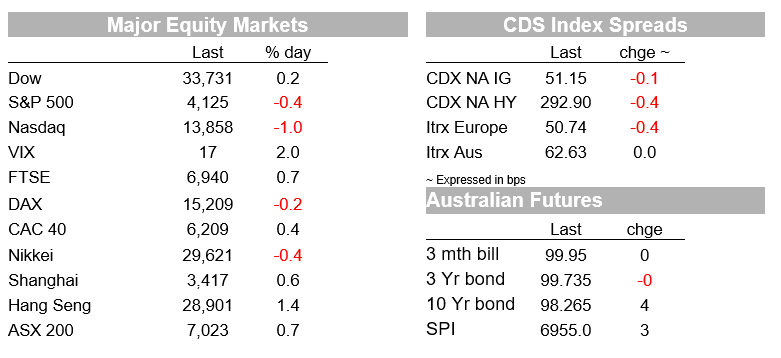

Coinbase hits $100bn before tumbling and dragging IT shares lower

US Bank earnings report impress, but outlook remains uncertain

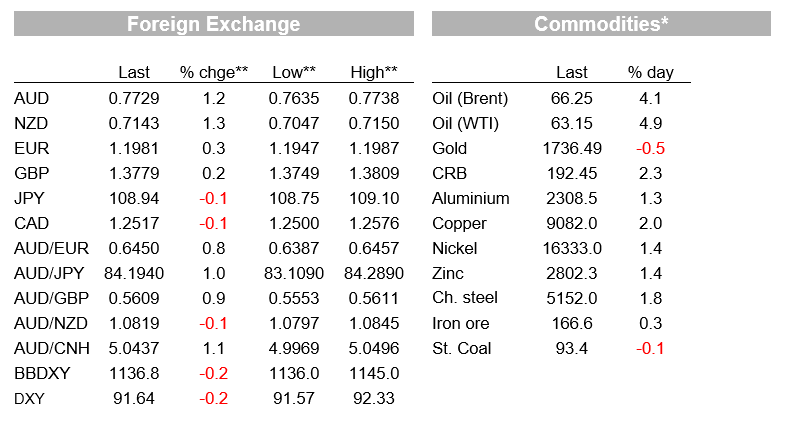

Oil gains over 4% on inventory decline and IEA improved outlook

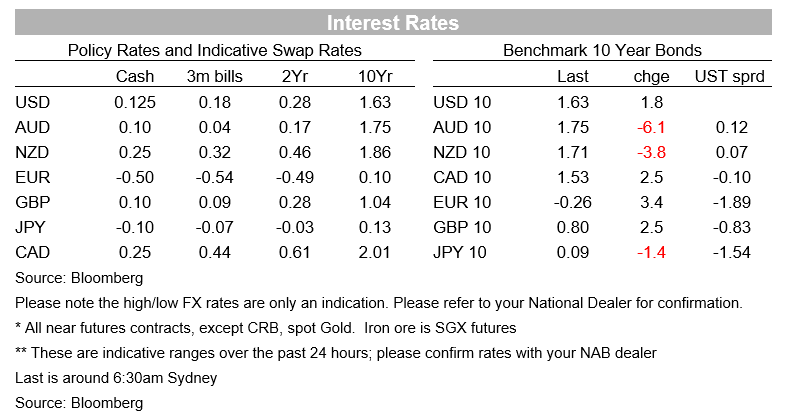

UST yields consolidate yesterday’s modest rise

Powell confirms tapering likely well before rate hikes

USD decline extends lifting AUD and NZD above 77c and 71c respectively

Denmark becomes the first country to completely stop using the AstraZeneca vaccine

Coming up: AU Labour force, US retails Sales, Philly Fed, Joblees claims and more Fed speakers

You’ve got to trust your instinct And let go of regret You’ve got to bet on yourself now star… All mixed up you don’t know what to do – 311

European equities closed mostly higher, led by cyclical shares and after a positive start, US equities are mostly lower with the IT sector the big underperformer. Coinbase hits $100bn in its trading debut, before tumbling below its opening level. Oil gains over 4% on inventory decline and IEA improved outlook while UST yields consolidate yesterday’s modest rise. USD underperformance extends with AUD and NZD the top G10 performers in the past 24 hours.

A sharp selloff in Coinbase, following its IPO today has been noted as the main factor for the u turn in the NASDAQ and the S&P IT sector performance overnight. Coinbase which runs the largest bitcoin exchange in the US listed on the NASDAQ and soared on the open (did anyone expect anything else?) putting its valuation up around $100b, before reversing course. The listing coincided with a record price for Bitcoin, which rose to just under $65k, but the opening euphoria proved to be short-lived with the stock falling close to 20% from its opening level and now trades at $328, around 14% lower on the day. That would be a bit painful if you bought the stock at its intraday peak of $429.54, but for initial investors it was a massive bonanza.

US banks earnings reports were the other big focus in the equity market with Goldman Sachs, JPM and Wells Fargo kick starting the reporting season in earnest. JP Morgan posted a record quarter, supported by a boom in investment banking, strong trading profits and $5.2b of credit reserve releases. However, its share price fell as it warned that loan demand was challenging , with higher interest rates weighing on mortgage finance applications (now down 1.87%). Goldman Sachs reported strong trading profits on similar themes and its share price was up 2.3%. Wells Fargo also reported strong profitability and the bank provided an upbeat outlook for net-interest income and further loan-loss reserve releases, with the share price up around 5.5% on that.

European equities closed mostly higher and the Stoxx 600 Index gained 0.2% with cyclical sectors the outperformers. As I type, the S&P 500 is down 0.41% and the NASDAQ is -0.99% while the Dow is +0.16%. IT and Consumer discretionary shares have led the declines in the S&P 500 (down over 1%) while Financials +0.66% and Energy (+2.91%) sectors were the outperformers. The latter no doubt aided by the over 4% rise in oil prices following news of a decline in US crude stockpiles. US crude oil inventories fell 5.89 m/b, according to the International Energy Agency (EIA) data, and bigger than estimates of a 2.58m draw. The EIA also upgraded its global consumption outlook for this year.

Moves in UST yields were pretty subdued overnight, essentially consolidating the small rise that we saw during our APAC session yesterday. The 10y US Note now trades at 1.6323%, up 1.7bps from yesterday’s closing levels while the 30y bond now trades at 2.3120%, (+1.8bps ).

Fed Chair Powell participated in a virtual discussion with the Economic Club of Washington overnight and reiterated the Fed’s key messages noting that a tightening of policy will wait until substantial progress has been made toward the Fed’s dual mandate. Powell stressed the point that the Fed is more outcome based and that at this stage a rate liftoff is highly unlikely before the end of 2022, notwithstanding market’s pricing suggesting there is a good chance it could happen. Notably, Powell suggested the Fed would follow strategy to 2013 and 2014 meaning QE tapering would come “well before” any interest rate increase.

Moving onto currencies, the USD extended its decline into a third day with the AUD and NZD leading the G10 gains against the greenback over the past 24 hours. Both antipodean pairs were looking a bit undervalued and yesterday both pairs finally broke above their recent narrow ranges that had confined them since early in the month. The AUD now trades at 0.7723 (+1.09%), a level last seen on March 23 while NZD now trades at 0.7142 (1.18%). The upsize range break have probably contributed to both AUD and NZD’s outperformance over the past 24 hours, however the resilience of risk appetite and recent gains in commodities have also helped.

Looking at other majors both the EUR and GBP are up over 0.20% and USD/JPY is down 0.10 consolidating just below the ¥109 mark. The ¥108.50/60 area is the next key support level to watch.

We finish the daily with some covid news that could be relevant for Australia, given our large commitment the Astrazeneca vaccine. Denmark became the first country to completely stop using the AstraZeneca vaccine, with the country’s health authority noting the “real risk of severe side-effects” associated with its use . Soren Brostrom, the head of the Danish Health Authority, said that his “best estimate” based on local research suggests a 1-in-40,000 risk of getting a blood clot after an Astra shot. Although he also noted that the higher incidence of clotting among younger women appears to be linked to the fact that a lot of health-care workers were inoculated early on, many of whom are female.

Denmark’s ability so far to keep the virus in check also fed into the health authority’s decision and gives it some leeway to delay its vaccination program. The EU unveiled plans to massively increase its supply of the Pfizer vaccine, signalling a move away from the AstraZeneca jab as well.

Coming up

Australia’s March Labour Force report is the data highlight during our time zone and then it is all about US data releases and Fed speakers.

NAB has pencilled in an above consensus +55k jobs and for the unemployment rate to fall two tenths to 5.6% (consensus 35k/5.7%).

As for Job Keeper, worth noting that that the scheme ended March 28 with around 1.1m people supported, so today’s report will not capture the impact from the scheme’s termination. Official estimates suggest that 100k to 150k workers may have been displaced. Our economists believe the broader strength of the labour market alongside an elevated level of Jobs Vacancies are positive signs suggesting the end of the scheme is unlikely to derail the recovery.

US data releases include Jobless claims (700k exp vs 740k prev.), March retail sales (Total 5.8% exp vs -3% prev, ex auto and gas 6.4% exp vs -3.3% prev.), Philly Fed ( 40.9 vs 51.8 prev.) and Industrial Production ( Mar 2.5% exp. vs -2.2% prev.)

Fed’s Bostic, Daly, Clarida and Mester are on the speaking roster tonight

Q1 US Earnings Reporting highlights include Bank of America, Pepsi, Citigroup, Charles, BlackRock and Delta Air Lines

Market prices

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.