NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Reopening and vaccines are helping economies, but the Delta variant is still a concern for markets says NAB’s Rodrigo Catril, explaining today’s sideways moves.

https://soundcloud.com/user-291029717/confidence-rising-but-so-is-the-delta-strain?in=user-291029717/sets/the-morning-call

US and EU equities have eked out small gains in the overnight session supported by solid data releases. Meanwhile, core yields remain confined to recent tight ranges while the USD is broadly stronger with commodity linked currencies the notable underperformers, notwithstanding higher commodity prices and positive risk backdrop. ECB President Lagarde talks up the Bank’s green ambition, aiming for a green capital markets union (CMU) that transcends national borders.

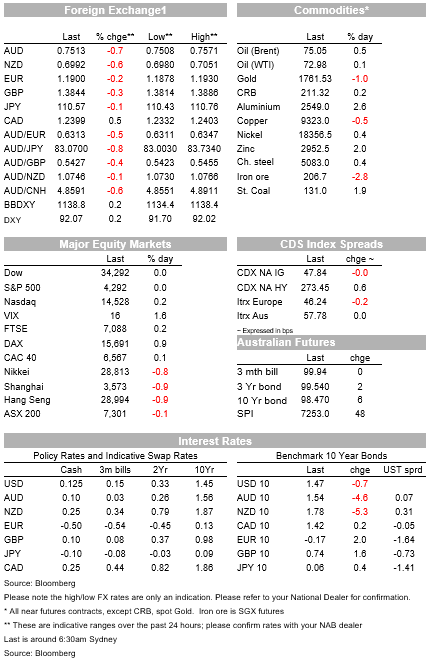

After a positive start, followed by a brief period in the red, the S&P 500 has managed to end the day marginally higher, closing at 0.03%. Another record high and still on track to close a fifth straight monthly advance. Technology (+0.70%) and Consumer Discretionary (0.23%) led the gains while financial were among the underperformers despite announcements after the bell yesterday by many US banks of higher dividend payments and buy backs. The NASDAQ closed +0.19% and the Dow was 0.03%.

European equities enjoyed a better night with all main regional indices closing with gains between 0.16% and 1.04%. The Stoxx Europe 600 Index climbed 0.3% with Chemicals (+0.9%) and cyclical sectors like automotive (+0.8%) and energy (+0.7%) leading the charge.

Strong data releases supported the risk positive vibes within equities. The Conference Board measure of US consumer confidence surged to a fresh pandemic high and well above expectations and its long-term average. The headline index surged to 127.3 from revised 120 (prev.117.2) and 119 forecast, the new reading is now close its pre pandemic average after basing around 85. Furthermore, the closely watched difference between jobs-plentiful and jobs-hard-to-get indicators rose to a 21-year high, indicative of a very tight labour market, but yet to be reflected by the official labour market figures.

Not to be undone, Euro area economic confidence – a mix of consumer and business confidence – rose to its highest level in 21 years, a stronger result than expected. The data are consistent with a strong economic rebound as lockdown restrictions ease and activity returns to normal. The vaccine rollout story also playing an important role. After a very slow start, EU vaccine numbers are now getting traction with the share of the population fully vaccinated up to 35.1% in Germany, 33.0% in Belgium, 34% in Spain and 28.8% in France. Hungary at 50.1%. EU still not up to UK (47.8%) and the US (45.8%) but rising to a degree of critical mass, opening the door toward the next less restricted phase of growth.

Worth noting too that both the WSJ and FT headline their websites with “US home-price growth hits highest level in more than 30 years”, based on the S&P-Case-Shiller index rising by 14.6% y/y Meanwhile UK house price inflation rose to a 17-year high of 13.4%. The common factor here, of course, is central bank monetary policy which has taken rates down to near-zero and fuelled widespread asset price inflation. The issue of affordability is also part of the discussion and debate that needs to be had along with concerns over potential financial stability impact.

It has been another moribund session in core global yields showing little reaction to the solid flow of data releases. 10y UST yields are little changed at 1.4782% while in Europe 10y Bunds edged up a little with the 10y tenor +2bps to -0.17%.

Moving onto FX, it is a bit surprising to see the USD broadly stronger with JPY, a safe-haven currency, the only pair stronger than the USD. USD/JPY currently trades at ¥110.53 (+0.1%) over the past 24 hours while USD indices are up close to 0.20%.

Commodity linked currencies are the notable underperformers despite higher commodity prices and a positive risk backdrop . The AUD is at the bottom of the pile, down 0.75% and now trading close to its intraday lows at 0.7512. NZD is not too far behind, down 0.63% and trading at 0.6992. All this against a backdrop of a fifth consecutive daily gain in Bloomberg’s commodity price index. Concerns over the spread of the covid Delta variant around the globe and specially among countries with low vaccination rates is a potential factor weighing on risk sensitive currencies like the AUD and NZD, that said measures of risk sentiment would suggest otherwise. Indeed, from a fundamental basis, our AUD and NZD models which include risk measures suggest both antipodean currencies are undervalued.

Month end rebalancing flows may also be at play, but with US equities outperforming in June and in the quarter, the bias would be for USD selling rather than buying. Maybe that is a theme to watch for today, given today is the last day of June.

Lastly, but still very importantly, overnight ECB President Lagarde Lagarde spoke at the Brussels Economic Forum talking about financing a green and digital recovery. The President noted that 70% of Europeans are in favour of stricter government measures to fight climate change adding that the ECB needs to invest around EUR 330bn every year by 2030 to achieve Europe’s climate and energy targets and an extra EUR 125bn every year to carry out digital transformation. ECB wants to match NGEU (recovery fund) with a green capital markets union (CMU) that transcends national borders.

Major Central Banks around the globe are looking at climate change very closely and thinking about the role they can play to help this process. The ECB looks to be taking a leading role and if Lagarde’s initiative finds support, the ECB could play a significant role on the EU green credentials and green led growth. See here for more.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.