Online retail sales growth slowed in May following a fairly strong April

Insight

The S&P500 high to low fall since the early January high puts it down 19% year to date and although not officially in bear market territory yet, looks to be only a matter of time.

https://soundcloud.com/user-291029717/equities-bomb-as-investors-are-reminded-of-inflation?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Tuesday’s US equity market rally is now distant memory, the S&P500 and NASDAQ finishing Wednesday’s NY session off 4% and 5.1% respectively. More poor US retailer results (Target) and warnings about margin squeezes gets some of the blame, for the early-day losses at least, before momentum appears to have taken over in the afternoon. No last ‘hour of power’ reversal today, quite the opposite. (Much) weaker stocks sees bond yields lower again, led by the longer end (10s -10bps) while the USD has regained its safe haven mojo, up 0.5% in DXY terms and meaning the AUD’s early-week flirtation with levels back above 0.70 has proved all too short-lived (currently 1.1% down on the last 24 hours). Today’s local labour market data is expected to show unemployment below 4% for the first time in more than 50 years.

Following Walmart yesterday, Target has been the latest big US retailer – covering both consumer staples and discretionaries – to trim its profits forecasts (profit margins down to 6% from 8% previously) and which has seen its share price fall 25% – the most in a single day since the 1987 ‘Black Monday’ crash, if anyone remembers. This got the ball rolling (downhill) in the US equity market and it was pretty much one-way traffic down for the whole of the day, with both the S&P and the NASDAQ closing near the lows.

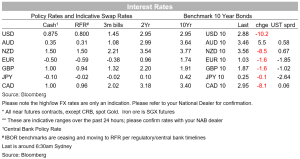

A fall back in US bond yields in conjunction with the latest deterioration in risk sentiment has proven to be of no comfort for the more interest rate sensitive NASDAQ, ending the day -5.1% against -4.0% for the S&P. The S&P500 high to low fall since the early January high puts it down 19% year to date (and still above last Thursday’s low). So officially not yet in bear market territory, but which looks to only a matter of time. The NASDAQ is 30% off its (November 2021) high, so firmly ensconced in bear market terrain.

Bond markets see 10-year Treasuries finishing in NY -10bps at 2.88%, so more than 30bps off the cycle highs seen at the start of last week. 2s are off just 3bps in contrast, so there is still no serious entertainment of a ‘Fed put’ being anyway close to the radar amid still very high and rising inflation.

Latest inflation reads overnight have come from the UK, where headline CPI hit 9.0%, 0.1% less than expected and up from 7.0% on March, the lifting of the price caps on household energy bills by Ofgem, the regulator, that took effect at the start of April, responsible for most of the increase. Core CPI rose to 6.2% from 5.7%, in line with expectations. In Canada, inflation on all measures surprised to the upside, on top of upward revision to the march measures. The average of the 3 core measures is 4.2% up from a revied 3.9% while headline rose to 6.8% from 6.7%, a tenth more than expected.

Other data to note overnight was for US Housing Starts and Building Permits. Starts were only down 0.2% against -2.1% expected but only because March was revised sharply lower – the level of starts at 1,724k was below expectations. Permits meanwhile fell by 3.2%. More signs that the earlier sharp drop-off in mortgage applications and New Home Sales is starting to filter into reduced starts (and applications for future starts).

In geopolitical news, Sweden and Finland have formally submitted their NATO applications, but which for the time being will be subject to a veto from Turkey amid its ongoing accusations that Sweden is supplying arms to Kurdish military group YPG in the name of supporting the fight against Islamic State but which Turkey claims are being used to kill Turkish soldiers and civilians alike.

In currency markets , the jump in UK inflation, albeit not unexpectedly so, saw GBP reverse much of the gain seen in the wake of Tuesday’s much-stronger than expected labour market today. To the extent that the latest rise is not seen leading to any epiphany from the Bank of England regarding what it is minded to do on policy rates in coming months helps rationalise the FX market response. This is despite what former BoE governor Mervyn King had to say overnight about the incompatibility of BoE policy settings with wages growth running at 5-7%. We might have reminded Lord King that while wage growth (pretty much everywhere) significantly lags actual inflation, it is not adding to inflationary pressure – that only happens if the sort of rises being achieved now are repeated down the track. It’s far from obvious they will be.

AUD took a hit yesterday after the local Wage Price Index printed 0.7%, as forecast by NAB but a tenth less than consensus. The still-soft annual growth vindicates the RBA’s recent shift toward more contemporaneous, albeit anecdotal evidence, of faster wages growth (both from their liaison programme and the likes of the NAB business survey). The data nevertheless helped consolidate thinking that the RBA will more likely than not persist with no more than 25bps incremental policy changes at upcoming meetings.

AUD has been hurt further by the risk-off mood overnight, down to a low near 0.6950 and at -1.1% on the night is the second worse performing major currency after GBP (-1.2%). Lower commodity prices amid rising concerns about ‘demand destruction’ can’t be helping either. Oil prices are off +/-3% and most industrial metals off by at least 1%.

The USD is bid across the board in line with risk sentiment, DXY 0.5% stronger at 103.9 but still some way off last Friday’s 105 cycle high.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.