Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Demand is outstripping supply on both sides of the Atlantic.

https://soundcloud.com/user-291029717/demand-beating-supply-inflation-anyone?in=user-291029717/sets/the-morning-call

‘Cause you’re hot then you’re cold. You’re yes then you’re no

You’re in and you’re out. You’re up and you’re down – Katy Perry

Hot and cold was the main theme from the price action overnight. The ISM manufacturing was a big miss (cold), but details in the report showed supply and inflationary pressures continue to intensify (hot). After closing lower on Friday, US and European equity markets have began the new month on a positive note (hot), although the NASDAQ is a notable laggard (cold). The ISM miss weighed on UST yields (cold), but the breakeven component rose (hot) and the USD is weaker(cold) across the board with NZD (hot) leading the way.

Against expectations for a small uptick, the April ISM Manufacturing index printed 4.7 point lower at 60.7 , defying signals from regional surveys which pointed to the potential for the headline number to edge a little bit higher. Notably, the decline in the ISM index was not due to an ease in demand, indeed it was the opposite with purchasing managers reporting that their companies and suppliers “continue to struggle to meet increasing rates of demand due to coronavirus impacts limiting availability of parts and materials”. Order backlogs are up to their highest level in more than forty years, while the prices paid index is at a more than decade high, consistent with rising inflationary pressure. Some commentators have also noted how China’s PMI numbers tend to lead the ISM and with China activity readings peaking a few months ago and ease in the ISM numbers was only a matter of time, the new order subindex fell 3.7 points to 63.7, so still at a very high level, but consistent with the China narrative.

The final reading for the euro area manufacturing PMI was revised down slightly from the flash estimate, but at 62.9 in April it was still at its highest level in the 24-year history of the survey. Like the US survey, the message was one of demand running ahead of supply and widespread and high inflationary pressure.

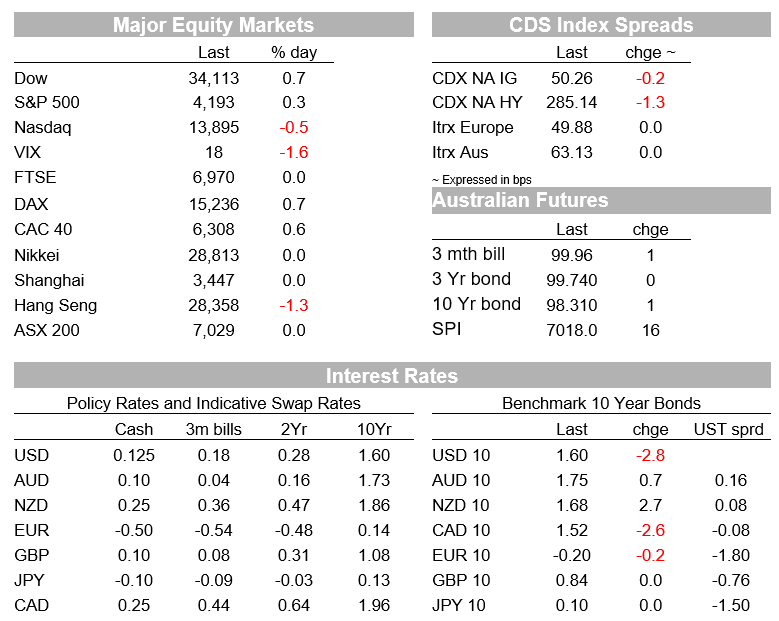

European and US equity markets began the new month on a positive note with the underwhelming PMI/ISM releases only eliciting a small negative reaction . All major European indices ended the day in positive territory with the Stoxx 600 index gaining 0.58%. After opening higher, gaining close to 0.7% in the first half hour of trading, the S&P 500 lost its mojo following the ISM release, but still managed to end the day +0.27%. The NASDAQ was a notable laggard, falling 0.48% with big tech stocks Facebook, Amazon and Netflix weighing on the IT heavy index.

While not necessarily saying anything new, soothing Fed words may have helped ease some of the ISM disappointment . Fed Chair Powell said Monday that while the US economic recovery is “making real progress,” gains have been uneven following a downturn that cut hard along lines of race and income. Meanwhile Fed Williams noted that current conditions are “not nearly enough” for a shift in the policy stance.

Reaction to the ISM miss was more pronounced and interesting the UST market. The release of the survey triggered a rally in the 10y with the benchmark yield falling from an intraday high of 1.6527% to a low of 1.5763%, recovering to 1.5976% where it currently trades . Looking at the component of the nominal yield the ~5bps decline was made up by an 8bps decline in the real yield to -0.83% while the breakeven component climbed 3bps to 2.4250%. So, the ease in activity and inflationary pressures revealed in the ISM survey were clearly not missed by the UST market.

Before moving to currencies, overnight the US Treasury announced its expectations to borrow $463bn in April through June, this is an increase of about $368bn compared to the numbers projected in February, when it expected $95 billion in net marketable debt issuance over the quarter.

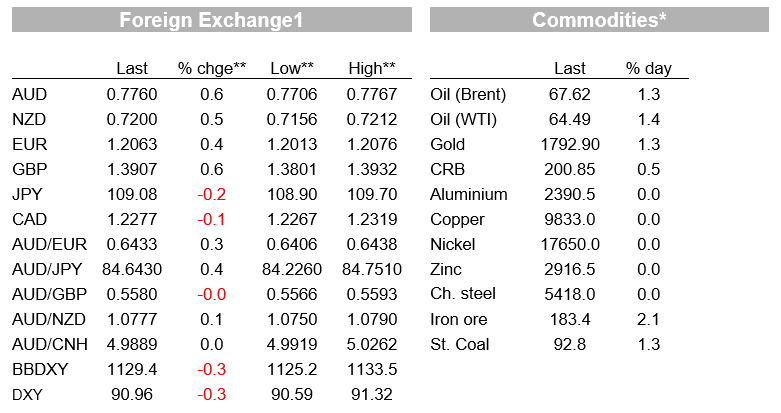

Consistent with a decline in real UST yields, the USD shows broadly based losses, with both the DXY and BBDXY indices down ~0.35%. NZD has led the USD gains within G10, up 0.67% over the past 24 hours. After its Friday decline, the kiwi is trying to get back above the 72c mark and currently trades at 0.7198.

Yesterday during our APAC session, the AUD tested levels in the low 77’s, a support area that has proven to be reliable in recent weeks. The AUD now trades at 0.7762, around the middle of the 0.7698 to 0.7818 range held since mid-April.

Looking at other currency pairs, GBP has started May on a positive note, at least initially defying an apparent seasonal pattern which has seen the currency down for the month of May for the past eleven years straight. GBP is up 0.6% to regain the 1.39 handle. EUR, JPY and CAD show more modest gains.

Finally on some good news for European tourist, the European Commission said it’s “time to revive the EU tourism industry and for cross-border friendships to rekindle — safely,”. The Commission recommended welcoming visitors from countries with relatively low infection rates as well as those who are fully vaccinated. The proposals require approval from a weighted majority of the bloc’s 27 member states and could be adopted as soon as the end of May.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.