The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

Market sentiment was tempered somewhat by rising rhetoric between the US and China.

https://soundcloud.com/user-291029717/equities-hit-by-chinas-clashes-with-trump-and-hong-kong?in=user-291029717/sets/the-morning-call

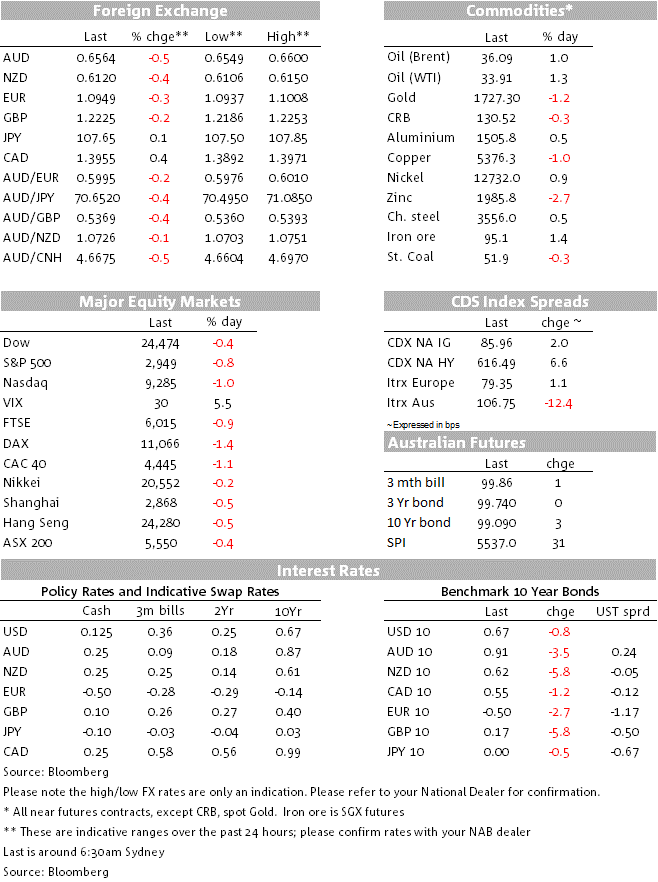

Heading into the weekend and the start of the (delayed) China National People’s Congress, the temperature of US China tensions are rising and taking a bite out of risk sentiment everywhere, albeit only modestly so at this stage. This includes USD/CNH which has risen from 7.1050 to 7.1350 during the course of the night and the HKD lifting off the 7.7500 level to 7.7550, with 12-month forward points doubling alongside, from 250 to 500. The S&P has closed down 0.8%, alongside which AUD/USD is back down to 0.6565 from a high of 0.6616 on Wednesday.

The US Senate yesterday passed – unanimously – a bipartisan bill aimed at forcing non-US firms to certify they are not under control of a foreign (read: Chinese) government or the Public Company Accounting Oversight Board is not able to complete three consecutive years of audits. If firms don’t comply, the bill would require delisting from US exchanges. The bill needs sign-off from Congress and Trump but, if implemented, could lead to the de-listings of Chinese technology heavyweights such as Baidu, Alibaba and JD.com.

Trump lashed out at China in a tweet, accusing the country of a “massive disinformation campaign” and blaming the “incompetence of China” for the worldwide spread of the virus. China responded that it will safeguard its sovereignty, security and interests while media reported that China was prepared to respond with retaliatory measures if the US presses ahead with sanctions.

China outlined plans for new national security laws in Hong Kong, with could reignite protests in the city and further inflame tensions with the US. Trump told reporters “if it happens, we’ll address that issue very strongly.” Remember the US was, pre-COVID-19, threatening to repeal the 1992 Hong Kong Relations Act allowing the United States to treat Hong Kong separately from Mainland China on the basis that it is not under the control of the Chinese government.

The 0.8% drop in the S&P still leaves it 3% up week to date, ditto the NASDAQ despite the 1% overnight fall. European stocks continue to underperform the US, e.g. the Eurostoxx 50 finished its day 1.4% lower.

The mild risk-of market tone hasn’t made much on an impression on the bond market, 10-year US treasury yields coming into the New York close unchanged at 0.68%. Of some note and against the backdrop of negative Bank of England policy rate chatter, 5-year gilt yields went negative for the first time (-0.015%).

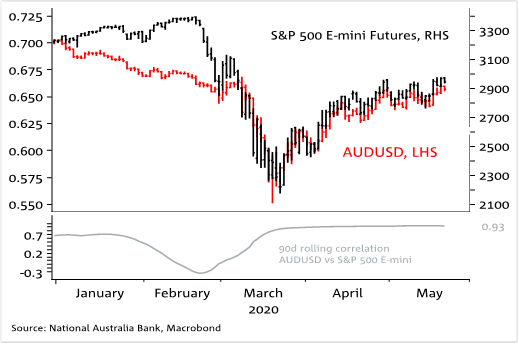

The AUD has predictably given back a little more of its mid-week gains to above 0.66 (0.6616 high) to be back just inside the prior 0.6370-0.6570 range. So yet again the Aussie is tracking almost tick for tick with the S&P futures (see Chart of the Day below). We’ve haven’t seen anything new with regards to China-Australia trade issues, though this time yesterday we noted an earlier editorial in the (Chinese state-sponsored) Global Times which gave reason to believe that at this stage China is not intending to extend trade restrictions beyond barley and beef, despite the public threat to include wine, dairy, fruit and oatmeal in the list of goods that could face import blocks. This is, according to the report, assuming there is no specific trade retaliation against Chines to the beef ban and (80%) tariffs imposed on barley.

The 0.5% 24-hour fall-back in the AUD has only been exceeded – curiously – by a 0.6% drop in the normally safe-haven CHF, while the JPY has behaved more predictably, little changed and so the best performing G10 currency. The NZD is also lower, by some 0.4% to 0.6117. Thursday’s moves leave the USD back a bit more comfortably inside its recent ranges, after threatening a break lower earlier in the week (e.g. the DXY is now 99.40 versus a 99.0 – 101.0 effective range since early April).

The keenly awaited ‘flash’ PMI data showed some improvement but all remained deep in contractionary territory – activity just falling less fast than in April and which was pretty much the best that could be hoped for (in contrast to China where PMIs are back above the 50 expansion/contraction mark). Germany’s manufacturing PMI lifted to 36.8 from 34.5, less than the 39.4 expected but services rose to 31.4 from 17.4, above the 33.1 expected. At the pan-Eurozone level, the composite PMI came in at 30.5 up from 13.6, above the 27.0 consensus. For the US (Markit) versions, manufacturing was 39,8 from 36.1 (40.0 expected) and services 36.9 from 26.7 (32.5). US weekly jobless claims fell back , but to a still huge 2.438 million from a downward revised 2.687 million the week before and meaning that since the crisis began, over 40 million Americans have filed for unemployment benefit. The Philadelphia Fed Business outlook ‘improved’ to -43.1 from -56.6. Markets were little moved by any of the data.

US Treasury Secretary Mnuchin said “I think there is a strong likelihood we will need another bill”, in reference to another stimulus package though did note the ‘need to fix the quirk that in certain cases we’re actually paying people more than they made (something that has also been apparent in Australia). Meanwhile, Federal Reserve vice-chair Clarida said the more monetary and fiscal support could be needed, adding that the Fed might return to its balance sheet options in the coming meetings. Clarida said the Fed was being briefed on Yield Curve Control (something that figures in Wednesday’s FOMC Minutes as a possibly new policy option).

China’s NPC will capturing most of the headlines today and through the weekend, other than which there isn’t whole lot on the calendar

New Zealand’s has Q1 retail trade, Japan has nationwide April CPI, and offshore this evening there’s UK April retail sales and the ECB’s account of its latest Governing Council meeting.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.