Markets Today: Does the US jobs shortfall vindicate the Fed’s cautious approach?

US non-farm payrolls markedly undershot market expectations on Friday with just 266k more people in work versus the expectation of close to one million.

US Payrolls disappoints sharply at 266k v. 1m expected, still 8.2m below pre-pandemic

Fuels expectations the Fed will stick to its ultra-accommodative stance for longer

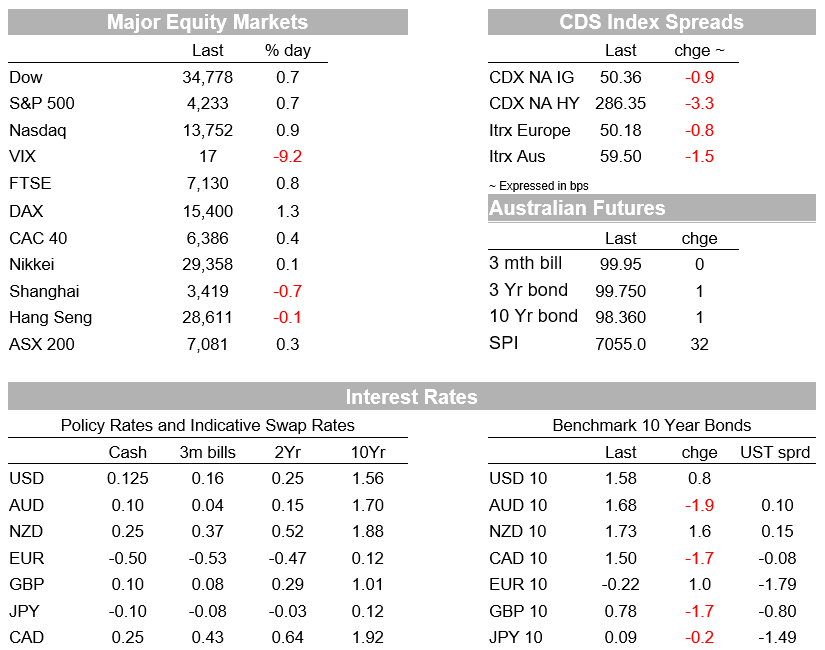

Equities lift on a lower for longer view with the S&P500 +0.7% and NASDAQ +0.9%

Yield curve steepens, 10yr swings sharply, while inflation breakeven lifts to 2.50%

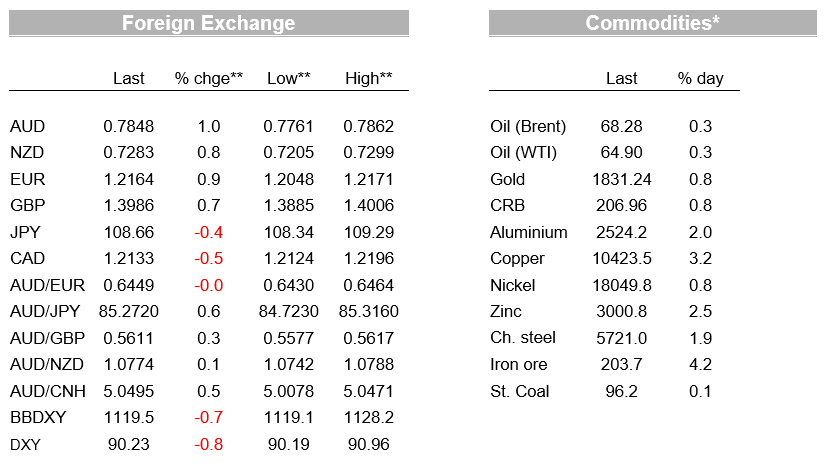

USD falls (BBDXY -0.7%), decline in real yields doesn’t help, AUD (+1.0%) outperforms

This week: AU Budget, US CPI & Retail, CH Aggregate Financing and CPI/PPI, Fed speak

Coming up today: AU Retail & NAB Survey, CH Aggregate Financing, Fed’s Evans

“But I don’t feel like dancin’, no sir, no dancin’ today; Don’t feel like dancin’, dancin’; Even if I find nothin’ better to do; Don’t feel like dancin’, dancin’”, Scissor Sisters (2006)

Friday was all about Payrolls with a disappointing print (266k vs. 1m expected) providing further ammunition for the Fed doves to keep policy ultra-accommodative. The weekend was all about digesting the implications with opinion divided on whether fiscal stimulus is acting as a disincentive for people to seek work, or whether a slower recovery in the labour market warrants more stimulus. Markets so far have taken it as supporting a lower for longer view with equities lifting to new record highs (S&P500 +0.7% on Friday and 1.2% for the week). Yields were volatile in the wake of the report with the US 10yr falling to as low as 1.49%, before more than fully reversing to be up 0.8bps to 1.58%. Part of the snapback in yields reflects inflation fears with the curve steepening (5yr yield -4bps, 30yr +5bps), while the 10yr implied inflation breakeven lifted to 2.50%, its highest since 2013. With nominal rates steady, real rates fell -3.9bps to -0.93%. The USD fell sharply with BBDXY -0.7%, while the AUD (+1.0%) outperformed after having underperformed for the past few weeks and opens up at 0.7848. The lower USD also lit another fire under commodities with copper at an all-time high of $10,423.

First to Payrolls. The report was a shocker with Payrolls in April of just 266k, well below the 1m consensus, while downward revisions of 78k to the past two months also added to the weak tone. The unemployment rate unexpectedly ticked up, from 6% to 6.1% against expectations of a fall to 5.8%. One area of the report which surprised to the upside was wages with average hourly earnings +0.7% m/m vs. 0.0% expected, despite the influx of traditionally lower paid leisure and hospitality workers where average earnings rose by 1.6% m/m. The lift in wages aligns with anecdotes of businesses having to pay up for labour. With the US economy continuing to re-open, payrolls should lift more strongly from here – one example is New York State which is aiming to have stores, restaurants and museums to be running near fully capacity by May 19.

As for what can explain the lacklustre rebound in jobs seen in April, opinion is very much divided along partisan lines which also likely pushes back further stimulus, including President Biden’s infrastructure plans. Republicans and the business community are citing elevated unemployment benefits as acting as a disincentive for people to work, with several states (incl. Florida, Montana and North Carolina) tightening requirements to receive enhanced unemployment benefits. Note currently those on jobless benefits get an additional $300 a week until September on top of their regular state benefit of around $318 a week. While $600 a week may not sound like much, that does result in people receiving the equivalent of $15 an hour full time, which may act as a disincentive for lower paid workers. Some employers are anecdotally stating they are willing to postpone hiring until the $300 a week top-up expires at the end of September. On the other side of the spectrum, a lacklustre rebound points to ongoing weakness in the recovery, justifying the need for stimulus and with payrolls being 8.2m below pre-pandemic levels is unlikely to be inflationary.

The reaction in markets was risk-on, with equities lifting and the USD falling sharply. The USD BBDXY fell 0.7%, its biggest one day fall since early December and is trading at its lowest level since early January. The reaction in yields, which saw implied inflation breakevens lift and real yields falls, adds to the weaker USD view – the USD’s renewed downtrend since the end of March – some 3% on a BBDXY basis – has coincided with the 30bp fall in the US 10-year real yield over that time.

The AUD outperformed, up 1.0% to 0.7848, along with EUR up 0.9% to 1.2164. The JPY underperformed (USD/JPY -0.4%) amidst the risk-on backdrop, although it was still higher on the day. The CAD was the weakest of the G-10 currencies, rising just 0.1% after a soft Canadian employment report (although this followed two exceptionally strong releases).

Finally in Australian news, JobSeeker numbers are reported to have fallen 105k in April, even as JobKeeper ended in March. To put that into perspective, only 15-20k jobs needed to see a 0.1 fall in the unemployment, which means the unemployment rate could be heading below 5% soon than expected given the unemployment is at 5.6%. As for Friday’s RBA Statement on Monetary Policy (SoMP), it shed more light on the RBA’s sharply upgraded forecasts for economic growth that were outlined in last Tuesday’s post-Meeting Statement. Our conclusion following Tuesday’s Statement was that the RBA would not extend their 3yr YCC target from the April 2024 bond to the November 2024 bond, and that the RBA would taper QE purchases in a 3rd round.

The SoMP forecasts see core inflation approach the bottom-end of the RBA’s 2-3% target band by mid-2023. Upside risks to that central forecast suggests the RBA cannot credibly extend the 3yr YCC target from the April 2024 bond to the November bond. Importantly for the outlook, the baseline unemployment rate forecast at 4½% by end 2022 (previously 5½%) is at the bottom end of model-based NAIRU estimates. The upside scenario sees the unemployment rate falling through NAIRU to 3¾% by mid-2023. The RBA has clearly fed part of the tighter labour market through to their inflation forecasts with core inflation at 2% by mid-2023 (previously 1¾%), while in the upside scenario inflation lifts to 2¼% and importantly ” remains on an upward trajectory at that point”. The other implication from the upside scenario which sees core inflation sustainably in the band in 2023, is that it potentially opens up the possibility that the RBA could hike rates earlier than their 2024 guidance, especially should inflation remain “on an upward trajectory at that point”. There had been some contention around whether YCC would prevent the RBA hiking rates earlier than 2024, but Dr Debelle clarified yesterday that “it is the state of the economy that is the key determinant of policy settings, not the calendar”.

In news over the weekend, Scottish National Party leader Nicola Sturgeon said the weekend’s Scottish election results represented a mandate for another referendum on independence from the UK. The SNP fell just short of an overall majority, but a stronger than anticipated performance by the independence-supporting Scottish Green party means there is a majority for another referendum in the Scottish parliament. The UK government still needs to agree to a referendum and PM Johnson has indicated in the past that he won’t do so. The GBP may come under some short-term pressure this morning although, with the SNP saying their immediate focus is securing the recovery from Covid-19 and the UK government likely to resist SNP wishes for a referendum, we suspect the market will move onto other drivers before long.

Coming this week

Domestic focus will be on the Federal Budget and on any debt issuance implications for the RBA’s QE program. Offshore the US CPI will dominate given the extent to which inflation pricing has lifted, while Chinese CPI/PPI will also be closely watched. Details below:

AU: Federal Budget: The underlying deficit is expected to come in much lower than projected in MYEFO given the unemployment rate at 5.6% is more than one-and-a-half percentage points lower than the 7¼% forecast in MYEFO. The iron ore price is also significantly higher at $200 a tonne, well above the forecast decline to $55 a tonne by September 2021. NAB pencils in a 2020-21 deficit of $150bn (MYEFO $197.7bn) and $80bn for 2021-22 (MYEFO $108.5bn). A lower deficit profile may also have implications for the RBA’s QE program, with Deputy Governor Debelle noting “in recent months, the RBA has often been buying bonds at a faster weekly pace” than the AOFM ” has been issuing. This is not true in some other countries, including most notably the US”.

CH: Aggregate Financing and CPI/PPI: An important week with Aggregate Financing figures due anytime in the week, along with CPI/PPI on Tuesday. There has been a lot of speculation on whether China is trying to tighten credit growth, while inflation pressures appear to be lifting on the back of commodity prices with the consensus on PPI being 6.5% y/y.

US: CPI CPI and Retail Sales: The CPI on Wednesday is expected to lift on the back of base effects with the consensus for core at 2.3% y/y, up from 1.3%, though the monthly pace will remain unchanged at 0.3% m/m. Retail Sales should continue to see a stimulus boost with sales ex auto and gas at 2.1% m/m after last month’s blockbuster 8.2%.

Coming up today

A busy day in Australia ahead of the Budget tomorrow with Retail Sales and the NAB Survey. Offshore it is very with only Chinese Aggregate Financing figures due anytime during the week. Details below:

AU: Retail Sales and NAB Survey: Quarterly retail sales will be one of the first partial indicators for Q1 GDP with the consensus for retail volumes being -0.4% q/q. The monthly retail sales number though should be well positive given the preliminary read for March was +1.4% m/m. Payrolls data is for the week ending 24 April 2021 and will continue to be watched for how the labour market is faring post JobKeeper. The NAB Business Survey is also out today and as always no hints today.

CH:Aggregate Financing – April: Potentially out anytime this week. Credit growth will be closely watched given mixed signals on a tightening in credit conditions from Beijing.

US: Fed’s Evans: The Fed’s Evans will be discussing the economy outlook. There is no text, but there will be Q&A.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.