Robust growth for online retail sales observed in June

Insight

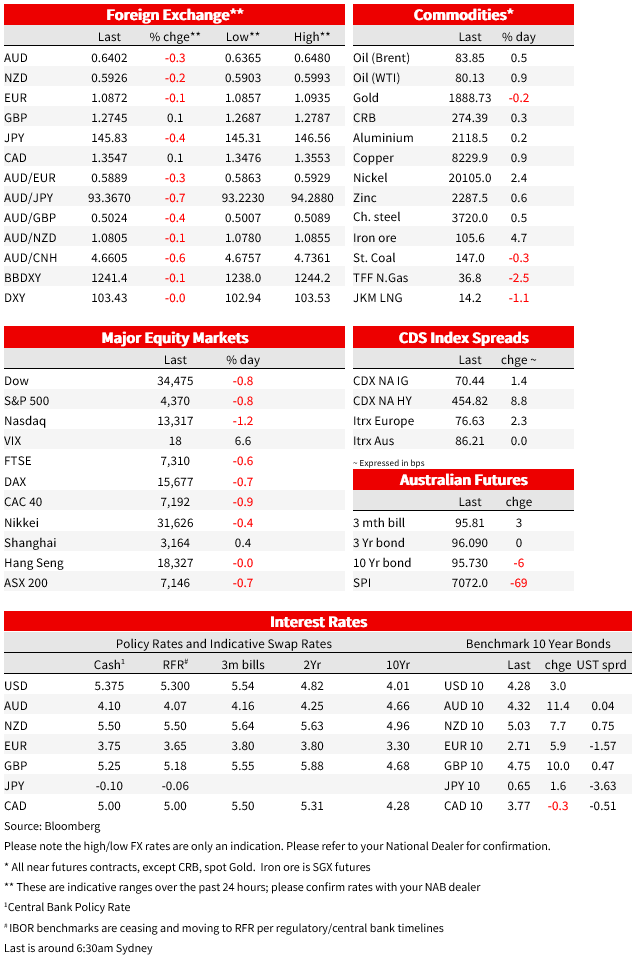

It’s been onwards and upwards for global bond yields overnight, and AUD has spent time below 64 cents

Higher yield, steeper curves and ongoing APAC regional currency weakness continue to be the hallmarks of current global financial markets, alongside which investor enthusiasm for Northern Hemisphere stocks continues to wilt, joining many of their Southern Hemisphere counterparts. The S&P500 has suffered its third successive daily fall to currently be more than 5% off from its late July highs, so too the UK FTSE 100, while the Eurostoxx 50 is more than 6% off its 31 July high. Only second tier (and mixed) US data overnight; the main data point Friday is Japan CPI.

Doom loop (or “urban doom loop”) is a term coined by a Columbia University professor for the downward spiral some cites seem to be on (San Francisco, one of the epicentres of the United States’ opioid crisis and a city which has saw some of highest housing cost in the world at the height of this millennium’s tech. boom) has been mentioned in this regard in some recent dispatches.

Here, we plagiarise the term in relation to currency markets, with the Japanese yen at the epicentre. The ongoing appreciation of USD/JPY – to a new post November 10 ’22 high of ¥146.56 overnight – is in turn seeing the Chinese authorities displaying an evident aversion to the CNY/JPY exchange rate trading persistently above 20.0 (given its ever-increasing competition with Japan in high end manufacturing goods – electric vehicles the best current example). USD/CNY on Thursday hits its highest level since 3 November, which in turn is plaguing currency markets throughout the APAC region, no more so than in Australia and New Zealand. The NZD/USD fell to its lowest level since 3 November (0.5903) and AUD/USD to its lowest since 4 November (0.6363). In light of what are quite fast moving market developments, NAB’s FX Strategy team have put its FX forecasts under review and will provide an update to clients early next week.

Since our local market close, we have seen some respite for the ongoing rise in USD/CNY after a report that Chinese authorities told state-owned banks to step up intervention in the currency market this week, in a push to prevent a surge in yuan volatility – “according to people familiar with the matter” (Bloomberg). Senior officials are also considering the use of tools such as cutting banks’ foreign-exchange reserve requirements to prevent a rapid depreciation in the Chinese currency, said the people. All well and good, but we’d note that despite the fall back, CNY/JPY is till trading above ¥20, so unless the Japanese authorities are about to step in and do something to arrest the rise in USD/JPY, China will almost inevitably countenance further (orderly) USD/CNY appreciation.

As for the prospects of BoJ intervention, we do note that the overnight high of ¥146.56 was last seen on 10 November 2022 – the day the BoJ intervened (selling over $40 billion) and which on the day produced a more than 5-big figure fall in USD/JPY (and subsequently to below ¥130). Caveat emptor, though we’d note the backdrop to that (successful) intervention was falling 10-year Treasury yields, from above 4.0% to below 3.50% in less than four weeks. No such JPY tailwind this time round.

The latest rise in 10-year US Treasury yields, to a high of 4.325%, took them to within a basis point of their 2022 high (currently +3bps at 4.28%) while the 4.42% high on the 30-year bond is the highest it’s been since 2011. It comes into the NY close +4bps on the day at 4.39%. the latter has, as my BNZ colleague Jason Wong notes, pushed the US 30-year mortgage rate up to a 21-year high of 7.09%. UK 10-year gilts yields yesterday hit their highest levesl since 2008, and in NZ the 10-year rate exceeded 5% for the first time since 2011.

Overnight US data releases were second tier and not market moving. Initial jobless claims came in line with the consensus at 239k, consistent with a flat trend albeit down on the prior week’s 250k but which was seen to be inflated by the collapse of the Yellow trucking corporation (employing some 30,000 staff). The Philadelphia Fed index unexpectedly rose to a 16-month high of +12, going against the lower Empire manufacturing index earlier in the week. It wasn’t all positive though, with employment and capex indicators both weaker.

Yesterday’s local Labour Force Survey disappointed, employment in July falling 15k (and the unemployment rate rose 2 tenths to 3.7%). NAB’s economists note that month to month swings in employment growth continue to be volatile, but that the update is clearly on the soft side, consistent with some underlying cooling in the labour market and that combined with the WPI earlier this week further suggests the RBA will be on hold in September.

US equity markets have closed with the S&P500 down 0.8% and the (more interest rate sensitive) NASDAQ -1.2%. bringing its fall off its mid-July highs to around 8%. Consumer Discretionary stocks are the worst performing S&P500 sub-sector (-1.58%) Energy is the only sector in the green, aided by a near 1% gains for WTI crude (+$0.72 to $80.10). Most base metals are firmer, while iron ore futures are up almost 3%, in which respect we note some positive rhetoric on Chinese radio yesterday coming out of the current CCP-leader gathering in Beidaihe, though at this stage rhetoric is the operative word.

As for the G10 FX scoreboard, the fall back in USD/CNY from its highs has spilled over to USD/JPY (tail now wagging dog?) to see the JPY as the best performing currency (+0.4%) with AUD (-0.3%) and NZD (-0.2%) the worst. GBP/USD is marginally firmer on the day, EUR/USD a fraction weaker. The overall DXY USD index is flat on the day and the broader BBDXY down 0.1%.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.