We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

As expected, the ECB will moderate its Pandemic Emergency Purchase Program (PEPP) bond buying pace in Q4 with its December meeting now a key event. China makes historic sale of oil reserves weighing on oil prices.

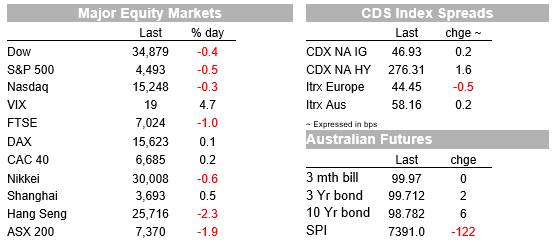

US equity markets have closed in the red again with the S&P 500 extending its decline to a fourth day in a row. The UST curve bull flattened with a solid 30y auction contributing to move lower in longer dated yields. The USD weakness evident in our afternoon session yesterday accelerates overnight with greenback failing to show any safe haven demand, Euro and AUD are little changed. As expected, the ECB will moderate its Pandemic Emergency Purchase Program (PEPP) bond buying pace in Q4 with its December meeting now a key event. China makes historic sale of oil reserves weighing on oil prices.

US equity markets remain on struggle street with the S&P 500 recording its fourth consecutive day of decline, down 0.46%, the NASDAQ closed -0.25% and the Dow was -0.43%. Buying the dip is not yet coming to the rescue with investors seemingly conflicted by mixed data signals while uncertainties over the economic impact from the delta variant outbreak are restraining investors appetite for risk, notwithstanding ultra easy accommodative policy by the Fed and other central banks. EU equities closed mixed with the Euro Stoxx 600 index modestly lower at -0.06%

Overnight the big event was the ECB meeting and as expected the Bank confirmed it intentions to moderate the PEPP bond buying pace in Q4. Lagarde justified the decision by saying the euro region’s “increasingly advanced” rebound could be maintained with less monetary help. Higher vaccination rates and better market conditions (read: lower bond yields and a lower EUR exchange rate than earlier in the year) were noted as key supporting factors for the decision. The ECB president also stressed that the decision was not tapering, but rather a recalibration consistent with the PEPP’s envelop . Lagarde didn’t put an exact figure on the new monthly bond buying pace but Reuters reported it will be a still hefty €60b-€70b per month pace, giving the ECB some flexibility to adjust to changing market conditions.

New staff forecasts showed a stronger near-term outlook for prices and growth, however Inflation is seen averaging only 1.5% in 2023, below the Bank’s 2% target. The PEPP programme is due to end in March next year and President Lagarde flagged the December meeting as the one at which the Governing Council will decide how to transition from this programme to the ECB’s other bond buying programme (the Asset Purchase Programme). Analysts expect the Asset Purchase Programme, which is currently running at €20b per month, will be expanded when the Pandemic bond buying programme comes to an end, to smooth the adjustment for the market.

On first impression the ECB’s upbeat assessment of the EU economy and calibration of the PEPP should have elicited a risk positive outcome, providing an uplift to the Euro and core EU yields. But with inflation projection below the 2% target , Lagarde also noted that unlike the Fed and BoE among other Central Banks, the ECB does not have a plan to end its bond buying programme. The Delta outbreak was also noted at a cause for concern.

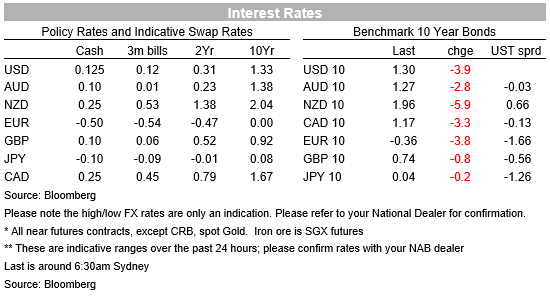

In the end reaction to ECB decision resulted in a move lower in core EU yields with 10y Bund closing the day 4bs to -0.36%. That said other core yields also moved lower with the UST curve bull flattening overt the course of the night. A solid 30y bond auction was a factor at play and arguably the move lower in oil prices likely played a hand too (more below). The 30y bond auction printed at 1.91%, almost 2 basis points lower than the bonds’ yield in pre-auction trading, remarkably too Bloomberg noted dealers were awarded their lowest-ever share – just 13.1% – as investor demand surged with indirect bidders (which includes foreign central banks) showing big appetite for the bond.

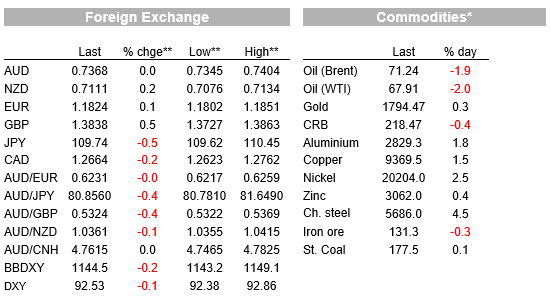

Meanwhile the move lower in oil prices ( down 1.9%/1.8%) has been attributed to the news that China made an unprecedented intervention in the market, releasing crude from its strategic reserve for the first time with the explicit intention of lowering prices. China’s National Food and Strategic Reserves Administration said in a statement the country had tapped its giant oil reserves to “to ease the pressure of rising raw material prices.”. Oil prices briefly rose earlier in the session after a US government report showed crude stockpiles fell as production tumbled the most on record last week due to disruptions by Hurricane Ida.

Moving on to currencies the USD is modestly weaker, down 0.15/0.2% in index terms, showing little safe haven demand in spite evidence of risk aversion in equity markets . JPY and CHF, the G10 safe havens are up between 0.45% and 0.55% with GBP sandwiched in between. Meanwhile the Eure and AUD are little changed, up a few pips at 0.7368 and 1.1826 respectively. NZD has done a little bit better, up 0.17% and now trades at 0.7105.

Finally, in terms of data releases, US jobless claims fell more than expected to 310K from 345K, well below the consensus, 335K. The positive reading was countered by potential disruptions caused by Hurricane Ida. So hard to read too much into it.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.