Total spending grew 0.9% in June.

Markets are apprehensive ahead of US Fed Chair Powell’s Jackson Hole speech on Friday

Having exhausted my back catalogue, a play by the venerable bard seems apt in describing events overnights. There was a big hit to risk appetite in what was a night devoid of any top tier data. Instead markets are apprehensive ahead of US Fed Chair Powell’s Jackson Hole speech on Friday. Hawkish signals from Fed officials recently, as well as hawkish words from the ECB about hiking even with growing recession risks in Germany has led to a re-assessment of the markets view on rates. Meanwhile Europe’s dire energy situation and headlines of UK inflation hitting 18.6% suggests the peak of inflation is not here yet, and the risk remains that inflation is sticky higher for longer without further aggressive central bank action. No surprise then to see the USD at near multi-decade highs (DXY +0.7%), against a falling EUR (-0.9%) and GBP (-0.5%). Also adding fuel to the higher for longer inflation view was the Saudi energy minister pushing back on the fall in the oil price seen recently, stating extreme volatility and lack of liquidity in the futures market are disconnecting prices from fundamentals and may force OPEC+ to act.

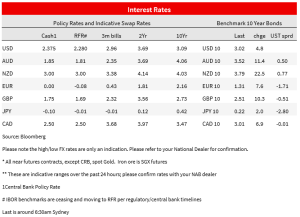

First to the move in rates. The US 10yr yield rose 5.5bps to 3.03%, its first close above 3.0% since 20 July, but still below the 3.5% peak in mid-June. The 2yr yield rose by more, up some 8.4bps to 3.32% with the 2/10s curve flattening to ‑29.9bps. The move in yields reflect markets pricing in a higher peak in the Fed Funds Rate, as well pricing less cuts in 2023. Markets now price a 66% chance of a 75bp hike in September, a peak of 3.78% in March 2023, and 35bps worth of cuts. This compared to last week which had a peak of 3.61% and 47bps worth of cuts. Hawkish signals from Fed officials last week, and weekend comments by the ECB’s Nagel about the ECB continuing hiking interest rates even as recession risks grow in Germany, has led markets to anticipate hawkish signals from US Fed Chair Powell on Friday at Jackson Hole. Former Treasury Secretary Larry Summers also added to the mix, stating that he hopes “…that we will get clarity that policy is not yet restrictive, that it needs to be restrictive if we’re going to contain inflation and that we’ll need to accept the consequences of that”.

Across the pond, the European inflation situation remains dire. UK inflation could hit 18.6% by early 2023 if there is no cost of living relief according to Citigroup given the expected rise in retail energy prices (note the UK energy regulator Ofgem makes another price announcement on Friday. Notably that 18.6% is well above the 13% peak forecast by the BoE only a few weeks ago, and argues the BoE will need to do more to avoid high headline inflation becoming imbedded into inflation expectations (Citi noted if inflation expectations lift, rates may need to rise as high as 6-7%). The question now is whether there will be any cost of living relief with the Tory leadership race set to wrap up and a new PM announced on 5 September. The rest of Europe is also straining under energy costs with gas price surging according with the Dutch TTF gas benchmark up some 13% to close at another fresh record high of EUR277/MWh – more than a 14 fold increase on the average of the past decade. Prompting that was Friday’s news of Russia shutting down the Nord Steam natural gas pipeline to Germany for three days of maintenance in late August, with fears around to what extent already reduced gas flows will come back on line.

Risk appetite has fallen on the combination of higher rates, elevated inflation, and growth risks. The S&P500 which had a mostly technical-driven rally since mid-July fell sharply, down -2.1% and with all sectors in the red. Tech stocks fell more sharply with the NASDAQ -2.6%. On growth risks, preliminary Korean export growth slowed sharply in the first 20 days of August with expects -4.3% m/m and the y/y rate falling sharply to 0.9% from 14.2%. Given Korea’s large tech exports and recent downward guidance from US semi-conductor firms, the wider tech sector may be facing headwinds amid high inflation, a pivot away from goods, and rising recession risk. Meanwhile in China, Chinese banks cut the 1yr lending rate by 5bps to 3.65%, but cut the 5yr rate by a larger 15bps to 4.3%. The bigger cut in the 5yr rate should help mortgage services costs, but given the main impediment to stimulus gaining traction is China’s zero-COVID policy, it is hard to see the stimulus having much of an impact. Chinese policy makers to date have also been reluctant to unleash large scale stimulus as they had done previously.

In FX it has been all about USD strength (DXY +0.7% and within a hairsbreadth of the mid-July high) in the face of European weakness with EUR (-0.9%, back to below parity at 0.9944 and at two-decade lows) and GBP (-0.5% to 1.1768 and around its lowest levels since the Brexit referendum vote). The Yen has struggled against the higher rates backdrop, with USD/Yen +0.4% to 137.47. The AUD and NZD have showed some surprising resilience, both only slightly lower from their close last week, although this must be seen in the context of large week’s chunky depreciation, which saw the NZD plunge over 4% and the AUD down 3½%. Further yuan weakness hasn’t spilled over in the NZD or AUD. Overnight, USD/CNY hit a two-year high of 6.85.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.