NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Markets opened with a cautious mood to start the week , reflecting on both the stellar US payrolls report on Friday and the surge in the delta variant which has seen China tighten restrictions and Israel contemplate another lockdown. The Fed’s Bostic was the first voter to speak post payrolls, indicating that the Fed should taper after one or two more payroll prints.

https://soundcloud.com/user-291029717/code-red-but-focus-is-on-the-fed?in=user-291029717/sets/the-morning-call

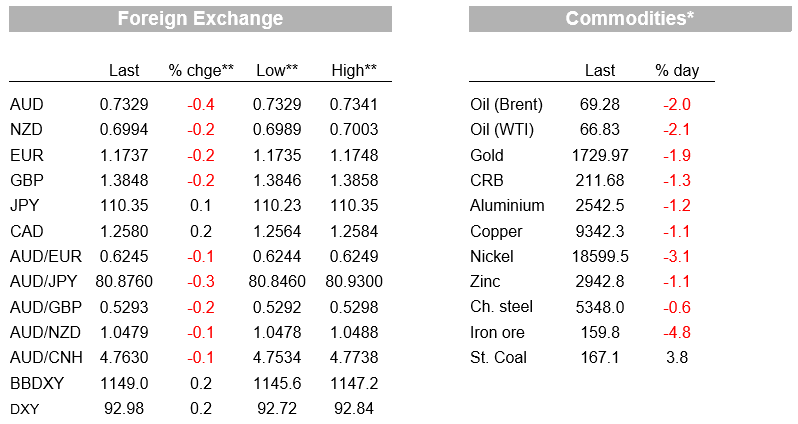

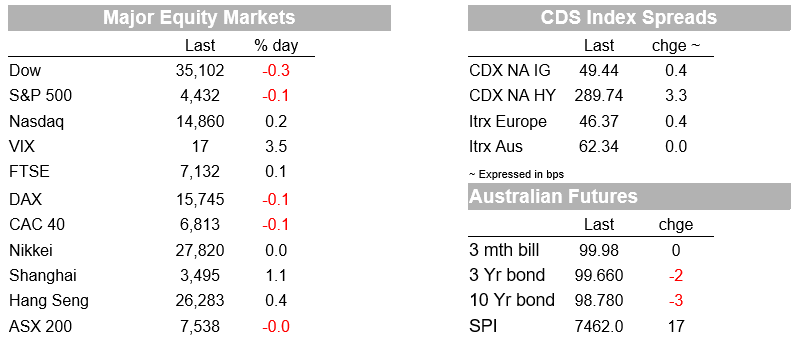

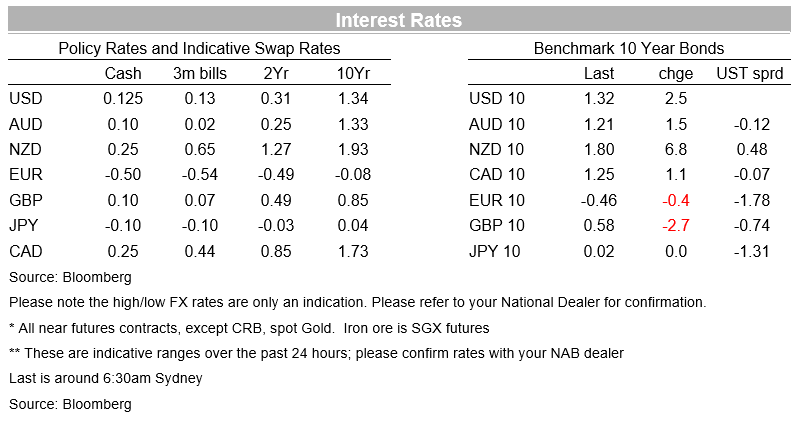

Markets opened with a cautious mood to start the week , reflecting on both the stellar US payrolls report on Friday and the surge in the delta variant which has seen China tighten restrictions and Israel contemplate another lockdown. The Fed’s Bostic was the first voter to speak post payrolls, indicating that the Fed should taper after one or two more payroll prints. With tapering clearer the focus for markets is shifting to what does the tapering profile imply for the timing and pace of rate hikes. As for market moves, the S&P500 fell slightly by 0.1%, dragged down by the energy sector (-1.5%) with WTI oil down -2.0% on delta concerns. Financials (+0.3%) in contrast were up given the lift in yields. Yields rose with the US 10yr +2.5bps to 1.32%, marking four straight days of increases from 1.17% on Tuesday. There were sizeable falls in other commodities including copper (-1.1%), along with gold (-1.9%) even after some recovery from its flash crash in Asia. FX has seen a cautious tone with the USD gaining (BBDXY +0.2%) against most pairs and the AUD (-0.4%) underperformed

First to the US taper prospects. The Fed’s Bostic (voter) was the first out of the blocks to comment on Friday’s stellar payrolls report. In Bostic’s view the report was “quite encouraging” and that “if we are able to continue this for the next month or two I think we would have made the ‘substantial progress’ toward the goal and should be thinking about what our new policy position should be.” “ Right now I’m thinking in the October-to-December range, but if the number comes back big…I’d be open to moving it forward,”. Note the Fed meetings for the rest of the year are September, November and December. The Fed’s Rosengren (non-voter) also spoke, noting tapering should begin in the fall.

With a tapering announcement becoming more certain at an upcoming meeting the focus is quickly shifting to the form of tapering to help inform on the likely timing of rates lift-off. Bostic notes that he supports reducing MBS and Treasuries at the same rate and that he would be in favour of tapering over a shorter period than what the Fed has previously done. A relatively fast taper would thus open up the possibility of a rate hike in H2 2022, contingent on achieving the maximum employment mandate (given inflation overshoot to anchor inflation expectations looks to have been achieved) (see NAB’s Australian Markets Weekly for details). Note Bostic was a former dove, having already made in road to Damascus conversion back in June when he pencilled in late 2022 for the start of rate hikes. Markets currently price around 20bps of hikes at the end of 2022, with the potential for this to shift given 7/18 Fed members in June saw a case for a 2022 hike.

Delta concerns in contrast continue to be a source of worry for markets. China has over recent weeks tightened restrictions and a number of banks have downgraded Chinese growth expectations over the past few days. Reflecting movement restrictions, Chinese airlines have reported a reduction in seat capacity of 32% in the past week. Those concerns are weighing on commodity markets with oil prices down overnight (Brent at one stage was down 4%), currently -2.0% $69.28. Industrial metals are also softer, with falls for the likes of copper (-1.1%), nickel (-3.1%) and aluminium (-1.2%). Gold and silver prices saw a flash crash during illiquid Asian trading conditions, the former temporarily going sub-USD1700 per ounce, before bouncing back. This was linked to a recurrence of selling pressure after Friday night’s strong US employment report and the lift in bond yields. The price has drifted lower overnight to be down 1.9% for the day to $1,729. Of more concern for the thesis of vaccines breaking the link between cases and hospitalisations, Israel is reportedly considering imposing a lockdown to help buy time to free up hospital capacity as hospitalisations increase in response to the delta outbreak. No announcement has been made, but it will be important to watch.

Economic data was sparse with only US job openings of any note. Job openings surged to a record high in June at 10.1m vs. 9.3m expected. The number of job openings at 10.1m again exceeds the number looking for work at 8.7m, with this trend having existed prior to the pandemic in early 2018. Optimistically for the outlook the quits rate increased, while layoffs and discharges was little changed. It is likely that labour supply will come back into the labour market as people become more confident in the path of the virus, and as children head back to the classrooms. The strength in openings also suggests there is good reason to expect further gains in payrolls ahead, which would further justify tapering and some shifting of the probability of hikes into late 2022.

FX moves have been dominated by USD strength with the DXY and BBDXY up 0.2%. The AUD is one of the weakest in the G10, down -0.4% in the face of commodity price weakness and also some global growth headwinds given the fall in commodity prices is in reaction to demand slowing due to the delta variant. EUR (-0.2%), GBP -0.2%) and USD/Yen (+0.1%) are slightly weaker.

The NAB Business Survey is the biggest piece domestically with focus on how conditions and confidence are faring amidst lockdowns in several cities. Offshore it is very quiet with only the German ZEW Survey and the Fed’s Mester of any note. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.