Total spending grew 0.9% in June.

US equities recover into the close calming market sentiment. Spike in VIX and rotation into defensive/tech stock point to a cautionary tale. European equities cannot escape the negative vibes from Asia

https://soundcloud.com/user-291029717/commodities-fall-vix-jumps-aussie-hit-hard-as-growth-concerns-rise?in=user-291029717/sets/the-morning-call

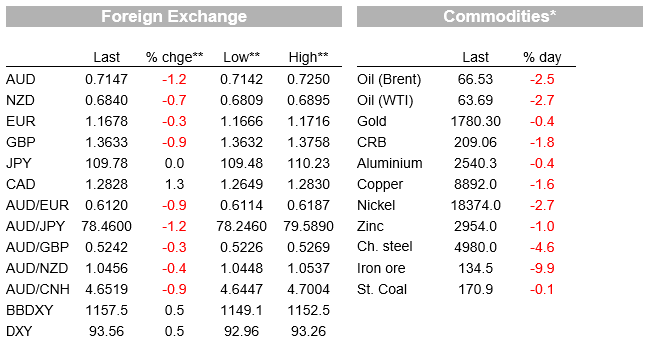

US equities recovered into the close providing a (temporary?) reprieve to the rout in risk assets, but spike in the VIX and rotation into defensive/tech stocks point to a cautionary tale while the broad decline in commodities reflect heightened concerns of a global growth slowdown. Move in core yields has been more subdued while king Dollar continues its ascendancy with pro-growth currencies bearing the brunt of it. AUD and NZD make new year to date lows, now at 0.7148 and 0.6827 respectively.

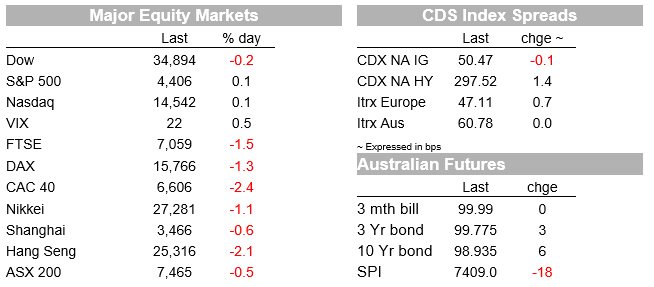

US equities have staged a recovery into the NY session with the hour power yet again providing a turn in market dynamics. Early in the overnight session, European equities ended their day with sharp losses (CAC 40 -2.43%, FTSE 100 -0.54%, Euro Stoxx 600 -1.51%). The S&P 500 opened its session with an almost instant 0.75% drop and after trading in and out of positive territory, the main US equity index managed to recover into the close, ending the day at +0.13%. The Dow closed down 0.19% while the NASDAQ was 0.11%.

While certainly a much better outcome relative to the sharp losses recorded in Europe and Asia (Nikkei -1.10%, Hang Seng -2.13, CSI 300 -0.66), a look at the S&P 500 sector performance reveals a clear shift away from pro cyclical sectors while defensive and big tech enjoyed a day of positive returns . The IT sector closed up around 1% and real estate was not too far behind up around 0.9%, meanwhile materials and industrials fell around 0.8/0.9% while the energy sector fell 2.65%. The VIX index which ended last week with a 15 handle, traded to an intraday high of 24.74, before closing the day at 21.59. Still below its one year average of 22.11, but a decent weekly jump none the less.

What has caused this broad U turn in sentiment? Well, some are pointing to the FOMC Minutes as the main culprit, but if anyone has been listening to the round of Fed speakers recently, it shouldn’t be any surprise that the Fed has been gearing up to make an imminent QE tapering announcement for quite some time now. Perhaps the best one can say is that the Minutes were the straw that broke the camel’s back. Instead we would attribute heightening concerns over the global growth outlook as the main casue for the turn in sentiment , recent softer than expected Chinese economic data along with lockdowns/activity restrictions around the globe due to a rise in delta infections have been simmering for sometime now, China regulatory/credit tightening drive has not helped either. Against this backdrop the recent acceleration in the decline of key commodity prices, appears to have spooked the broader market with yesterday’s news of supply constraint forcing Toyota’s to slash its production plans adding to concerns over activity decline and inflationary pressures too ( more below).

Copper fell to its lowest price since April ($8,894.00,) down 1.92% on the day and heading for its worst week in two months. Meanwhile oil prices fell for a sixth day in a row to the lowest level since May , WTI is down 2.66% while Brent is 2.45%. Metal prices are down 1.70% in index terms and iron ore futures in Singapore tumbled as much as 10% yesterday before eventually retracing around half that move. Iron ore prices are more than 20% lower this month with factors, including Chinese steel production curbs as the authorities seek to reduce pollution exacerbating the decline in the bulk commodity.

Yesterday the Nikkei reported that Toyota expects to reduce production by 40% in September due to the shortage of semiconductors and Covid-related production disruptions in South-East Asia. Supply-chain disruptions, partly stemming from the havoc being wrecked by the Delta variant, look set to stay with us for some time yet. Toyota’s share price slumped more than 4%.

Against this backdrop is not surprising to see the USD extending its recent ascendency, up another 0.50% in index terms over the past 24 hours. DYX now trades at 0.9356 while BBDXY is at 1157.54. Risk aversion in the air has buoyed the greenback with pro-growth currencies bearing the brunt of it. The NZD (-0.8%) and AUD (-1.1%) have made fresh year-to-date lows overnight – the NZD 0.6809 and the AUD below 0.7142. The AUD now trades at 0.7147 and NZD is at 0.6839.

NOK and CAD have fair worst, reflecting the sharper decline in oil prices while the former showed little sensitivity to the Norges Bank signalling its intentions to hike its policy rate next month, as expect by most analysts. The safe haven JPY and Swiss franc have fared the best, down just 0.05% and 0.16% respectively, while the EUR is down a modest 0.28%, albeit to its lowest level since November, at 1.1676.

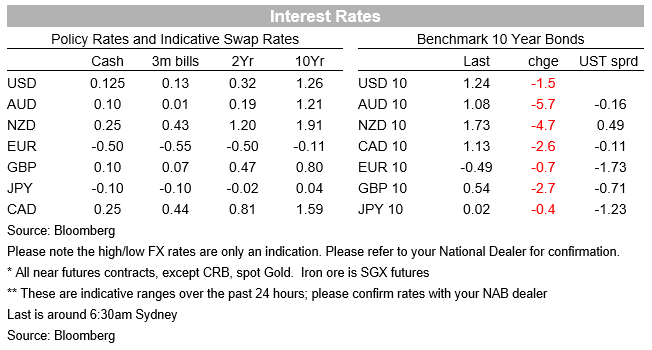

Moves in core global yields have been more subdued relative to other markets. The US 10-year rate has dipped 2bps, to 1.24%, and remains stuck within its one-month range. German Bunds are 1bps lower at -0.489% and after a sharp rise in price yesterday, AU Bond futures traded sideways for most of the NY session, now at 98.935 ( 1.065% in yield).

Lastly in Covid news, an Oxford University study on vaccine efficacy has gained some attention over the past 24 hours. Researchers found that Pfizer’s vaccine lost protection against symptomatic infection at a quicker pace than the AstraZeneca vaccine, falling from 92% effectiveness 14 days after the second shot to 78% after three months, with the trajectory suggesting further falls from this point. A recent study in Israel found the Pfizer vaccine was only 41% effective at preventing symptomatic infection in June and July. Furthermore, the Oxford researchers found that vaccinated people which did contract the Delta variant had viral loads as high as the unvaccinated, suggesting they are still just as likely to pass it on. The researchers pointed out that the vaccine still appears to be doing its job in preventing serious illness, which is clearly crucial.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.