NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The rally in equities has stalled for now – except for the NASDAQ.

“Last night I had the strangest dream; I sailed away to China; In a little row boat to find ya; And you said you had to get your laundry cleaned” Matthew Wilder, 1983

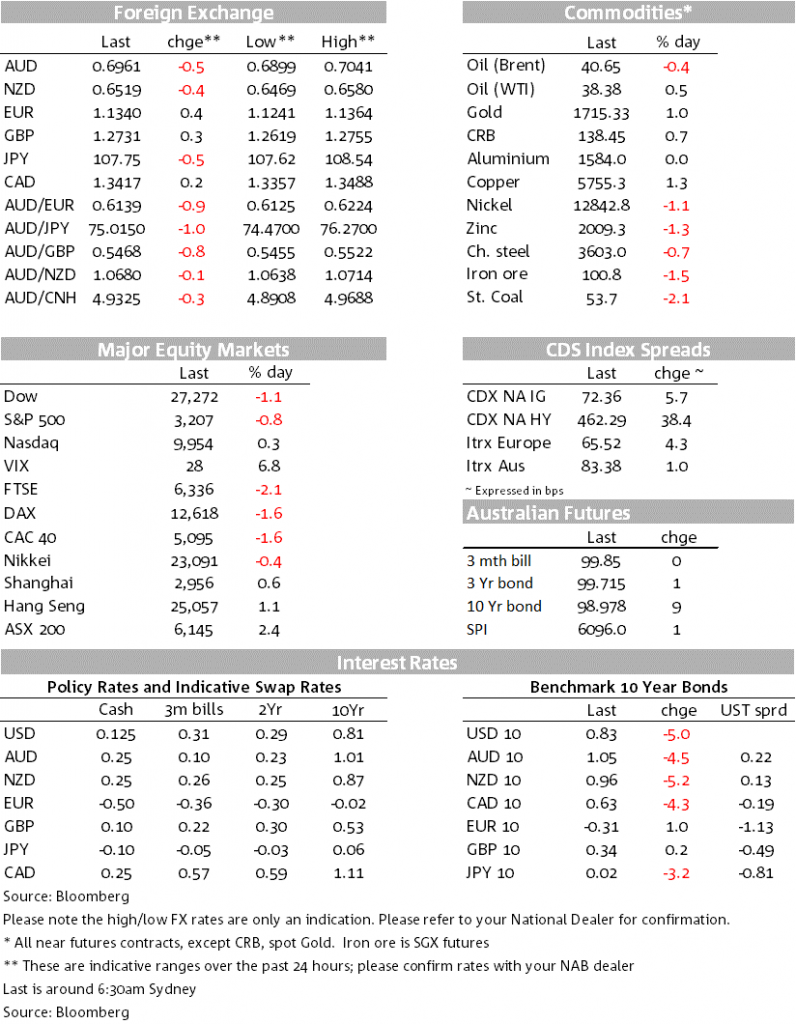

The risk rally took a breather overnight with little in the way of new data or newsflow. US stocks were mixed with the S&P500 down -0.8%, but the tech-heavy NASDAQ closed up +0.3% driven by outperformance by Apple and Amazon (both +3.1%). The USD remains on the backfoot (DXY -0.3% to 96.39) with EUR (+0.4% to 1.1340) and USD/Yen (-0.5% to 107.75) driving. The AUD and NZD both pulled back from recent highs amid the slight risk-off tone. Highlighting that slight risk-off tone is the VIX which has risen for two days to 27.

After hitting a high of 0.7041 hit a low of 0.6899 before recovering to be -0.5% at 0.6961. The move lower coincided with headlines that China was issuing an alert to Chinese students studying or proposing to study in Australia due to rising discrimination (see Global Times). The move lower though also coincided with broad USD strength at the time with similar moves being seen in the NZD as well (high of 0.6580 to a low of 0.6469). While the alert has little immediate impact due to border restrictions, the move does hamper an earlier easing of restrictions that could have allowed the resumption of international education via a 14-day quarantine period. The alert follows a general travel alert that was issued last Friday and is widely seen as part of the recent deterioration in the Australia-China relationship.

The bilateral relationship has come under strain following Australia’s vocal push for a COVID-19 inquiry and Australia’s co-authored letter urging China to reconsider its proposed Hong Kong Security Law (that letter signed alongside Canada, US and the UK). Restrictions over recent weeks have been placed on other sector including on selected beef abattoirs and tariffs on barely. To date restrictions have been only on a small minority of goods worth just 0.2% of GDP, but the travel alert could affect a further 0.8% of GDP. An escalation to other sectors would have a more significant impact. Some hint of that perhaps was given yesterday with reports of Sinopec reducing long term contract purchases from APLNG, though should be seen in the context of spot markets offering cheaper prices.

Unemployment is expected to peak at a lower rate with the Australian Treasury revising its forecast peak to 8% from 10%. Treasury Secretary Dr Kennedy noted yesterday “I think the unemployment rate won’t go as high as previously thought,” Dr Kennedy said. “I think the unemployment rate by September will likely to be in the order of 8 per cent“. Yesterday also saw no new locally transmitted coronavirus cases, suggesting restrictions are likely to be eased further and faster than that outlined by the National Cabinet. It is conceivable that should there by no new locally transmitted cases for 14 days, social distancing restrictions could be lifted inline with NZ. Yesterday’s NAB survey had little impact on markets, showing some recovery but conditions remained deeply in negative territory at -24.

Key to its fortunes will be the EUR which rose 0.4% alongside comments by Germany’s Finance Minister which boosted hopes around the €750bn EU recovery plan. Minister Scholz said that there was a “constructive spirit” and that he had the impression that everyone “has the will to reach an agreement within a short time”. The broader USD index, the BBDXY had fallen for 8 straight days. Gold also continues to rally +1.1% and rejecting a move below $1,700 for a second day.

The US NFIB Small Business Optimism survey rose to 94.4 from 90.0 and clawing back around a quarter of its combined March-April fall. Interestingly the survey showed an incremental improvement in the “plan to hire” to a reading of +8%%. Research by the St Louis Fed using home base data finds the improvement in the job market continued into June with high-frequency data showing employment is now down just -8.75% from January, compared to -11.15% in May and -15.08% in April (see link for details). US Jolts for April were also out last night but are very dated and pre-date the latest improvement in the labour market.

It is quiet domestically with most focus on the US CPI and FOMC later tonight. As for the domestic data calendar, the two measures of consumer confidence are out along with housing finance approvals. Focus then shifts to Asia with the Chinese CPI/PPI – the PPI being an important signal around whether the aftermath of COVID-19 continues to be disinflationary. Europe has little on the radar with the US CPI and FOMC likely to dominate. Although no change is expected at the FOMC meeting, focus will be on the forecast dots, any discussion of yield curve control and on Chair Powell’s thoughts about the sharp upward surprise in last Fridays payrolls.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.