Total spending grew 0.9% in June.

Data, supply and hawkish CB talk push core yields higher

https://soundcloud.com/user-291029717/europes-caution-chinas-hope?in=user-291029717/sets/the-morning-call

US Treasury yield have a led a rise in core yields with a curve bear steepening instigated by a 8bps rise in the 30y Bond. US tech shares succumb to the weight of higher yields, the S&P 500 is flat and the USD is stronger largely reflecting euro underperformance, now trading with a 1.13 handle. Commodity/pro-growth currency pairs perform, notwithstanding a softer commodity backdrop. Biden-Xi virtual summit today at 11:45am Sydney time

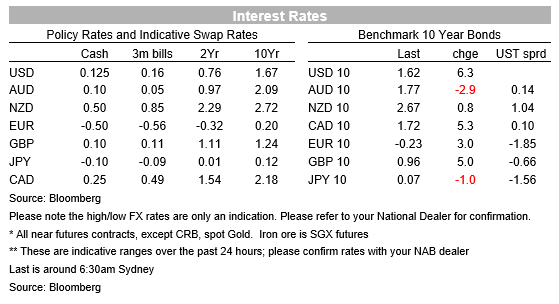

The steepening in the UST curve has been led by an 8bps rise in the 30y Bond to 2.01%. 10y UST yields are up 6bps to 1.62% with the breakeven component explains most of the uptick in the 10y yield, up 5bps to a 16-year high of 2.77%. Solid US data, supply dynamics and hawkish ex Fed talk have all played a part in the move up in yields with European core yields also higher.

The US Empire State Survey beat expectations, jumping 11 points to 30.9 with inflation related components higher as well . New orders climbed from 24.3 to 28.8, shipments dipped from 52.3 to 32.2, while prices paid (83 after 78.7) and prices received (50.8 vs 43.5) both rose. Adding a little more encouragement on the supply chain side, delivery times eased back from 38 to 32.2. Six months ahead conditions eased back to 36.9 from a v high 52.0.

There has been plenty of corporate issuance overnight adding momentum to the move up in yields with the market also cognisant of the $23bn 20-year UST auction later this week. Hawkish Central Bank talk has been an additional variable explaining the move up in yiedls with ECB dovishness a contrasting feature.

In separate interviews, Ex-New York Fed Dudley and former Richmond Fed Lacker weighed into the Fed hiking debate noting that the Fed will probably have to raise its target for the federal funds rate to at least 3% to try to keep inflation in check. Dudley added “I certainly expect the peak to be well above the 1.75% price point” implied in the Treasury securities market.

Staying with the hawkish theme, Bank of Canada Governor Macklem wrote an opinion piece in the FT saying “we are not there yet, but we are getting closer” when commenting on the prospect for higher rates. The Bank’s forward guidance requires slack in the economy to be fully absorbed and Macklem noted that the Bank has twice brought forward the likely timing of slack being absorbed.

Meanwhile in the UK, BoE Bailey told lawmakers he remained “very uneasy about the inflation situation”, although evidently not so uneasy that he shocked the market by not voting for a rate hike a couple of weeks ago that had been fully priced. He suggested that he was waiting for more information on the labour market post the end of the furlough scheme before making a decision on rates. UK labour market data is out later today, but Bailey and co. are probably going to need to see a few more labour market prints before making any conclusion on employment conditions post the furlough scheme.

In contrast to all this hawkish talk, speaking to the EU parliament ECB Lagarde reiterated the Bank view that inflationary pressures should ease over the medium term while risks of rising wages and second-round effects are ‘limited’ . The ECB president noted that “If we were to have any kind of tightening approach to the current situation, it would actually do more harm than good,” she said. “It would begin having an impact at a time when inflation is actually returning to lower levels.”

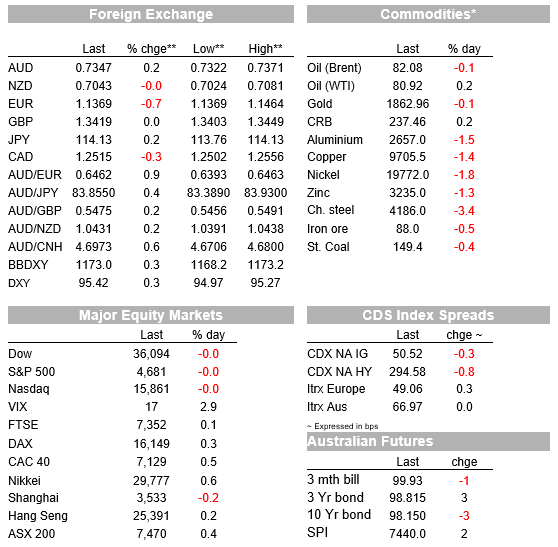

Moving onto currencies USD indices are up around 0.3% (DXY and BBDXY) largely reflecting euro weakness, down 0.55% to 1.1387 . The union currency’s underperformance has not been helped by the technical break below the 1.14 mark and although dovish ECB talk is not new news, it has certainly been a contrast to all the other overnight hawkish messages. Covid outbreaks and news of social restriction not helping the perception Europe is in struggle street while the US is rebounding nicely, albeit with price pressures.

The past 24 hours have been good to pro-growth/commodity linked currencies with the AUD and CAD up around 0.20% to 7350 and 1.2526 respectively. NZD is up a little bit less to 0.7043 (+0.10%), after trading to an overnight high of 0.7083. Yesterday’s China activity data for October was good news, showing activity is starting to recover, although a lower growth path ahead still looks like the more likely outcome given the need to deleverage the property sector while covid related disruptions are likely to remain a feature for a while longer still. In terms of the numbers, monthly seasonally adjusted numbers were only slightly higher than September. October retail sales were 0.4% m/m, up from 0.3% m/m in September. Y/Y consensus I think missed the base effect moving on from September. Industrial Production was the one to show the largest rise with monthly at 0.4% m/m, up from 0.1% in September. The beat in Industrial Production appears to have come from Mining and Utilities rather than Manufacturing – so consistent with the Manufacturing PMI in October being at 49.2.

The resilience of the AUD and other commodity linked currencies is notable given the softer backdrop in commodity prices . Copper (-1.02%), Aluminium (-1.59%), iron ore ( -0.43%) and energy prices are all lower, perhaps reflecting a more cautious take on China’s activity readings, a theme to watch as a more persistent decline in commodities more likely than not will eventually weigh on the AUD and other pro -growth pairs.

The S&P 500 is trading flat on the day with tech and materials struggling amid a higher UST yields and softer commodities. The NASDAQ is down 0.30% with Tesla share making a late rebound, after falling on news Elon Musk was considering selling more of his shares in an online sparring with Senator Bernie Sanders.

The Biden-Xi virtual summit is expected to start at 11:45am Sydney time and last for a couple of hours. No major breakthroughs are expected, although the fact that both presidents are willing to talk to each other is good news. An ease in trade tensions is a potential outcome while issues around human rights, Taiwan and Covid are likely to remain unresolved.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.