Online retail sales growth slowed in May following a fairly strong April

Insight

In a quitter session, relative to recent times, the risk positive vibes have extended into a third consecutive day with higher global equity markets, lower global rates and a weaker USD.

Events Round-Up

In a quitter session, relative to recent times, the risk positive vibes have extended into a third consecutive day with higher global equity markets, lower global rates and a weaker USD. After a dovish interpretation to the Fed Minutes, overnight accounts of the ECB’s October meeting revealed a preference for a smaller hike in December (50bps instead of 75bps) while the German IFO survey was also positive (small) surprise. China’s daily Covid infections climbed to a record high, but market remain calm while Chinese media suggest a PBoC RRR could come as soon as today.

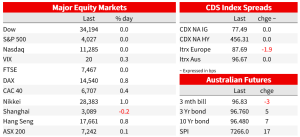

The US Thanksgiving holiday has contributed to a quitter overnight session as the US cash market is shut with lower trading volumes seen across the board. European equities extended their recent gains with the Stoxx 600 adding another 0.46% while regional indices also ended in the green. Meanwhile US equity futures are also higher with the S&P 500 mini +0.26%. Gains in Europe were boosted by a better-than-expected German IFO survey and the prospects of slower (Fed and ECB) rate hikes.

Germany’s Ifo business-climate index rose more than economists had expected in November, with companies turning less pessimistic about the economic outlook. This is a narrative of a less pessimistic assessment, a recession in Germany is still expected, but not an economic collapse .Commerzbank’s chief economist suggested the reasons for the improvement (business climate, Nov: 86.3 vs. 85.0 exp.) are that the risk of gas rationing has fallen significantly in recent weeks, the German government has massively increased its relief package, and supply shortages have eased. Of note while the current conditions gauge continued to slide downwards, the expectations component jumped consistent with winter recession and a spring recovery.

After yesterday’s dovish Fed Minutes interpretation, the overnight positive equity vibes were also aided by the ECB minutes revealing a preference for a 50bps hike in December rather than a repeat of the October 75bps step up. The accounts of the ECB October meeting suggested that one reason for the 75bps increase was that it was fully priced, and a smaller hike would imply an unwelcome loosening of financial conditions. Using that logic, market pricing for a December hike has been ranging around 50bps (52bps today), so given the ECB is apparently not keen on disappointing/shocking the market, a 50bps hike in December looks preferable. Favouring this view, the Minutes also revealed concerns over the deteriorating economic outlook ahead with contained wages growth also favouring a smaller hike. Overall, the minutes seem to be consistent with the recent leaks from policymakers. Countering this trend, however, overnight the well-respected ECB Board member Isabel Schnabel signalled it may be premature to scale back increases in interest rates with inflation continuing to pose dangers to the euro-zone economy. Speaking in London, Shnabel said “Incoming data so far suggest that the room for slowing down the pace of interest rate adjustments remains limited,”.

Moves in European core yields have been quite mixed with 2y UK Gilts and French FRTR moving up by 10 and 8bps while 2y Bunds fell by 4bps. Further out the curve, 10y Bunds extended their decline by 9bps to 1.84%, 10y French yields fell by 9.4 bps to 2.28% while 10y UK gilts gained 2.3% to 3.02%. The inversion of the 2s10s Bund curve has been getting some market attention, now down to -24bps, the most inverted since 1993. Meanwhile in the US, US 10-year Treasury futures are pointing towards small downside pressure on rates, adding to the 14bps fall already seen this week.

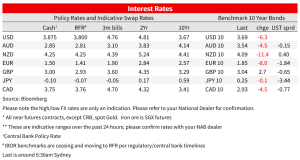

The move lower in core global bond yields alongside the ongoing improvement in (equity) risk appetite have contributed a lengthening in the USD decline to a third consecutive day. Both DXY and BBDXY USD indices are down around 0.25% with JPY is leading the gains within G10 pairs. After trading to just above ¥142 on Monday, USD/JPY now trades at ¥138.45 (JPY +0.9% over the past 24 hours), the move lower in 10y UST yields contributing to JPY gains, but also keeping the pair quite volatile.

Yesterday, during our time zone, the euro traded to a high of 1.0444, but overnight it lost some altitude and now it exchanges hands at 1.0414, meanwhile while GBP continued its outperforming run, reaching a three-month high of 1.2150 overnight, before losing steam, the pair now trades at 1.212.

The NZD also pushed up to a three-month high, reaching just under 0.6290 at the London close (now at 0.62, My BNZ colleague Jason Wong notes that chartists will be seeing whether it can break the 200-day moving average of 0.6302. During the NZD downturn that really kicked off from June 2021, the NZD has made several upside breaks of the 200-day moving average but has subsequently retreated. Our projections show a stronger NZD through next year, although following a 14% gain off the mid-October low, a period of consolidation is probably now overdue. The technical RSI has breached 70, typically seen as a short-term “overbought” signal

The AUD traded to an overnight high of 0.6778 and now starts the new day at 0.6767. Consistent with our recent narrative the AUD is finding the air thinning as it approached the 0.68 level. The pair is more sensitive to China’s economic outlook with news of daily Covid infections climbing to a new record likely contributing to some cautiousness. The recent spike in infections is a real test for Chinese leaders, who have recently signalled a higher degree of tolerance in order to minimise the economic impact from lockdowns, but the speed in the rise of infections may force them to change their mind. Bloomberg notes that many Chinese cities are once again expanding their testing efforts and building makeshift hospitals to quarantine the growing number of people who are infected. Though no city-wide lockdowns have been announced, the widespread restrictions are increasingly paralysing economic activities.

Meanwhile Chinese newspapers are suggesting the PBoC may cut banks’ reserve requirement ratio as early as today as fresh Covid outbreaks fuel concerns about the sluggish economic recovery.

In other news, Sweden’s Riksbank hiked by 75bps to 2.5%, as expected, a dialled-down pace from the 100bps hike in September, and with a projected terminal rate around 3%. The Riksbank projected inflation to remain high, averaging 5.7% next year, a 20% slump in house prices and a 1.2% contraction in GDP.

Germany has set out its plan to claw back 90% of the earnings from some clean power generators as the government seeks funding for its consumer aid package. The government is planning to skim earnings above €130 a megawatt-hour for solar, wind and nuclear, according to a draft law seen by Bloomberg News. The level proposed is lower than the European Commission’s suggested level of €180 a megawatt hour.

Meanwhile deliberations on the EU proposed oil cap for Russian oil continue with Poland rejecting the EU’s executive arm’s proposed price of $65 per barrel as being too soft on Moscow while Greece, a massive player in the oil shipping industry, doesn’t want to go below $70. Critics of the levels proposed so far point to the fact that Russia is already selling its oil at a discount, so a price cap at that level would allow for business as usual. Oil fell 0.1% /0.3% (WTI/Brent) as traders expect Russian oil to keep flowing as a result of the talks. Shutting Russian oil out of the global market would send prices surging.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.