NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Ukraine/Russia tensions continue, no further military escalation apart from cyberattacks

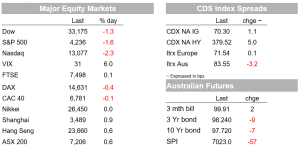

Geopolitical tensions continue to dominate. Markets were broadly steady overnight given there was no further military escalation, but escalation fears remain. Ukraine reported it had suffered from cyberattacks overnight, Russia has begun evacuating its embassy in Kyiv, while a senior US defence official notes Russia has moved nearly 100% of forces into attack position and warns an offensive could begin within 48 hours. Against that backdrop market moves have been contained. The S&P500 is down by -1.6% as we head into the last hour of power, yields have inched higher with the US 10yr Treasury +4bps to 1.98%, while oil prices are broadly steady with Brent at $96.79. FX continues to be an unusual sea of calm with the USD broadly steady (DXY +0.1%) and the AUD (+0.3%) and NZD (+0.5%) outperforming with higher commodity prices seemingly outweighing risk sentiment. One factor assisting the calm has been the limited ‘light-touch’ sanctions imposed by the US and its NATO allies, though of course further sanctions will depend on what Russia does next.

For markets, Russia/Ukraine tensions bring both a possible demand shock (for Europe), and more importantly a much larger a supply shock for the rest of the world given the importance of Russia and Ukraine to energy, hard commodities and soft commodities. In the UK BoE MPC members have been talking to the issue with Governor Bailey noting the sharp lift in oil and gas prices so far will add at least £700 to the average UK household energy bill and warned of an even tighter living standard squeeze due to the escalating crisis in Ukraine. External MPC member Haskel noted the material upside risk of further increases in global gas prices, adding to the already considerable rise in CPI inflation. The ECB has also asked banks for stress-tests on their Russian exposures, looking at liquidity, loan books, trading and currency positions.

While market moves have been contained, it is worth highlighting two points: (1) The Russia/Ukraine situation has not greatly impacted US Fed rate hike pricing with 6.5 rate hikes still priced in 2022, while a 50bps move in March is around a 40% chance – the decision not to move by 50bps by the RBNZ yesterday and BoE early in the month all suggests central banks don’t want to spook the horses too much in the early part of the tightening cycle. A supply shock to commodities and the need for a higher geopolitical risk premium though may mean inflation remains elevated for longer with the risk the hiking cycle may need to be steeper; and (2) recession fears are likely to build if central banks respond to supply driven inflation as demand eases. On this point it is worth noting US 1Y1Y OIS is at 2.05%, 2Y1Y OIS is 1.93% and 3Y1Y OIS is 1.79%. The 2s5s curve has flattened immensely over recent months and is currently sitting at 29.2bps.

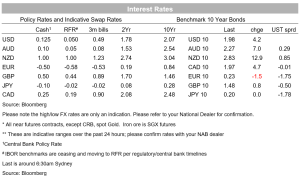

Across the ditch in NZ the RBNZ’s 25bp hike was much more hawkish than the headline. The terminal rate forecast in the MPS was revised significantly higher to around 3.35% from 2.60%, while the Bank also said it was happy to move by 50bp increments in the future (“The Committee also affirmed that it was willing to move the OCR in larger increments if required over coming quarters ”) and that the decision to move by 25bps at this meeting was “finely balanced” against a 50bps move. (see RBNZ: More tightening needed for details). My BNZ colleagues noted in their write-up that the RBNZ only has annual inflation returning to the mid-point of its target band in March 2025, meaning only a weak economy will deter the RBNZ from its published course of action if it results in the labour market softening substantially and inflation abating.

NZ markets were wrongfooted going into the meeting, pricing terminal rate closer to 3%, and yields leapt in response. The 2-year swap rate rose 11bps post-RBNZ with the 24 hour move +14bps to 2.70%. The curve flattened with 5-year swap +10bps to 2.95% and 10yr +8bps to 2.99%. The market sell-off saw market pricing for a 50bps move at the next meeting in April increasing to 65%. The NZD also rose up 0.7%. Additionally, the RBNZ announced Quantitative Tightening with agreement to directly sell government bonds to the DMO at a rate of $5 billion per fiscal year, commencing in July 2022. This came as no surprise and the upward movement in NZGB yields for the day wasn’t significantly out of line with swap rates – 10-year NZGB rose 9bps to 2.79% against the 8bp move in swaps.

Finally in Australia, yesterday’s wages number failed to provide the smoking gun for rate hikes as early as June. Headline wages growth was 0.7% q/q and 2.3% y/y, broadly in line with the gradual progress expected by the RBA in its latest SoMP. Governor Lowe had previously indicating such progress was consistent with considering a rate hike later in the year, which was interpreted as being August at the earliest. Note the wages measure including bonuses was a bit hotter at 1.1% q/q and 3.0% y/y. Media with close contacts to Martin Place emphasised the data will reinforce the RBA’s base case, illustrating Australia is different to the US, and that Governor Lowe will remain patient (see AFR: Wages not a trigger for RBA interest rate rises). That patience of course is bounded by the degree of tolerance the RBA has for having inflation running outside of the target and NAB continues to see the risk of inflation again printing substantially higher than what the RBA has projected. Market pricing for the RBA is little changed.

Fairly quiet domestically with only the ABS Capex Survey. Offshore it the calendar is full of central bank speak. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.