Coming in for landing in a heavy cross wind

Insight

US payrolls came in softer than the consensus (235k vs. 733k expected), but a soft print was widely expected given the weakness seen in high frequency indicators such as HomeBase. The surprise for markets was more on Average Hourly Earnings which were stronger than expected

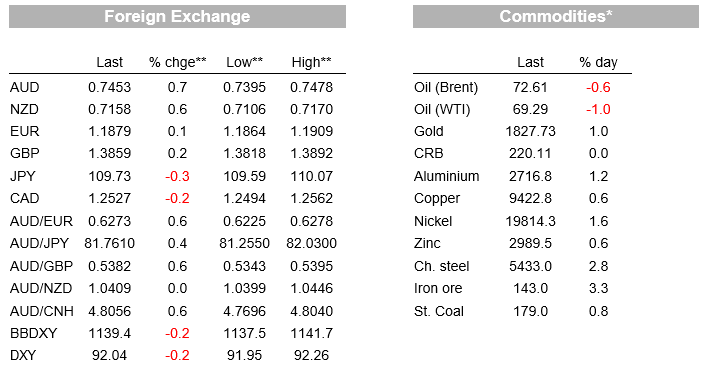

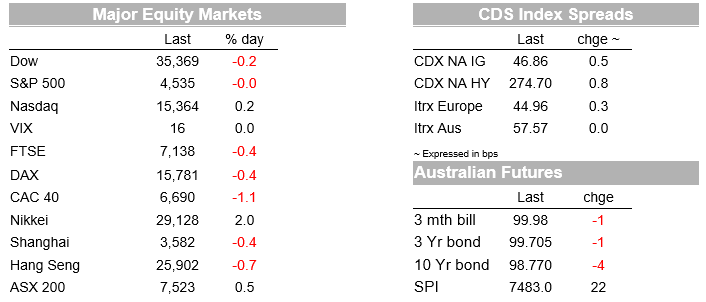

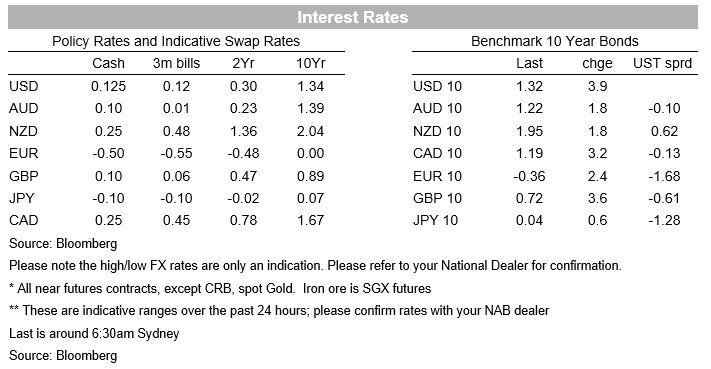

US payrolls came in softer than the consensus (235k vs. 733k expected), but a soft print was widely expected given the weakness seen in high frequency indicators such as HomeBase. The surprise for markets was more on Average Hourly Earnings which were stronger than expected (0.6% m/m vs. 0.3% expected). That probably explains the market reaction which was relatively mild for the size of the headline payrolls miss and for why yields rose (rather than fell in the wake of the report). The US 10-year yield ended up 3.9bps to 1.32% with the curve steepening, while the policy sensitive 5 year yields also rose by 1.8bps to 0.78%. Over the past week the 10yr yield is little changed along with the 5yr. There was little change in Fed rate hike expectations, with only a marginal downshift in pricing for 2022 and 2023, by around 1bp. The first Fed hike is still priced for March 2023. Steepening in the curve might also reflect prepositioning ahead of the $120b of bond supply this week given the Labor Day Public Holiday today in the US (and in Canada). Equity markets were little moved with the S&P500 ‑0.0% and hold onto its 0.6% rise over the week. Tech stocks outperformed (NASDAW +0.2) with cyclicals edging lower.

The USD (BBDXY -0.2%) in contrast continued its push lower (though did make up some ground later in the session as yields rose), ending the week down -0.7% which came in the wake of Powell’s Jackson Hole speech. The AUD and NZD were outperformers on Friday, both up around 0.6-0.7% to be around 2% higher on the week. Both appear to have firmly broken out of recent ranges and helping to lift NZD over the week has been hawkish RBNZ rhetoric, some signs of delta peaking, both seeing OCR rate expectations creep up with October now seeing a greater than 90% chance of a 25bp rate hike and 70bps of hikes are priced into the next three meetings. Kiwi rates are likely to be very sensitive to virus counts in the lead up to the October RBNZ meeting. As for other FX moves, it was mostly modest for EUR (+0.1%) which was little moved as was GBP (+0.2%), while USD/Yen eased -0.3% despite the rise in yields. For the week EUR and GBP are both up around 0.7%, while USD/Yen is down a marginal 0.1% and so far has shown little reaction to showing little reaction to PM Suga’s resignation – the ruling LDP will hold its leadership election on September 29.

First to Payrolls. Headline payrolls missed expectations at +235k against 233k expected. There were though favourable upward revisions to the prior two months of 134k, with July payrolls now at 1.053m compared to the initially reported 943k. While payrolls did miss the consensus, the whisper number was for a weak print given the weakness seen in the high frequency data such as HomeBase. Delving into the details reveals delta has halted labour gains in some industries with a flattening in hiring in ‘leisure and hospitality’ after the sector had averaged job gains of 350k a month for the past 6 months. Clearly the delta variant sweeping across the US has impacted and it is worth noting that employment in ‘leisure and hospitality’ is still down some 1.7m on pre-pandemic February 2020 levels. Overall payrolls are still down 5.3m on pre-pandemic levels while it would take around 7 months at the current trend pace of 750k to get back to pre-pandemic levels. Average Hourly Earnings within the report also continued to surprise, up 0.6% m/m against 0.3% expected and keeping alive fears of inflation being more than transitory for some, though inflation breakeven were little changed. The unemployment rate which is from a different survey fell to 5.2% as expected, from 5.4%.

The market reaction to the report suggests they are viewing the jobs slowdown as transitory for now, with the Fed still likely to taper, though more likely at November or December rather than as early as September. Dovish Fed Governor Brainard’s rule of wanting to make up 2/3rds of jobs lost as of December 2020 means there still needs to be another 2m worth of jobs to be made before tapering, and at the current trend pace of 750k it would take 2.7 months to get there, which puts the bias closer to December. Key to the ‘delta transitory’ narrative as far as the labour market is concerned is on expectations of further job gains as the enhanced $300 unemployment benefit payment end as of today and as in-person school resumes. The participation rate which was unchanged at 61.7% will be watched closely in this regard. Anecdotes amongst firms and strong job openings data continue to point to labour supply issues, rather than labour demand. Those notions were picked up in the ISM Services Index on Friday which was broadly in line with expectations at 61.7 vs. 61.6 expected. Symptomatic of a tight labour market, a widely run media story last week highlighted a McDonald’s restaurant in Oregon had called on 14 and 15 years olds to apply, having had limited success attracting staff even after it raised its minimum wage to $15/hour. Note Federal law allows 14-year-olds to work, with limits on hours.

Across the other side of the world, China’s Caixin PMI plunged to 46.7 in August, its lowest level since April last year, but the market looked through the data given the Delta outbreak in the country has since been brought under control. The report though did contain some interesting anecdotes on prices with output prices falling for the second time in three months and according to panel members, efforts to attract and secure new business had led firms to reduce their output prices over the month.

Central banks dominate with the RBA on Tuesday, and the ECB and BoC on Thursday. All three will be watched closely. The start of the week though will be quiet with Labor Day Public Holidays in the US and Canada.

A quiet day ahead with Labor Day Holidays in the US and Canada with markets closed in both countries. It is also very quiet in Australia with only ANZ Job Ads scheduled. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.