Coming in for landing in a heavy cross wind

Insight

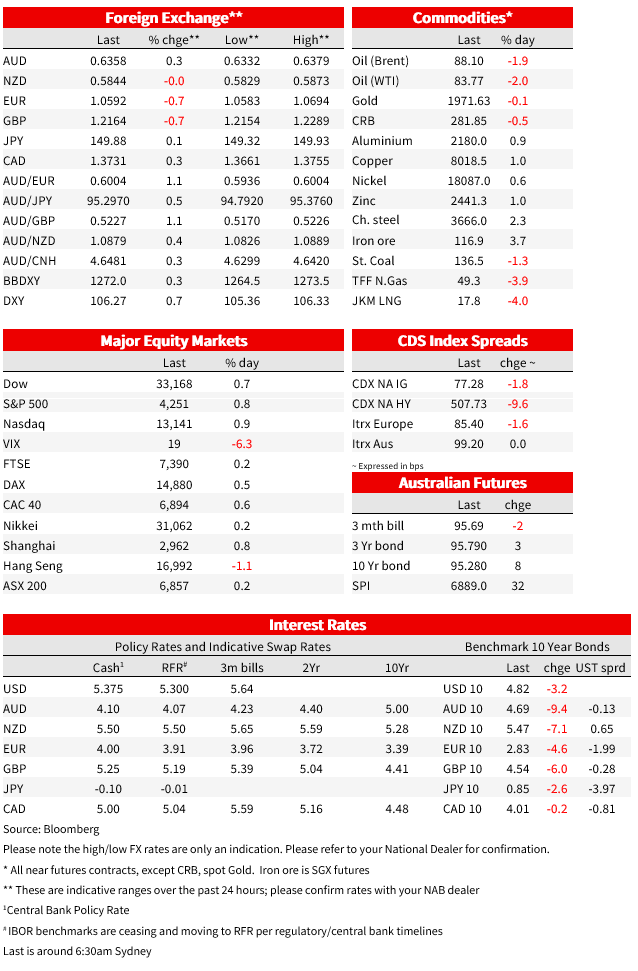

Weaker European PMIs, and potentially some unwind of yesterday’s move, have seen a stronger US dollar the main mover overnight, up 0.7% on the DXY.

GE: GfK consumer confidence, Nov: -28.1 vs. -27.0 exp.

GE: Manufacturing PMI, Oct: 40.7 vs. 40.1 exp.

GE: Services PMI, Oct: 48.0 vs. 50.0 exp.

EC: Manufacturing PMI, Oct: 43.0 vs. 43.7 exp.

EC: Services PMI, Oct: 47.8 vs. 48.6 exp.

UK: Manufacturing PMI, Oct: 45.2 vs. 44.7 exp.

UK: Services PMI, Oct: 49.2 vs. 49.3 exp.

US: Manufacturing PMI, Oct: 50.0 vs. 49.4 exp.

US: Services PMI, Oct: 50.9 vs. 49.9 exp.

Weaker European PMIs, and potentially some unwind of yesterday’s move, have seen a stronger US dollar the main mover overnight, up 0.7% on the DXY. Elsewhere, oil was lower, and the S&P500 was up 0.7%, following 5 consecutive days of losses. Bullock last night said “the Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation,” consistent with other recent commentary but leaving no doubt about the importance of today’s Q3 CPI print for the near-term outlook for policy.

Preliminary PMIs tended to re-affirm relative European underperformance. The Eurozone composite PMI slipped back to 46.5 from 47.2. That level reflects the steepest contraction signal since November 2020, or excluding the pandemic, since March 2013. S&P Global noted faster falls in orders, depleting backlogs, and employment in contraction territory. Manufacturing remained mired at very weak levels at 43.0 (from 43.4 and 43.7 expected) while services disappointed, slipping back to 47.8 from 48.7 (48.6 expected). Hope for continued stabilisation in German services disappointed, with a fall to 48.0 in the German Services PMI after briefly eking above 50 last month weighing on the Eurozone aggregate. The silver lining of the soft activity indicators is ongoing moderation in inflation pressures. Output prices slowed a little further in October, and are a little below their average in the 3 years prior to the pandemic.

The UK services PMI was relatively steady at 49.2, consistent with the economy remaining sluggish. UK labour market data showed the employment rate fell 0.3% in the three months to August. The unemployment rate was 4.2, up from 4.0% the previous quarter but revised down from 4.3% under the previous methodology. Low survey response rates made the normal method unreliable, with the ONS warning the new estimates should be treated as ‘experimental.’

Contrast the US, where PMIs where slightly stronger than expected, the composite at 51.0 from 50.2. Services rose to 50.9 from 50.1, closing some of the gap to the stronger, and closer watched, Services ISM (at 53.6) and consistent with ongoing expansion. The selling price index fell to a three-year low and is now close to the pre-pandemic long-run average.

The data only highlighted the gap relative weakness out of Europe, leaving the dollar stronger with gains led against European currencies. The DXY was 0.7% higher to 106.27, unwinding yesterdays decline. The euro lost 0.7% and is back a little below 106 after trading near 107 ahead of the PMI data, reaching an intraday high of 106.94. The pound lost 0.7% at 1.2164. Outside of Europe, currency moves were smaller, the CAD down 0.3% despite the fall in oil, and the yen and NZD both off just 0.1%. Ahead of CPI today, the AUD was the only G10 currency to gain against the US dollar, up 0.3% to 0.6357 after an intraday higher of 0.6379. German 10yr yields were 5bp lower, while 10yr gilts lost 6bp.

Speaking last night, RBA Governor Bullock gave a speech outlining the framework the RBA uses, emphasising the complementarity between the full employment and inflation objectives. There was little new in the substantive speech, though consistent with recent commentary and the October Minutes, Bullock opted to re-affirm that the Board is prepared to tighten if the inflation outlook surprises. Specifically, Bullock said “the Board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation.” Bullock was understandably not drawn in the Q&A on a specific threshold for today’s CPI and made clear updated November forecasts take into account broader information as well. Today’s CPI print (see coming up) is the key data ahead of the Melbourne Cup Day meeting and November forecast update. Market pricing has moved higher over the past couple of weeks to better reflect the risk of further tightening. There is a 37% chance of a hike priced for November and about a full hike priced by March next year.

While currency markets in large part reversed yesterday’s move, the same was not true for rates. The US 10-year Treasury yield has sustained the big fall seen over the previous session and currently sits at 4.82%, down 3bps for the day. The curve has flattened, with the 2-year rate up 5bps to 5.10%, with a run up to 5.13% after the stronger US PMI data not being sustained.

Oil prices fell, with Brent oil down around 2% to $88.10. WTI fell below $84 a barrel, and is only around 1% above its level prior to October 7. Brent is a little over 4% higher than prior to attacks in Israel. Easing concerns that the conflict between Israel and Hamas will widen across the Middle East. Israel’s delay to any ground invasion in the Gaza strip and G5 diplomatic efforts to prevent an escalation are seemingly factors here, though that contrasts the sentiment in WSJ’s lead story this morning that Iranian-Backed Militias Mount New Wave of Attacks as U.S. Supports Israel.

US equities were higher with the S&P500 up 0.7% to marking its first gain after 5 days of falls. Bullish forecasts from Verizon, 3M and General Electric supported. 10 of 11 sectors in the S&P500 rose, with only Energy in the red. The Nasdaq was 1% higher. In late trading, Microsoft Corp. climbed, while Google’s parent Alphabet Inc. dropped after reporting results.

In China, there looks to be some follow through from earlier reports that the central government could increase the fiscal deficit and provide more support. China’s legislature approved a rare mid-year budgetary expansion that will take the fiscal deficit up to 3.8% of GDP, higher than the usual 3% limit. The plan will require an additional 1 trillion yuan (USD137b) of debt and is designed to support disaster relief and construction. In a broader sign of increased focus on shoring up the economy and financial markets, Bloomberg reported that earlier in the day President Xi made his first known visit to the PBoC and also visited the state sovereign fund (SAFE).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.