NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The global reflation trade is not dead, says NAB’s Ray Attrill, as Fed speakers help markets further unwind their response to last week’s FOMC.

https://soundcloud.com/user-291029717/fed-cools-things-down-words-from-the-rba-later?in=user-291029717/sets/the-morning-call

Just checking my calendar to see that the September FOMC meeting begins, for us here, on the night of the 21st night of September, though I suspect Earth Wind and Fire weren’t in receipt of the Fed calendar when they penned this classic in 1978.

Latest smoke signals from the Fed, care of Jerome Powell in testimony just finished, NY Fed President John Williams and too the ‘normally hawkish’ Cleveland Fed President Loretta Mester, all point to September as the meeting when the Fed is, on current trends, most likely to declare that substantial further progress towards their goals has been achieved, or is being achieved, enabling them to give advance notice that the QE tapering process can begin in coming months. In our view, this is still most likely not until the start of 2022). Their comments have seen markets row back somewhat from their largely position-driven convulsions last week but where the fundamental catalyst was fear that the process of tapering and then tightening could be concertinaed into a significantly shorter time frame than the FOMC collectively signalled three months earlier.

After a non-market moving prepared testimony from Fed chair Powell overnight, the text of which was known during our morning yesterday, it has been subsequent Q&A comments that have proved market moving. Powell says that he ‘expect strong job creation should arrive by the fall’ (technically not until the 22nd September as it happens, the last day of the aforementioned FOMC meeting – how about that for a coincidence?). The Fed chair also opined that it is ‘very, very, unlikely’ we will see a repeat of the 1970s inflation experience and that high inflation is temporary and ‘will abate’.

Also of note given her traditionally hawkish credentials, the Cleveland Fed’s Mester says she expects more ‘clarity in September’ on progress towards the Fed’s goals and that we are ‘not at a point to dial back accommodation’. San Francisco Fed President Mary Daly (who to date has been characterised as dovish) said that substantial further progress ‘is within our line of sight’. And to round out Fed speakers, another of the ‘big three – along with Powell and Rich Clarida – NY Fed President John Williams said that we are ‘not close’ to substantial progress.

The market upshot of all this has been to see the US yield curve (very) mildly bull steepen after last week’s dramatic flattening as the proliferation of earlier curve steepening trades were subject to mass liquidations, doubtless in part forced by financial institutions’ risk managers. 2 and 5-year US notes are down 2.5-3bps, while 10s and 30s are down a slightly lesser 2bps.

US equity market have closed with the S&P500 up 0.5% and the NASDAQ +0.8%. All S&P sub-sectors bar real estate and utilities are in the green, headed by a 1% gain for consumer Discretionaries and 0.9% gains for IT.

On the real estate front, US may Existing Home Sales fell by a smaller than expected 0.9% though sales are now 13% of their peak. Prices though are 23.6% above their trough, a familiar figure (20%+) across much of the globe where banks have been doling out mortgages at 2% or less for the past year or so fixed for 2-3 years (and not much more than this for 30-years in the United States). The only other data points to note have been the Richmond Fed manufacturing index, up to 22 from the (unchanged) 18 expected, and in Europe, Eurozone consumer confidence which lifted to -3.3 from -5.1, much as expected.

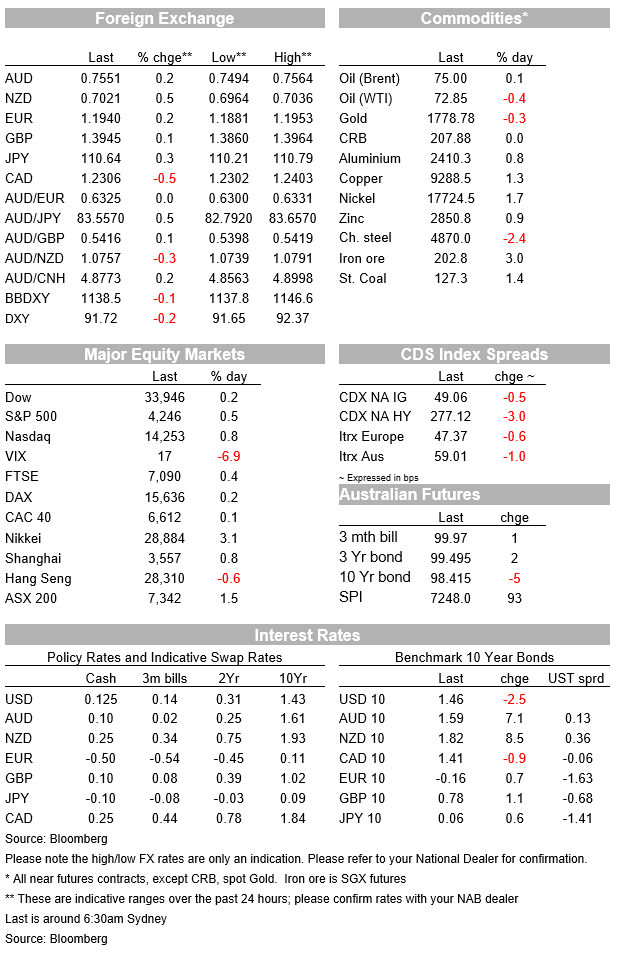

In FX, the USD has eased back some more, the DXY index off 0.2% and broader BBDXY a lesser 0.13%. the ultra-high beta NOK has been the best performing G10 currency (+0.6%) hardly surprising given that Brent crude oil prices have held the break above $75 (post 2019 high) seen early in our day yesterday. After than NZD has fared best, +0.5% and now back on to a 0.70 handle (0.7021 now) with AUD lagging somewhat, up only 0.25% but above 0.7750 having fallen briefly back below 0.75 post Tuesday’s local close. Other commodity prices are also mostly firmer, including a 1.3% rise in copper and 1.7% for nickel, while after iron futures, which dropped by more than 4% on Monday, are up just under 1% now.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.