Online retail sales growth slowed in May following a fairly strong April

Insight

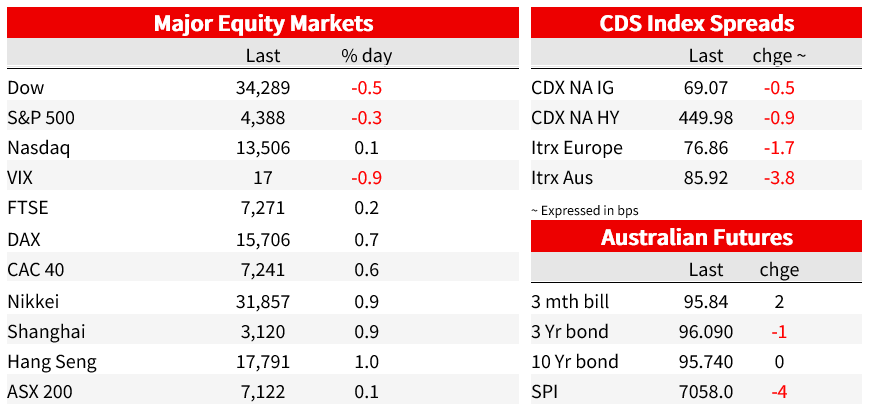

US equities traded in and out of positive territory, essentially marking time ahead of NVIDIA’s reporting tomorrow and Fed Chair Powell’s speech on Friday. It was also a quiet FX session while in rates 10y UST yields printed a fresh 16-year high before consolidating.

Events Round-Up

US: Existing home sales (m/m%), Jul: -2.2 vs. -0.2 exp.

US equities have traded in and out of positive territory, essentially marking time ahead of NVIDIA’s reporting tomorrow and Fed Chair Powell’s speech on Friday. 10y UST yields printed a fresh 16-year high before consolidating with the curve showing a flattening bias. FX moves have also been relatively subdued with the USD little changed. Modest gains in JPY and antipodean pairs have been offset by weakness in European FX.

US equities struggled for direction amid a lack of news flow and light summer trading. The S&P 500 closed 0.28% lower while the NASDAQ ended the day essentially unchanged (0.06%). Investors are seemingly on a wait and see mode ahead of the NVIDIA result due out after the bell tomorrow (NVIDIA’s share fell over 2%). The consensus view expects NVDIA second-quarter revenue to exceed the company’s forecast given three months ago. But at the same time there are some concerns the chipmaker may have experienced supply constraints against what it seems to be an unquenchable demand for its products. NVIDIA’s performance is seen by many as a potential bellwether for the IT sector and markets in general.

Looking at the S&P sector performance, Financials were the underperformers, down 0.88% not helped by news S&P Global Ratings joined Moody’s Investors Service in cutting some US lenders amid a “tough” climate. Of note too, news from retailers may be signalling at the emergence of a new consumer weakening trend, Dick’s Sporting Goods reported weaker sales than expected and excess inventory. Macy’s reported negative sales growth and rising delinquencies in credit-card payments. Both companies noted rising theft of merchandise, a sign of the times.

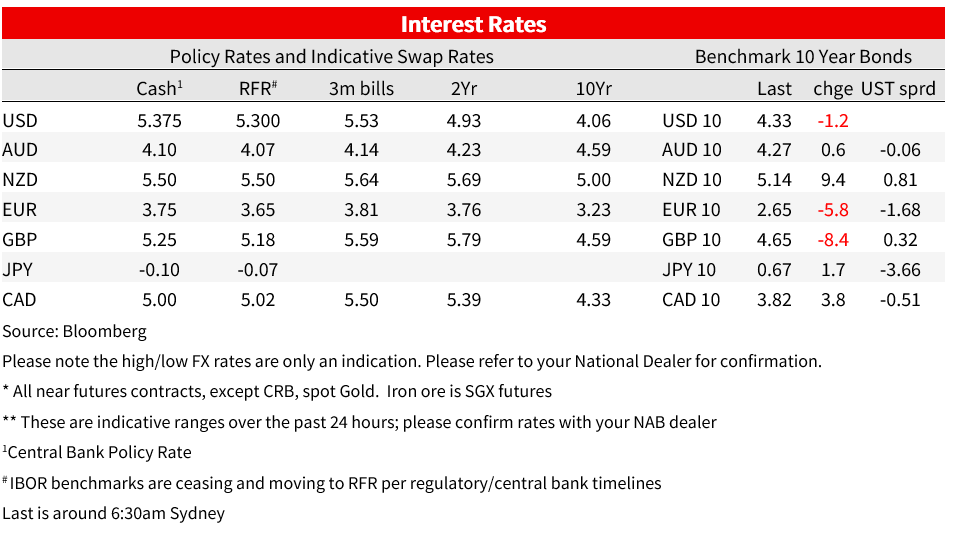

10y UST yields traded to a fresh 16-year high (4.3599%), before consolidating. The 2Y UST yield closed 3bp higher at 5.03% with the 2Y/10Y curve showing a flattening bias, back below -70bp with the 10y yield easing back towards 4.33%. Meanwhile in Europe, 10y Bunds and Gilts outperformed, falling by 6bp and 8.5bp respectively to 4.637% and 2.640%

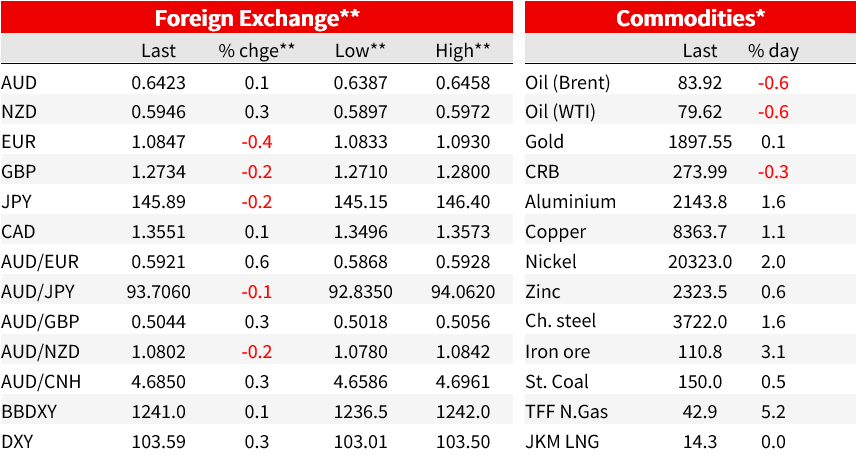

Moving onto FX, yesterday the PBoC set the CNY fix at its strongest rate relative to market estimates since Bloomberg began the daily survey in 2018 and has engineered a funding squeeze to make it more expensive to short the yuan. After all these efforts, USD/CNH still traded higher (0.24% to 7.3067), with fundamental drivers (weak economy, capital outflows, wider US-CH rate spreads) dominating and suggesting Beijing efforts are more about arresting the speed of CNY/CNH decline, rather than kick starting a new appreciating trend.

The USD is little changed in index terms (BBDXY and DXY are 0.05/7% higher) with modest outperformance from JPY and antipodean pairs offset by European FX weakness. The Kiwi is at the top of the leader board up 0.3% over the past 24 hours and starts the new day just below the 0.60 mark (0.5946). Wider NZ-global rate spreads might be providing some support with my BNZ colleague Jason Wong noting the underperformance of the domestic’s rates market ( higher yields) reflecting a lack of appetite for domestic government debt as well as an aggressive RBNZ outlook with the market suggesting another RBNZ rate hike is seen more likely than for the Fed or RBA, despite the RBNZ’s “conviction” that it has done enough to bring inflation down, especially with the economy mired in recession, while both Australia and the US have much stronger relative economies, and Australia’s real policy rate is barely positive.

The AUD also managed to edge higher over the past 24 hours, trading to an overnight high of 0.6458, before easing back down to 0.6423 were it currently trades (up 0.2%). So little changed relative to Sydney closing levels yesterday. China’s economic outlook remains the big swing factor for the AUD with risk sentiment now emerging as another influence given recent wobble in the US equity market.

EUR (-0.4% to 1.0847) and GBP (-0.15% to 1.2732) have been on the soft side of the ledger with the former not helped by another uptick in European gas prices . TTF futures rose as much as 9.9% after settling at a two-month high in the previous session amid heightened supply concerns. Norway said that seasonal works at the giant Troll field, previously scheduled to continue past the summer season, are now going to extend further to October 16. Meanwhile the market awaits the outcome of Woodside workers decision to strike unless they reach an agreement during scheduled talks on Wednesday. Staff at some Chevron’s facilities are also considering walkouts.

Finally for the record, in terms of economic data releases. US existing home sales fell a greater than expected 2.2% m/m in July, taking the level of sales back near the cycle low. The lack of sales reflects a lack of inventory, as homeowners are reluctant to shift, which would result in them needing to refinance their mortgage rate at a much higher level.

Coming Up:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.