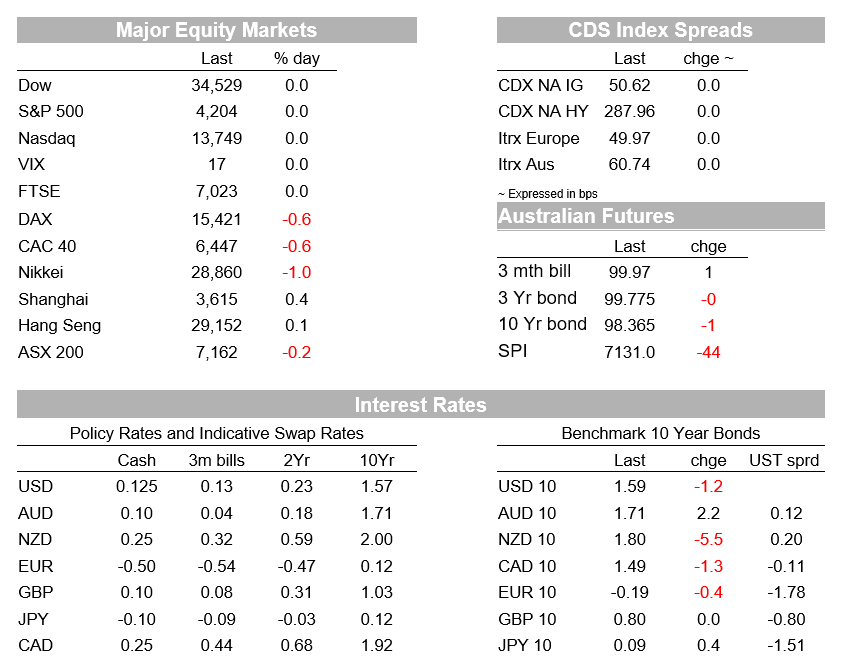

As for market moves, European equities were weaker overnight with the EuroStoxx 50 -0.8% with the DAX also down -0.6%. Weighing on European shares was a sharp 1.3% fall in Deutsche Bank after the WSJ reported the US Fed had told the bank to address persistent shortcomings in its anti-money-laundering controls. Also weighing was German CPI data that came in one-tenth hotter than expected at 2.4% y/y against 2.3% expected, the highest since November 2018. Note Spain was also 2.4% y/y. Hotter than expected CPI adds currency to the view of the ECB tapering its asset purchases earlier than what President Lagarde has said previously (her last comments were that it was “far too early ” to be talking about tapering). US equity futures are also pointing to a negative open.

Rate moves have also been modest with German 10yr yields -0.4bps to -0.19%. Over the past month it has been another range-bound month with the US 10yr trading in a 20-25bps range with the US 10yr yield only 3bps below its end April level, while the AU 10yr future is 6bps lower in yield. Delving into the implied inflation breakeven in the US suggests a more nuanced story with the implied 10yr inflation breakeven up 4.2bps to 2.45% and suggests markets are still worried about the potential for inflation to lift. A downward sloping BEI and inflation swaps curve though does suggest the market thinks the lift in inflation will be temporary.

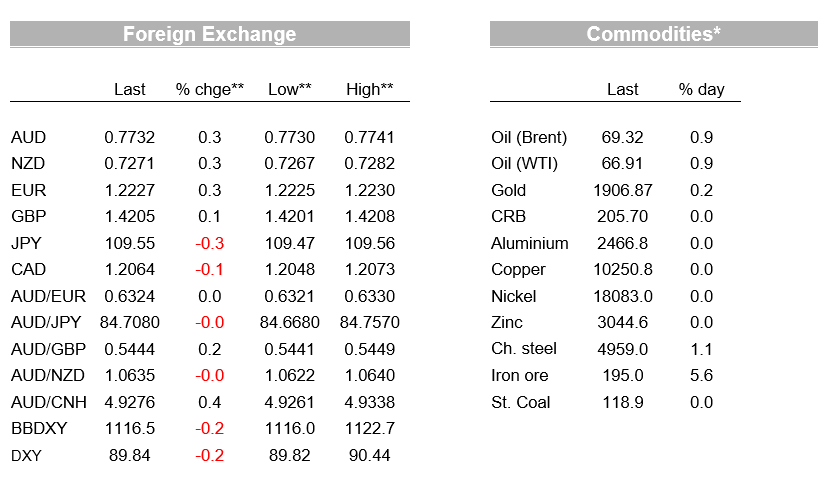

In FX, the biggest piece of news was the PBoC pushing back on the pace of Yuan strength. Three actions have been taken since Sunday, including: (1) a former PBoC officials being quoted in Xinhua of stating China should prevent huge short-term inflows, which could push up the yuan and hurt competitiveness of exports; (2) the PBoC raising the reserve requirement for banks’ foreign exchange deposits to 7% from 5%; and (3) fixing the Yuan reference rate at 6.3682 per dollar against the consensus of 6.3656. USD/CNY took a peek below 6.36 yesterday, a fresh three-year low, before weakening and ending the session close to 6.37.

The Chinese Manufacturing PMI yesterday does hint that export orders are coming under pressure with the Export Orders sub-index at 48.3 from 50.4, while overall New Orders also fell to 51.3 from 52.0. The fall in export orders may hint of an anticipated pivot of consumers globally to services and away from goods, as well as a recovery in manufacturing production in other countries. On this later point it is worth noting the Baltic Dry Capesize Index looks like it has peaked with the index at 3,089, down from the peak of 5404 in early May, but still well above pre-pandemic levels of 1,623 in May 2019. The overall Manufacturing PMI was little changed at 51.0 v. 51.1 expected. The Non-Manufacturing PMI was one-tenth higher than expected at 55.2 v. 55.1 expected.

As for other FX moves, the USD was weaker with BBDXY -0.2%. Moves though haven’t been particularly significant. The AUD is up 0.3% to 0.7732, along with the NZD up 0.4% to 0.7280. EUR, GBP and JPY show gains of 0.1-0.3% against the USD to start the week, with NZD crosses flat to slightly higher.

A very busy day today with the RBA and pre-GDP partials ahead of Q1 GDP on Wednesday. Offshore it is also very busy with China’s Caixin Manufacturing PMI, Eurozone CPI, Canadian GDP figures and the US ISM Manufacturing Index. The Fed’s Quarles and Brainard are also on the speaking circuit. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.