Online retail sales growth slowed in May following a fairly strong April

Insight

US yields continued to push higher ahead of the FOMC

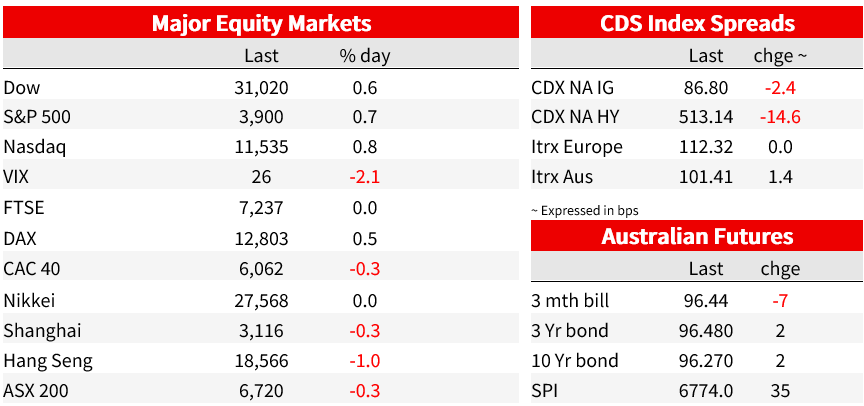

US equities close in the green but struggled to find direction in a start to the week that was light on for news flow. Holidays in Japan and the UK and coverage of the Queens funeral added to picture of a slow start to what will be a busy week. Yield curves have generally bear flattened. The FOMC, BoJ and BoE each meet from Thursday morning Sydney time.

After being down as much as 0.9%, US equities returned to positive territory through the afternoon and pushed higher in the final hour of trade led by megacaps. The S&P500 closed 0.7% higher, while the more tech focussed NASDAQ was 0.8% higher. Healthcare and Real Estate were the only sectors to record declines on the day, with vaccine makers knocked after President Biden said the pandemic is over in a TV interview. Moderna was 8.7% lower and Novavax fell 8.2%. European indexes were generally little changed. The Euro Stoxx 50 was flat.

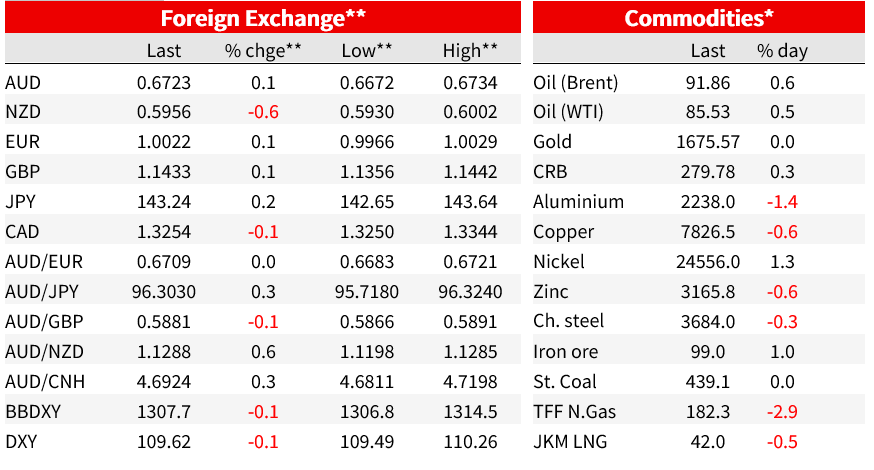

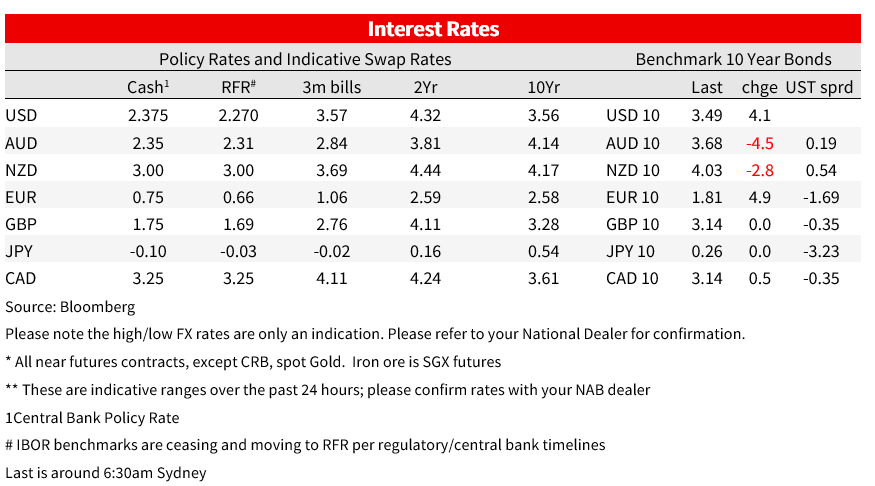

In rates markets, US short end yields continued to push higher ahead of the FOMC meeting. The 2yr yield pushed another 7bp higher to 3.94%. That’s 55bp higher than it’s September low on 2 September and a fresh post-GFC high. The 10yr yield was 44 bp higher to 3.49%, the 2s10s inverting further to -45bp. The German 10yr yield was 5bp higher at 1.81%, while the 2yr was 8bp higher to 1.6%.

The futures market continues to price 80bp of tightening by the Fed this week , and added another 7bp to the peak rate priced for March 2023, now at 4.47%. Focus on Thursday morning, beyond the decision in September, will be on whether updated projections and Fed Chair Powell’s commentary can match that hawkish outlook. Of some interest was a WSJ article by Fed whisperer Nick Timiraos during the US morning that reported a late change at Jackson Hole from a more nuanced address to something much more blunt amid concerns investors were misreading the Fed’s intentions given the need to slow the economy to combat high inflation. Notably absent was any mention of a possible 100bp move this week.

In Europe, ECB Vice President Guindos said “the slowdown will not reduce inflation by itself. Monetary policy needs to contribute to ease inflation,” as he emphasised the need to avoid second round effects. Governing council member dove de Cos, in his first remarks since the 75bp hike earlier this month, emphasised that though “we will continue to normalize monetary policy ” but struck a less proactive tone, saying the pace and magnitude depends on the “materialization of risks to our medium-term inflation target” because actions have a maximum effect after 2 years. “It may not be desirable to force an excessively rapid convergence of inflation to 2%, due to the excessive impact on activity and employment that this would entail.”

Moves in currency markets have generally been small. The DXY lost 0.1%, with movements against most of the G10 currencies under 0.3%. The dollar rose 0.25% against the yen alongside the push higher in yields, while the kiwi was the clear underperformer, down 0.5% to 0.5956 after trading at a fresh 2½-year low of 0.5930. The AUD was 0.1% higher at 0.6723 after trading as low as 0.6672 intraday, just shy of yesterdays low of 0.6670, before recovering through the US afternoon alongside the rebound in US equities.

The only economic data of note in the past 24 hours was a ninth consecutive drop in US Homebuilder sentiment in September. The NAHB index dropped 3 points to 46, its lowest since April 2020. Also on US housing, building permits and housing starts are published tonight.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.