Online retail sales growth slowed in May following a fairly strong April

Insight

Bailey in Washington says bond purchases will end as scheduled on Friday

“Should I stay or should I go now?

If I go, there will be trouble

And if I stay it will be double

So come on and let me know” – The Clash

Its been a story of thirds over the past 24 hours. Yesterday’s risk aversion extended into the Asian session before US equities turned higher and the USD more than reversed earlier gains overnight. That was until tough talk from Bailey in the last couple of hours saw that recovery reverse. All said, the dollar is a little higher, US 10yr yields are up 5bp to 3.93%, and equities are lower. The BoE has been in the driving seat, with the earlier announcement of another market intervention to protect financial stability helping calm bond markets, before Governor Bailey’s warning that pension funds have ‘three days left’ renewed the risk off tone.

The Bank of England and the UK gilts market were again in focus over the past 24 hours. The Bank of England extended support targeted at pension funds for the second day in a row, this time offering to buy up to £5b a day of inflation-linked government bonds, out of the expanded £10b daily envelope announced the previous day. The Bank warned that “the prospect of self-reinforcing ‘fire sale’ dynamics pose a material risk to U.K. financial stability. ” It marked the first time the BoE has purchased inflation linked debt. On the day, the BoE ended up buying just £1.95b of inflation-indexed gilts and £1.35b of gilts. Speaking in Washington in the US afternoon, Governor Bailey dampened hopes the BoE may have a longer presence in markets. He told pension funds “You’ve got three days left … You’ve got to get this done.” Saying that the window to act would indeed end 14 October and that intervention in markets is temporary. The Chancellor is expected to reveal borrowing plans on Oct. 31.

Not providing any breathing space of the Bank of England in its fight against inflation, UK employment data suggests a still robust labour market despite the mounting headwinds to the outlook. Payrolled employees rose 69k in September, outpacing the expected 35k gain, while the 3m jobless rate fell to 3.5%, the lowest since 1974.

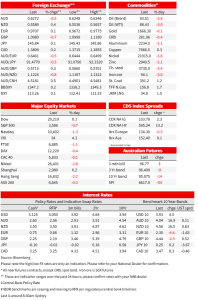

The 10yr gilt yields was 3bp lower at 4.44%, though the yield on 30yr gilts was 12bp higher to 4.79%. The US 10yr yield was trading above 4.0% late in the local session yesterday but has fallen back to close around 3.93% – well above the intraday yield low of 3.87%.

In currencies, the DXY initially extended its strength, appreciating to 113.50 during Asia, before falling back to 112.40 alongside the broader improvement in risk assets, but has swung back sharply to near the highs of the day following Bailey’s comments, and is now around 113.26, up 0.1% on the day. Among G10, declines over the past 24 hours were led by Scandinavian currencies and the pound. The GBP was 0.6% lower. The AUD also underperformed. The currency hit a new 2-year low of 0.6248 in Asian trading, recovered to an intraday high of 0.6346, before falling back sharply to be around 0.6276. The NZD held up better, gaining 0.4% against the USD, and seeing the AUD 0.8% lower against the kiwi at 1.1224. The yen is little changed against the dollar, down 0.1% at 145.85. Japan’s PM Kishida said in an FT interview that he fully supports the BoJ’s ultra-easy policy stance and that policy needs to remain easy until wages rise.

In equity markets, US equities turned lower following Bailey’s comments. The S&P500 had been up around 0.8%, but reversed a rally to be around 0.6% lower. The Nasdaq is 1.1% lower, returning the index to a bear market, more than 20% below its recent peak. US inflation data on Thursday the next big data print for US markets. Shares in Asia were lower, the Nikkei lost 2.6% and the Hang Seng 2.2%. the Euro Stoxx 50 was 0.5% lower.

In other economic news, and with most of the headlines already revealed in the press, the IMF cut its global growth projections. Growth next year was trimmed from 2.9% to 2.7%, after 3.2% growth this year, while inflation was revised up to 8.8% this year and 6.5% next year. The IMF said risks to the outlook remained “unusually large and to the downside”, with a 25% chance of year-ahead global growth falling to 2.0%, the 10th percentile of global growth outturns since 1970.

In Australian data flow yesterday, the NAB Business Survey strengthened further in September . Conditions rose 3pts to 25, higher than the pre-COVID peak and only exceeded only by the post-lockdown surge in early 2021. Trading conditions drove the increase, rising by 9pts to +38, while Profitability (+16) and employment (+16) were little changed. Confidence fell 5pts to around its long run average. Westpac-Melbourne Institute Consumer Confidence fell 0.9% m/m in October to 83.7, remaining near historic lows. Those surveyed after the RBA downshift to the pace of hikes supported the read, with much stronger sentiment than those surveyed prior to the meeting.

NAB Markets Research Disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.