Economic and financial market update

Insight

The ECB meeting was the big event for markets last night and as expected the Bank delivered a 75bps hike, but it sounded less committal on future rate hikes.

Events Round-Up

EC: ECB deposit facility rate (%), Oct: 1.5 vs. 1.5 exp.

US: GDP (q/q% ann’lsd), Q3: 2.6 vs. 2.4 exp.

US: Core PCE deflator (q/q% ann’lsd), Q3: 4.5 vs. 4.5 exp.

US: Durable goods orders (m/m%), Sep: 0.4 vs. 0.6 exp.

US: Durables ex transport. (m/m%), Sep: -0.5 vs. 0.2 exp.

US: Initial jobless claims (k), 22-Oct: 217 vs. 220 exp.

The ECB meeting was the big event for markets last night and as expected the Bank delivered a 75bps hike, but it sounded less committal on future rate hikes. After last week’s WSJ speculation of a potential Fed pivot followed by a smaller than expected BoC hike this week, rates markets are cheering the idea of a potential down shift or gear change by major central in terms their pace of hiking ahead. EU rates have led a global bond yield decline while the euro has led G10 declines vs the USD. NZD has been the outperformer while AUD has lagged with the decline in iron ore likely playing its part.

As expected, the ECB raised its key interest rates by 75bps (deposit rate to 1.5%, and refinancing operations and marginal lending facility to 2% and 2.25%, respectively), but after a third rate increase in a row, and its second 75bps hike in two meetings, the market was left with the impression the Governing Council is now more inclined to slowdown the pace of rate hikes ahead with the statement noting “substantial progress” in the withdrawal of monetary policy accommodation. In a widely expected move, the ECB also adjusted the terms on its targeted longer-term refinancing operations (LTRO) given the evolving economic circumstances and especially the surge of inflation. Going forward, the ECB will adjust the interest rates applicable on those operations from what had previously been very favourable terms. The change in the LTRO terms is likely to likely to encourage earlier repayment of these loans and faster ECB balance sheet normalisation. Banks that had originally borrowed from the ECB at -0.75% during the pandemic (with the possibility of achieving a -1% borrowing rate) will now be charged the average ECB deposit rate over the period.

As for quantitative tightening (QT) plans, the ECB said that it would determine the principles for running down its large bond holdings at the December meeting. Media reports suggested avoiding an immediate decision on QT just as officials plan their final interest-rate hike of the year would also be consistent with their preference to relegate to the background the unwinding of the portfolio. This was a surprise, given prior to the ECB meeting expectations were for the Bank to foreshadow a decision on QT at the December meeting.

Reinforcing the notion of a gear change or less hawkish ECB, a sourced Bloomberg story noted that while the decision to hike by 75bps was reached with broad consensus, three policy makers wanted a smaller half-point step. Speaking at the press conference ECB president Lagarde insisted that the ECB had “more ground to cover.” Adding that officials could still hike for “several meetings” and lift rates to a restrictive level if needed.

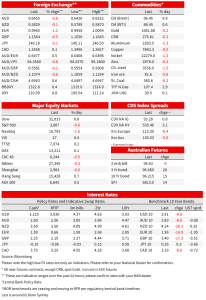

A less hawkish interpretation to the ECB triggered a decline in core global bond yields with European yields the leading the moves. Italian 10y BTPS fell 32bps to 3.98% while 10y Bunds fell 15bps to 1.95%. UK gilts also joined the party down 18bps to 3.387% while in the US the UST yields fell around between 8 and 13bps, 10y tenor down 10bps to 3.90%.

Notably too, ECB December pricing is around 5bps below what it was before the ECB meeting (1.96%). Further out in 2023 however the market has pared back the terminal rate to circa 2.55%-2.60% from 2.80% yesterday (though global bond mkt rally accounts for some of this).

Moving onto FX, the euro has led losses against the USD, down 1.11% to 0.9962, after trading above parity prior to the ECB announcement. The NZD has outperformed, up around 0.5% over the past 24 hours to a five-week high above 0.5829 while the AUD is down 0.58% to 0.6450 . Yesterday the AUD traded to a high of 0.6522, but then in the afternoon it drifted lower, trading to an overnight low of 0.6428, before recovering ahead of the NY close. A sharp decline in iron prices yesterday didn’t help the AUD, Iron ore extended its recent decline to its lowest level in more than two years amid mounting concerns over global steel demand. The bulk commodity hit $82.45 a ton in Singapore, its lowest since May 2020. Prices have fallen more than 50% from a peak in March.

The USD Q3 GDP beat expectations, but details underwhelm with the data release not eliciting a material market reaction. Q3 GDP rose at a 2.6% annualized rate, a bit above the consensus, 2.4%. Most of the growth in GDP was due to a huge swing in net foreign trade, contributing 2.8%, while domestic final demand rose only 0.5%. That compares with an average of almost 2.6% over the five years before the pandemic.

Other details also underwhelmed, Investment in residential housing plunged at an annual rate of about 26. Consumer spending, the engine of the economy, rose 1.4% from the previous three months, capping the weakest three quarters since the demand destruction of early 2020. The underlying growth trend in the US is softening and markets remain wary of a likely recession next year.

The S&P 500 closed 0.61% lower, after swinging between gains and losses for most of the session and the Nasdaq 100 fell more than 1% weighed down by weak earnings report from Meta (formerly Facebook), which saw its share price crumble more than 20% overnight. After the bell, Amazon sales and profit outlook trailed estimates with Bloomberg noting Amazon’s online retail business in North America and international both lost money. Amazon shares were down 19.7% in post-market trading.

NAB Markets Research Disclaimer

Economic and financial market update

Insight

Online retail sales growth slowed in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.