Online retail sales growth slowed in May following a fairly strong April

Insight

The ECB has surprised markets with an accelerated QE unwinding plan

https://soundcloud.com/user-291029717/ecb-taper-talk-while-lavrov-tells-tales?utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Overview

Market volatility remains elevated with sentiment not helped by failed Russia Ukraine talks while the ECB surprised markets with an accelerated QE unwinding plan. Meanwhile US CPI printed in line with expectations, but at a 40y high with higher numbers expected ahead. EU bonds have led a rise in core global bond yields with 10y UST yields now trading at 2%. Equities are a sea of red while commodity linked currencies are outperforming with EU fx on struggle street, euro ECB gains swiftly unwound.

Disappointingly, although widely expected, Russia-Ukraine talks failed to yield a positive outcome with Russia confirming attacks will continue until its goals are met. “We want a Ukraine that’s friendly and demilitarized, a Ukraine in which there isn’t a risk of the creation of another Nazi state, a Ukraine where there won’t be a ban on the Russian language, on Russian culture,” Russia’s Foreign Minister Lavrov said. A ceasefire remains well out of sight with Ukraine’s Foreign Minister Kuleba describing the meeting as “difficult” and accusing his counterpart of bringing “traditional narratives” to the table.

Amid an upwardly revised inflation outlook and against expectation for a cautious approach, the ECB announced a faster QE exits and opened the door to rate hikes in September, but more likely in Q4 . In line with its sole inflation/price stability mandate, the ECB expressed a greater level of concerned about record inflation than weaker economic growth with Russia’s invasion of Ukraine a “watershed” moment for Europe, threatening a bigger rise in prices ahead.

At the press conference President Lagarde confirmed the ending of the PEPP in March as expected with an APP downshifts to €40bn in Apr (presume Mar too), €30bn in May and €20bn in June. Thereafter, the calibration of the APP in Q3 will be data dependent and reflect an ‘evolving assessment’ of the outlook. Lagarde noted that “The ECB stands ready to revises its net asset purchase schedule if the medium-term inflation outlook changes and if financing conditions become inconsistent with further progress to the 2% target”.

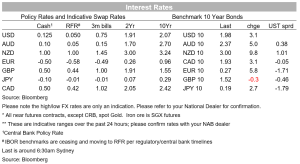

We interpret the ECB message as saying the ECB does not see the Medium-Term inflation outlook weakening and unless that changes, QE under APP will end at the end of Q2. The ECB also noted that any rate rise will take place ‘sometime after’ the end of APP and ‘will be gradual’, thus rate hikes now look possible in September, but more likely in Q4 i.e. October or December . “Clearly ‘sometime after’ is all-encompassing,” Lagarde said. “It can be the week after, but it can be months later”, message here is that the decision will be data dependent. A 20bps rate hike is now priced for the September meeting, versus 8bps priced yesterday with a cumulative lift in the effective cash rate of 40bps by the end of the year, vs 34bps a day before.

As for the ECB staff forecasts, inflation got an upward revision and GDP growth was slightly downgraded. HICP (CPI readings) are up at 5.1% in 2022 (3.2%), 2.1% in 2023 (1.8%) and 1.9% in 2023 (1.8%) while GDP forecast are now at 3.7% 2022 (4.2%), 2023 2.8% (2.9%) and for 2024 1.6% (unchanged).

US CPI headline and core printed in line with expectations at 0.8%mom (7.9%yoy from 7.5% prev.) and 0.5% mom (6.4%yoy vs 6.0% prev.) respectively. The headline print was a 40-year high reflecting higher gasoline, food and shelter costs and now with energy prices on the rise following Russia’s invasion of Ukraine and sanctions expectations are for inflation to rise even more . Net take-away is that US inflationary pressures are proving to be more persistent and expansive, increasing the pressure on the Fed to lift the funds rate and cool the economy. A 25bps rate hike remains well priced, but after the CPI print today, there has been a gradual uptick in Fed rate hike expectations with the December Funds rates now priced at 1.64%, 4bps higher relative to yesterday’s levels.

Moving on to markets, post the ECB, EU bonds have led a rise in core global bond yields with 10y Bunds closing the day 6bps higher at 0.266% while 10y Italian BTPS jumped 22bps to 1.897%, the market clearly reflecting its disappointment/surprise to the ECB’s plans for a faster unwind to the APP. 10y UST yields now trade at 1.9986% (lets call it 2%!), up 4bps on the day with similar rises recorded along the curve. Early this morning, the 30y UST bond auction was awarded at 2.375% vs 2.399% when-issued yield, helping ease the early ECB driven rise in longer dated yields. The 2y10y UST curve has steepened a little bit more, now at 28bs, up around 10bsp in the past couple of days.

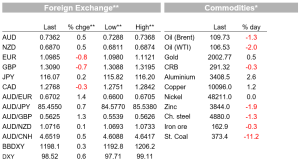

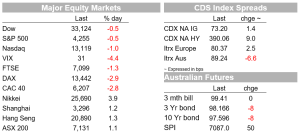

Equity markets are a sea of red with all EU regional indices closing down between 1% and 3% with the Euro Stoxx 600 index down 1.69%, Ukraine news and ECB hawkishness not helping. As I type the S&P 500 is down 0.91% with the energy sector the notable outperformer, up 2.78%, oil prices are little changed today Brent trading at $109.34 while WTI is $106.23, both around 1.5% lower relative to levels 24 hrs ago. Meanwhile Financials and IT are at the bottom of the pile, down 1.1% and 1.8% respectively. The NASDAQ now trades down 0.99% and the Dow is -0.60%.

EU currencies have been whipsawed overnight with ECB announcement briefly lifting the euro to an intraday high of 1.1121, but the realisation of a hawkish ECB before a slowing growth outlook and higher inflation, combined with a ragging war in the Ukraine quickly triggered a more sombre assessment of the euro’s fortunes. The pair now trades at 1.0986, down 0,8% over the past 24 hours with other EU pairs down by similar amounts. Safe-havens CHF and JPY are 0.4% and 0.2% lower with commodity linked currencies outperforming. The AUD has led the charge, up 0.53% to 0.7362 and as it has been the case in recent times, the prospect of commodities remaining well supported amid an energy supply crunch exacerbated by Russia’s sanctions and China’s commitment to stimulate its economy, are effectively trumping the pair’s risk sensitivity attributes. The Kiwi is not far behind, up, 045% to 0.6871.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.