The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

Globally equities had been dampened on Monday morning but equities are back on the rise in the US.

From zero to hero in no time flat, zero to hero just like that – Hercules sound track

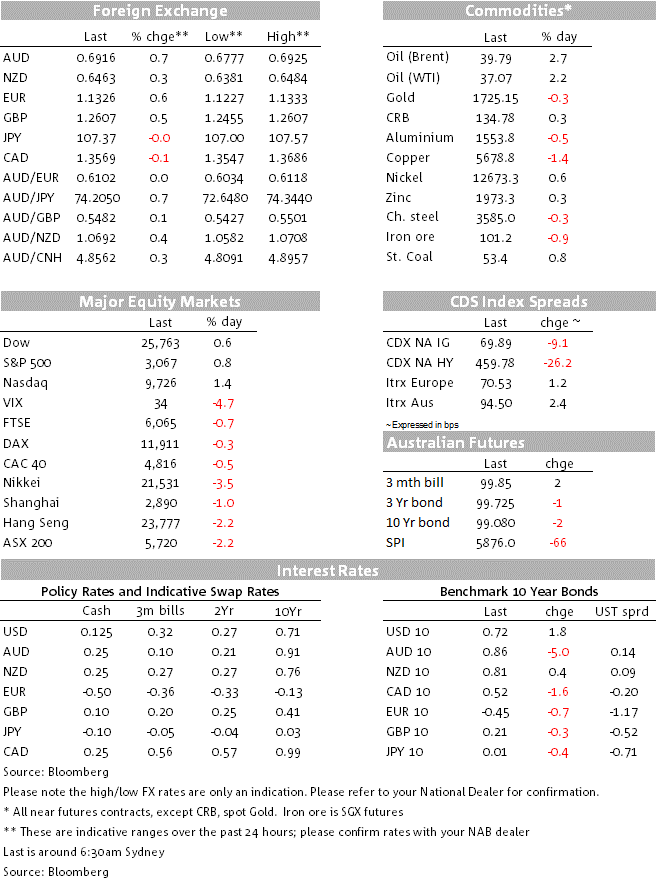

When your scribe was departing the study for the kitchen yesterday evening, you couldn’t give the AUD away at 68 cents. Back in here this morning and you can’t buy it at 69 cents. That’s more than 2% turnaround (these are big points down here) and there should be no surprise to learn that the move has coincided with the S&P 500 turning a 2% loss in the futures contract at 5pm Sydney time into a gain of more than 0.8% at the New York close. The NASDAQ has staged an even more impressive rebound, up 1.43% and where a Reuters report that the US government is about to issue a rule allowing US companies to work together with Huawei on standards for 5G networks has evidently played a part.

The news seemingly responsible for the smart reversal in risk sentiment more broadly has been that the Fed is about to embark on a programme of buying individual Corporate bonds. This Secondary Market Corporate Credit Facility (SMCCF), worth up to $250bn, was announced back in March recall, where the Fed said it would buy so called ‘Fallen Angels’, Investment Grade (IG) credits which had since the start of the pandemic seen their rating cut to no more than two notches below the BBB IG threshold, as well as High Yield ETFs. To date though, the Fed has done no more than purchase some $5.5bn worth of ETFs. Now the programme just got real. More than a few large institutional fund managers have since March publicly adopted a strategy of ‘buying what the Fed’s buying’ – something very much in evidence in the last few hours.

There was also some relatively positive US economic news last night in the form of the (New York State) Empire manufacturing survey, which jumped from -48.8 in May to -0.2 in June, vastly better than the -29.6 expected. The Empire survey is one of the first regional manufacturing surveys, and was evidently helped by New York being among the first regions to start exiting social distancing restrictions. It nevertheless offers hope that other regional surveys will also show sharp improvements as the June survey calendar unfolds. We also has a dramatic improvement in US Existing Home Sales, down by 56.8% in April but up 56.9% in May.

On the political and economic front was not great. The state-run Global Time ran an Op-Ed saying that Australia couldn’t assume that it was immune from any threat to include iron ore in the range of Australian goods and services imports that China might place restrictions on, even if it hurt its own short term economic interests to do so. The Op-Ed is pointed in saying that Australia started the diplomatic spat between the two countries and emphasised Australian PM Morrison’s remarks late last week talking about Australia not succumbing to ‘coercion’ by China. The news was responsible for the iron ore price dropping below $100 yesterday afternoon and for the AUD/USD spending time below 0.68 prior to the subsequent ‘risk-on’ recovery in the offshore market.

The May China activity readings confirmed a further improvement in industrial production, fixed asset investment and retail sales, but the production and sales numbers fell slightly short of expectations and while production is in YTD y/y terms now just 2.8% down on the same period last year, retail sales are still 13.5% below on the same basis. Whether this merely reflects the lingering effects of the virus in China or a potentially more enduring phenomenon – relevant not just to China but economies worldwide – is an important question in thinking about what the post-pandemic world looks like.

Bond markets have seen less volatility than equities and currencies, but US 10-year Treasuries have more than fully retraced the relatively sharp fall during our time zone yesterday (from 0.7% to 0.65%) to currently be 0.72%.

The AUD’s 0.8% gains has been straddled by a 1.1% rise in the NOK and 0.6% gain for the Euro, with all G10 currencies up against the USD which in (BBDXY) index terms is down 0.3%.

Locally we have the Westpac Q2 consumer confidence survey (it was 104.2 in Q1) as well as the weekly Roy Morgan confidence reading

Q1 House Prices will for the most part have pre-dated the start of lockdown and are expected to show a 2.5% increase and be +8.1% on a year ago.

The ABS’s weekly payroll jobs should show employment stabilised in the latter part of May (May full-month employment data comes on Thursday, where NAB expects to see a 75k drop in employment and rise in the unemployment rate to 7% ).

RBA Minutes this afternoon shouldn’t contain any surprises, policy having been left unchanged but the RBA acknowledging a somewhat less bleak view of the economy relative to earlier prognostication as social distancing restrictions lifted a little earlier than the government has previously led us all to expect.

The BoJ meets and should keep rates unchanged. The Bank may increase its funding facility, implemented in May to help businesses ride out the pandemic.

We get the UK labour market data for May, German ZEW survey (expectations seen up to 60 from 51.0) and in the US May Retail Sales and Industrial Production. Retail Sales are seen bouncing 8% after the 16.4% April fall (and by 5.3% ex-autos after -17.2%) and production by 3.0% after the -11.2% April fall.

Fed chair Jay Powell testifies before the Senate Banking Committee, where we have already had the (non-market moving) formal testimony published last week and it’s unlikely we’ll learn much more about Fed thinking tonight.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

The NAB Commercial Property Index lifted to an 8-year high in the March quarter, continuing the run of improvements seen in recent quarters.

Insight

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.