NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

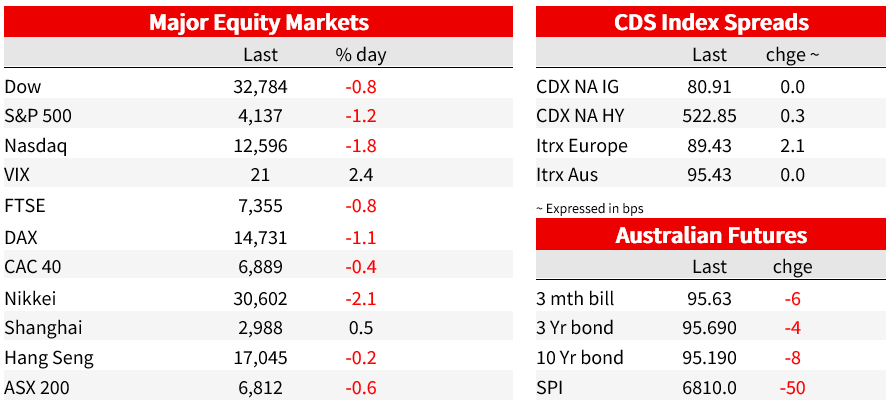

Risk sentiment remained fragile overnight with equities extending recent losses with disappointing earnings outlooks from major tech companies, despite mostly beating on current quarter earnings.

“‘Cause I’m here looking fine, babe; And I got eyes looking my way; And everybody’s on my vibe, babe”, Don’t call me up, Mabel 2017

Risk sentiment remained fragile overnight with equities extending recent losses with disappointing earnings outlooks from major tech companies, despite mostly beating on current quarter earnings. Meta noted it was seeing some advertising softness so far this quarter. The NASDAQ fell -1.8% and is now officially in correction territory after having fallen -10.9% from its mid-July high. The S&P500 fell -1.2% and is close to being in correction territory now being -9.7% away from its late-July high and has broken through its 200-day moving average. Global yields are mostly lower led by the US. The catalyst appeared to be the US GDP data which while beating was softer in the details, a good 7yr auction which bucked the trend of a run of mixed auction results recently, while the general fragile risk sentiment may also have contributed with yields generally tracking equities lower at the open.

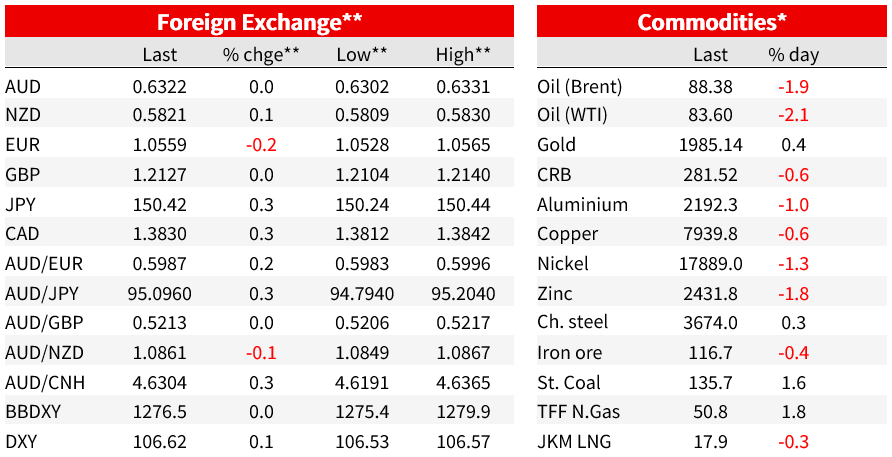

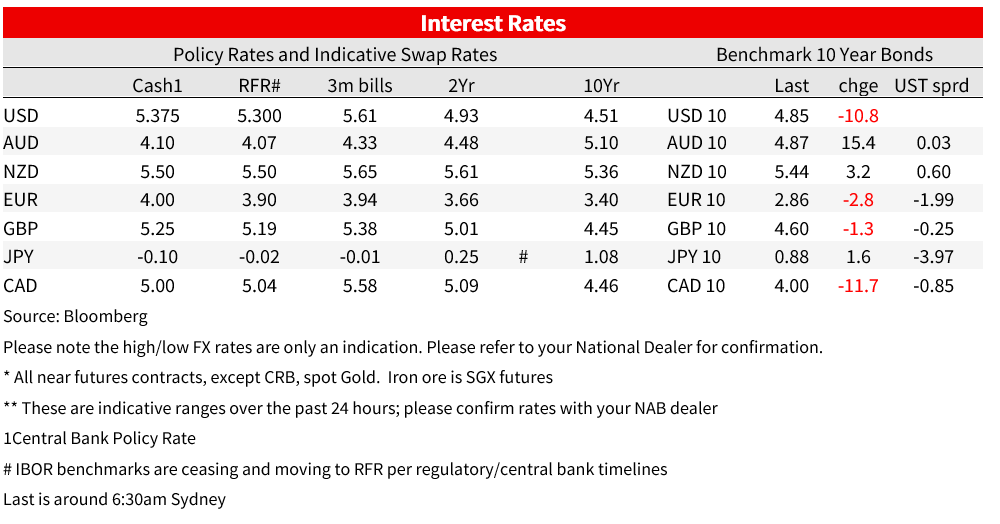

The US 10yr yield has fallen -11.3bps to 4.84% (high 4.99%; low 4.83%). The 2yr is also down -7.8bps to 5.04% (high 5.14%; low 5.02%). The moves generally continues the choppy price action of late. The US$38 billion 7-year auction saw strong demand, after a run of mixed auction results recently. US Fed Funds pricing has put some more cuts in 2024 with around 80bps worth of cuts now priced in 2024, up from 72bps worth of cuts yesterday. Most of the decline in nominal yields was reflected in real yields with the 10yr TIP -9.6bps to 2.42%. On the 7yr auction bid/cover was 2.7 from 2.47 and indirect bidding was 70.6% from 65.5%. In FX the US dollar dipped alongside the move lower in Treasury yields before paring losses with the DXY now up 0.2% with most currency pairs flat against the USD (GBP -0.0%; EUR -0.2%, USD/JPY +0.3% to 150.39). The AUD managed to claw back its losses of yesterday post Bullock testimony, with the AUD now flat at 0.6320.

First to the data. US Q4 GDP beat expectations at 4.9% annualised vs. 4.5% consensus and 2.1% previously. Growth was underpinned by strong consumer spending which rose 4.0% and added 2.7 percentage points to the GDP figure, while inventories also added 1.3 percentage points. That breakdown suggests growth in Q4 should be slower with many analysts citing the details were softer than the headline . On the inflation side some good news. The core PCE deflator rose at a 2.4% rate, a tenth below the consensus, 2.5%. The 2.4% increase in core PCE is the smallest since Q4 2019, ignoring the initial Covid distortions. There was also some other data out including US durable goods orders which jumped 4.7% m/m in September which was well above the consensus and reflected a large rise in aircraft orders. The core reading, which exclude defence and aircraft orders rose 0.6% after an upwardly revised 1.1% in August. Meanwhile jobless claims printed close to expectations at 210k vs. 207k consensus.

The ECB kept rates on hold as widely expected and there was little initial market reaction. The statement reported that interest rates are at levels that, if maintained for a sufficiently long duration, will bring inflation back to its target. That reinforced market expectations that the tightening cycle may now be finished. President Lagarde in her press conference played further to this view, noting the transmission is, “increasingly dampening demand and thereby helps push down on inflation.” The ECB said the economy remains weak, manufacturing activity continues to fall, subdued foreign demand and tighter financing conditions are increasingly weighing on investment and consumer spending. Reinvestments from the pandemic emergency purchase programme (PEPP) will run until at least the end of 2024. There was also speculation overnight whether Japan was intervening with USD/JPY trading up to 150.80 before dropping close to a big-figure in a matter of seconds but has since recovered. Finance minister Suzuki that he was ‘watching FX moves with the same sense of urgency’. If BoJ/MoF were worried by Yen weakness, ending or widening YCC would be a better policy in your scribe’s view – note BoJ meets next week.

In Australia yesterday, RBA Governor Bullock presented a clam demeanour in front of the Senate Economics Committee, not willing to be drawn into discussing the implications of yesterday’s CPI print to the RBA’s forecasts. This was expected given the RBA staff have yet to update their forecasts, and the Governor would not have wanted to pre-judge the decision by the RBA Board. The commentary provided was similar to the more hawkish remarks she gave earlier this week and last week and we do not see these remarks as being materially different. There was some confusion in markets regarding this quote, which wasn’t picked up well by the red headlines that traders use in Bloomberg or Reuters: “ the print came out a little higher than we’d been forecasting at our August SoMP…but it was pretty much where we thought it would come out given the information we’d come into since then, particularly the monthly CPI indicator, so we thought it was going to be about where it came out”.

To your scribe it appeared the nuance given by Bullock was not picked up, but also perhaps markets were anticipating a clearer statement on yesterday’s CPI which was too hopeful. In the evening around 8.00pm the Herald Sun’s RBA Whisperer was out arguing that “There is no need for an emergency rate hike. There won’t be one” which was in the author’s opinion rather than in the vein of informal messaging (see Herald Sun: No need to race to rate hike on Cup Day ). In contrast the AFRs RBA Whisperer Kehoe has been on the hawkish side. As we noted in our write-up of Bullock, the CPI outcome, combined with our expectation for Q4, sees our end 2023 trimmed mean forecast of 4.4% y/y being five tenths above the RBA’s August SoMP forecast for 3.9% y/y. RBA Governor Bullock said on Tuesday that “the Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation” and it is hard not to see that result meeting that bar (see NAB note AUS: RBA’s Bullock: yet to feed CPI through to the forecasts).

Coming up:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.