Online retail sales growth slowed in May following a fairly strong April

Insight

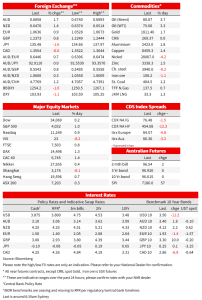

CPI comes in cool at 0.1% m/m and 7.1% y/y, two tenths below consensus

NZ: REINZ house sales (y/y%), Nov: -36.1 vs. -34.7 prev.

NZ: Food prices (y/y%), Nov: 10.7 vs. 10.1 prev.

AU: Westpac consumer conf, Dec: 80.3 vs. 78.0 prev.

AU: NAB business conditions, Nov: 20 vs. 22 prev.

UK: Unemployment rate (%), Oct: 3.7 vs. 3.7 exp.

UK: Weekly earnings x bonus (3m/y%), Oct: 6.1 vs. 5.9 exp.

GE: ZEW survey expectations, Dec: -23.3 vs. -26.4 exp.

US: NFIB small bus. optimism, Nov: 91.9 vs. 90.5 exp.

US: CPI (m/m%), Nov: 0.1 vs. 0.3 exp.

US: CPI (y/y%), Nov: 7.1 vs. 7.3 exp.

US: CPI ex food, energy (m/m%), Nov: 0.2 vs. 0.3 exp.

US: CPI ex food, energy (y/y%), Nov: 6.0 vs. 6.1 exp.

A softer than expected US CPI has seen the US dollar lower and treasuries rally, led by the front end as curves steepen and bets for the path for the Fed are pared. The November CPI came in at 0.1% m/m and 7.1% y/y, two tenths below expectations and the smallest increase since August 2021. US equities are tracking higher, but have pared most of their gains post CPI.

Last month’s positive surprise came with the caveat that it was ‘just one month of data’ but the November numbers add further weight to the interpretation that the long-awaited goods disinflation is showing up in the data, led be declines in used car prices. Evidence of easing inflation is welcome, but with wages growth as high as it is the Fed will be cautious that some unwind of earlier price increases, while welcome and a drag on inflation, won’t be enough to see it fall far enough or keep it lower even with some recovery in real wages.

As for the detail, core CPI came in at 0.2% and 6.0% y/y, one tenth below consensus. Helping the core lower was a larger fall in used car prices (2.9%) in the month than the lead from auction prices, which led a 0.5% m/m fall in core goods prices. Headline came in two tenths below expectations at 0.1% and 7.1% y/y (0.3/7.3 expected), with a 2% fall in gas prices. Rents inflation remained high at 0.7% m/m, but the lead from new rents gives confidence that will be moderating in a few months.

Treasuries have rallied and the curve steepened as rate hike bets have been pared. The 2yr down 17bps to 4.21%, down just under 60bps from the 4 November peak of 4.8%. The 5yr was 14bps lower to 3.64% and the 10yr off around 12bps to 3.49%. The 2s10s curve steepened to -73.3. The softer CPI print has further cemented in expectations of a dialled-down 50bps hike tomorrow to take the Fed Funds target range to 4.25-4.50%. The bigger question is what it means for the path for policy further out. Pricing for early February now leans in favour of a further step-down to 25bp hike with an incremental 33bp priced, from 39bp yesterday, while the peak rate in May sits at 4.84% from 4.95 yesterday.

That reaction was mirrored in currency markets. The US dollar was 1.1% lower at 103.93. The JPY was among the best performers. The USD/JPY fell 1.5% to 135.56 as lower US yields supported. Benefitting from the positive risk tone, the AUD was 1.7% higher at 0.6858 after reaching an intraday high of 0.6893, its highest since 13 September. The NOK was the best performing G10 currency, up +2.2% and buoyed by higher oil prices. Brent was 3.7% higher to be back above US$0.80

US equities opened higher but have fallen back throughout the day. The S&P500 was up 2.8% soon after the open before paring gains throughout the day even as currency and rates markets largely held on to their post CPI reaction. The S&P500 is currently tracking around 0.6% and the Nasdaq 1.0% higher. European equities were higher with the Euro Stoxx 50 +1.7%, helped by the risk on move post CPI.

As for whether the reaction in currencies and rates can be sustained, attention turns to the FOMC meeting 6am tomorrow morning Sydney time (more in ‘coming up’ below). Chair Powell has a difficult balance to tread. There is welcome news in the inflation report, but celebrating that with markets already sceptical of higher-for-longer rates and easier financial conditions unhelpful is a challenge given a wages backdrop that is still too hot to be comfortable inflation will fall sustainably back to target.

In other news and also supporting the risk on tone, Hong Kong announced it is ending some its last pandemic restrictions on arrivals to the city. These include a ban from entering bars and restaurants for 3 days after arrival and the end of a QR code app to log entry and enforce movement restrictions. China’s ambassador to the US said the country will continue relaxing its pandemic restrictions and will open to international travellers soon.

In the UK ahead of the BoE on Thursday and inflation data tonight, UK average weekly earnings strengthened further to 6.1% y/y and the unemployment rate rose a tenth to 3.7%, as expected. Strikes among rail workers are set to broaden to other professions. For Thursday, market pricing allows around a 25% chance of a larger 75bp move.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.