The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

There have been massive falls in US equities, particularly tech stocks.

https://soundcloud.com/user-291029717/sobering-up-equities-hit-aussie-dollar-slides-ahead-of-a-slow-recovery

I watch you disappear into the dark, Capture in your eyes, Hands

Pull me back to earth, Pull me back to earth – Friendly Fire

It is easy to see how many would argue that the US Tech led slump in equities overnight was/is the correction we needed to have. Many US tech companies are awesome performers, but their lofty valuations have been a major concern for some time.

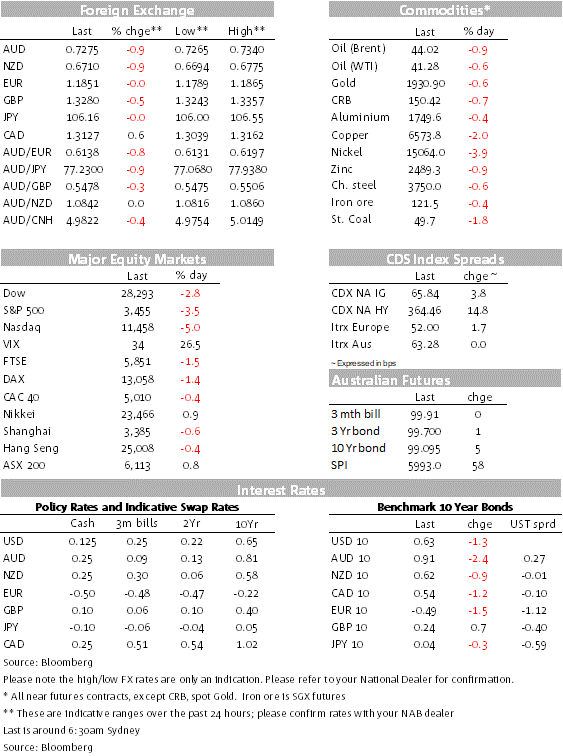

The big U turn in equities has added further fuel to the longer dated UST rally, now on its fifth day, taking the 10y UST Note to 0.63% around the middle of its recent 0.50% to 0.78% range. At the expense of risk sensitive currencies, the USD and safe haven currencies have found some loving with both the AUD and NZD, down ~0.9%.

Arguments for an equity correction have been growing for some time, but the huge amount of monetary stimulus and plus a new legion of retail investors have kept the fires burning. What started as a cool and swift drop of ~0.5% on the S&P 500 and ~1.3% on the NASDAQ at the open, gathered momentum shortly after with big IT shares leading the decline.

US data releases haven’t been great, but not soft enough either to justify the move, so the overbought signal (technicals and valuations) can now be used as a” justification of a I told you so”. That may well be the case, but if you have been investing in the NASDAQ since early April (not from the low in late March), after today 5% drop you would still be up just over 60%.

Now the question is whether the correction has legs or whether investors are temped back in. For now, both S&P 500 and NASDAQ still remain very close to their record highs, so the big drops overnight are not that material. For the record the tech led decline has seen Apple lose 8%, Microsoft down 6%, Amazon down 4.3% and Facebook -3.62%. The fall in US equities also spilled over into other markets. The Euro Stoxx 600 index was enjoying a good day, but ended down 1.4%.

The big U turn in equities added more ammunition to the UST curve flattening theme that has now been in place for a fifth day in a row. Last week’s curve steepening, led by the back end of the curve was all about the anticipation and eventual confirmation by Fed Chair Powell of a new FOMC averaging inflation target approach. That move up in longer dated UST yields has more than reversed, 10y UST yield now trade at 0.629% and the 30y bond is at 1.35%, down 2 and 3bps on the day and down 12.4 bps and 16.1 bps respectively over the past five days.

But then again not that bad either. Initial jobless claims came at 881k in the week ended Aug. 29, versus 1.01min the prior week, but numbers are not directly comparable given a change to seasonal adjustment methodology. On an unadjusted seasonal basis claims rose by 7.6k to 833k last week, led by a 39k increase in California.

Applications under the separate federal Pandemic Unemployment Assistance program – which targets the self-employed/gig workers and others who don’t usually qualify for state programs – jumped by about 152k to 759k. The key takeout is that the figures are still very large, above the worst levels seen during the GFC so any possible improvement in the labour market should be seen in that context.

The US ISM services index fell slightly, in line with expectations, still indicative of economic recovery but a bumpy one. The breakdown was mixed, showing an 11pt fall to 56.8 in new orders, but a nearly 6pt rise in the employment index to a 6-month high, albeit still sub-par at 47.9. In other economic news, the US trade deficit widened to its largest level since 2008.

The Fed’s Evans gave a sobering outlook for the US economic recovery, saying that its path will “critically depend on receiving substantial additional support from fiscal policy” and even then, alongside progress in controlling the virus, “it will be some time before the economy recovers from the hit it took”. Evans was evidently a fan of outcome-based policy guidance and he indicated that such “forward guidance for the rate path and asset purchases could be beneficial in the not-too-distant future”.

Unsurprisingly the equity slump has resulted in a bid for save haven currencies with CHF, JPY and the USD the key beneficiaries at the expense of the likes of AUD and NZD.

In index terms, the USD is up 0.17% on the BBDXY and little changed in DXY terms.

Looking at G10, commodity linked currencies are the big underperformers with NZD and AUD at the bottom of the pile, both down 0.9%. Early in the week we noted that the move up in the AUD above 74c was looking a bit stretched and was not fully justified by our short term fair value model, AUD now trades at 0.7273, a few bps above its overnight low of 0.7268.

Meanwhile the NZD is at 0.6712, a few more bps higher relative to its overnight low of 0.6694. Both antipodean currencies remains vulnerable to an extension of the tech led equity correction overnight.

After falling as low as 1.1790, it is back up to 1.1852. The FT reported that “several members” of the ECB governing council told it that the euro’s rise against the dollar and many other currencies risks holding back the eurozone’s economic recovery. One member added that the US Fed’s strategic shift to target average 2% inflation added to the pressure on the ECB to respond with its own strategy review. This is a nicely poise backdrop for the ECB Lagarde to set the record straight at the Bank’s policy meeting next week.

On the US fiscal front, Bloomberg reports that Treasury secretary Mnuchin and House speaker Pelosi have agreed to a “clean” stopgap funding bill free of stimulus that would help avoid a government shutdown. But this does nothing to support the recovery and we note Senate Majority Leader McConnell’s mid-week comments expressing doubts about whether Congress can get a deal on another pandemic relief package

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.