Online retail sales growth slowed in May following a fairly strong April

Insight

A torrid day for Hong Kong’s hang Seng index yesterday, driven by sharp fall in property sector stocks and led by a 16% fall in Evergrande ahead of Thursday’s bond coupon payment day, spilled over to the global arena on Monday with equities down sharply, bond yields lower and safe haven currencies in the ascendancy.

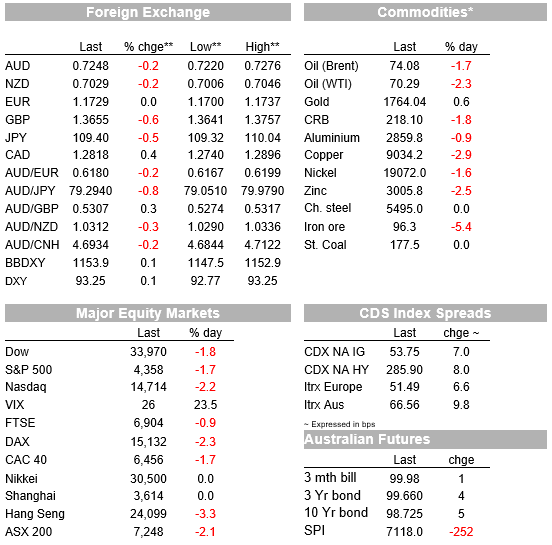

A torrid day for Hong Kong’s hang Seng index yesterday, driven by sharp fall in property sector stocks and led by a 16% fall in Evergrande ahead of Thursday’s bond coupon payment day, spilled over to the global arena on Monday with equities down sharply, bond yields lower and safe haven currencies in the ascendancy. The last ‘hour of power’ of NYSE trading has though seen losses for the S&P 500 pared to 1.7%, having been down 2.75% at 3pm NY time, pulling the VIX back to nearer 25 from 29 earlier (latter the highest since February) while AUD/USD, having been as low as 0.7220, is currently back near 0.7250.

Yesterday’s local market session was all about Evergrande and other Hong Kong listed property sector stocks, the expectation being that the former would come under some form of regional government control following an expected miss on bond coupon payment this Thursday. The question then being, how much pain would have to be endured by its creditors who include not just Chinese banks, but offshore bond holders, contractors, suppliers and retail investors, the latter including employee who own substantial amounts of Wealth Management Profits (WMP) issued by the stricken property behemoth. The latter is where the risk of social stability/unrest lies first and foremost. So the response of the Guangdong provincial government, assuming it takes effective control of Evergrande after Thursday, is going to be important.

Together with a further sharp in iron ore prices on the Singapore futures example yesterday (down from $102 to close to $91 at one stage (back to $96 now), spill over from weakness of HK property sector stocks was most evident in Australian mining sector shares, contributing most to the 2.1% loss for the ASX. Together with the dummy spit from France following last week’s AUKUS nuclear submarine deal, which includes a demand from France to cancel EU-Australia Free Trade Agreement talks, AUD/USD was the weakest major currency during our time zone Monday, amid generalised USD strength.

Of note though, the USD has not fared nearly as well as the JPY or CHF overnight, the latter both up 0.5% on the day while the DXY USD index has pared its gains back to just 0.05% at the NY close. This, alongside the late day reversal in US stocks, has helped AUD/USD pull up to around 0.7250 from a low of 0.7220, so only about 10 pips below where it ended in New York last Friday. Its way to soon to suggest that the AUD pull-up could mean that the worse is over, and epically with the FOMC just ahead, though we do note that FX futures market positioning data published last Friday from the IMM in Chicago shows record net speculative short positions in AUD/USD – sometimes a signal that a reversal should not be far off.

GBP was actually the worse performing major currency overnight, and where concerns about the impact on the economy from soaring gas prices and what, in particular, this is doing to CO2 supplies which are essential to so many industrial process (from animal slaughtering to fresh food preservation to carbonating beer and soft drinks), is clearly a factor. 40% of UK CO2 supplies are a by-product of fertiliser production, where the two big UK producers have ceased production given too-high gas prices – up 50% in the last month and 300% in the last year – rendering production unprofitable. The irony of a chronic shortage of CO2 crippling the UK economy, when excess CO2 emissions are the prime source of global warming and climate change, is not lost on your scribe.

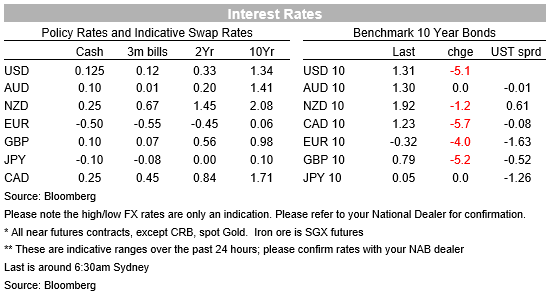

A text of a speech from RBNZ Assistant Governor Christian Hawkesby just released included this: “In the world of setting monetary policy, this translates to having confidence in the outlook for the economy, and inching in the right direction based on how the economy is likely to evolve. This is consistent with the observation that when there is a typical amount of uncertainty, and the risks are evenly balanced, then central banks globally tend to follow a smoothed path and keep their policy rate unchanged or move in 25 basis point increments”. This likely takes the market somewhat off the scent of a 50bp OCR rise next month, where as of yesterday the money market priced for about 40bp of tightening out of the October 6 meeting.

Bond markets have received a decent safe haven bid everywhere overnight, notwithstanding the proximity of the FOMC decision (4:00am Thursday AEST), with 10-yr treasuries off 5bps and following a 4bp fall in equivalent German Bunds and 5bp drop in UK gilts. Commodity prices have ended Monday in a sea of red, including crude oil down +/- 2% despite news that the US is relax travel restrictions for UK and EU citizens who are fully vaccinated. Copper is down 3%, leading the falls in base metals.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.