We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

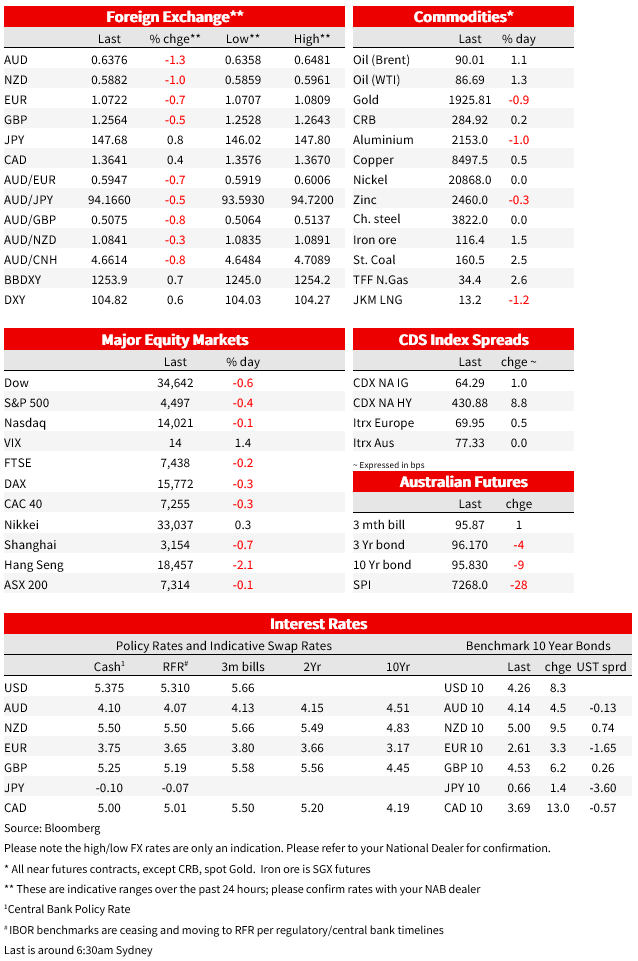

A softer Caixin Services PMI soured the mood yesterday, with the USD broadly stronger and the AUD the worst G10 performer

“Got me on repeat, got me on repeat

Got me on repeat, got me on repeat

Got me on repeat, got me on repeat” – Charli XCX

A softer Caixin Services PMI soured the mood yesterday, with the USD broadly stronger and the AUD the worst G10 performer. US yields were 8-9bp higher across the curve, with a deluge of corporate issuance on Tuesday a factor. The RBA was on hold as widely expected, with the post meeting statement a substantive repeat of the previous iteration. The RBA sees a path where they have done enough, but ‘some further tightening’ may be required and they are watching the data.

The Caixin Services PMI followed the official Services PMI last Thursday in showing a loss of momentum in the services sector even as some stabilisation emerged in manufacturing and construction. The Caixin Services PMI fell to 51.8 from 54.1, undershooting expectations for a fall to 53.5 and the weakest since December.

Chinese equities underperformed, the Hang Seng was 2.1% lower, while the CSI300 lost 0.7%. US equities were also lower, the S&P500 down 0.4% q/q, while the NASDAQ lost just 0.1%. Declines in the US were led by Materials and Industrials, while Energy managed a 0.5% gain.

The yuan weakened and the USD saw broad-based strength, with Asian-Pacific currencies once again at the vanguard. USD/CNH is up 0.4% to 7.304, not far off its intraday high of 7.3117, shy of last month’s peak just under 7.35. The USD gained 0.6% on the DXY to its highest level since March, while the NZD, AUD and JPY all fell to fresh lows for the year. The AUD was as low as 0.6358 overnight, and is currently around 0.6376. down 1.2%. The AUD was off around 0.6% ahead of the RBA and alongside weakness in the yuan, before another move lower alongside broad USD weakness, the as-expected RBA coming and going with little reaction. USD/JPY is near its highs for the day around 147.70. European currencies are weaker as well, with EUR down 0.7% to 1.0722

US yields were also higher, up 8-9bp across the curve. Fed headlines were mixed, with Fed Governor Waller saying that “there is nothing that is saying we need to do anything imminent anytime soon,” and that “we can just sit there and wait for the data.” He noted that “the data last week clearly showed the job market is starting to soften,” but there needs to be “ a couple of months continuing along this trajectory before I say we’re done.” Those comments contrasted Cleveland’s Mester who remained hawkish, saying “I can well imagine, from what I see so far, that we might have to go a bit higher.” Just 2bps of hikes priced for September and another hike by November given about a 40% chance.

A more likely culprit for the push higher in yields on the day then is a deluge of investment-grade bond sales. Nearly US$37bn of corporate issuance that happened overnight and data compiled by Bloomberg suggests Tuesday was shaping up to be the busiest day of issuance since 3 January. European yields (having sold off the previous day whilst Treasuries were closed) generally showed more modest yield moves but were near-universally higher.

Oil was higher, with Brent and WTI both up over 1% and Brent back around US$90 a barrel for the first time since November. Saudi Arabia announced it will continue its unilateral production cutback of 1 million barrels a day, first introduced in July, until December. Russia also announced an extension of the country’s 300,000 barrels a day export reduction.

As for the detail of the RBA yesterday, the Board left the official cash rate unchanged at 4.1% for the third successive month. The key final paragraph retained the guidance that “some further tightening of monetary policy may be required.” In fact, the final paragraph was unchanged apart from the addition of ‘to continue’ in “that will continue to depend upon the data and the evolving assessment of risks.” The rest of the statement also saw very few changes.

Overall, the Board remains hopeful they have done enough, but retain a modest tightening bias and will be watching the data to determine if they need to act on that bias. Market pricing is for another hold in October and just a 30% chance of a hike in November, little changed from prior meeting.

Of some note and despite concern in some circles that a lower AUD would the RBA higher, there was no mention of the currency in the statement. But a key driver of pressure on the AUD, a weaker China, did warrant a mention on its own merit with “increased uncertainty around the outlook for the Chinese economy ” added to a list of concerns. After yesterday’s moves, the AUD is around 3% lower than assumed at the August SoMP against the US dollar, but just 1.5% on a trade-weighted basis. With pressure on the AUD alongside weakness in other Asian currencies and driven by a deteriorating outlook in our largest trading partner, the read through from softer AUDUSD to upward pressure on the policy rate is smaller than it would be otherwise. Even still, the combination of higher oil and a lower AUD certainly add to headline inflation pressure in the near term, and the RBA is getting little help from the exchange rate channel.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.