Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

The Fed delivered a unanimous 75bp hike as widely anticipated.

https://soundcloud.com/user-291029717/fed-hikes-75bp-no-forward-guidance?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

The Fed delivered a unanimous 75bp hike as widely anticipated, but the market reaction indicates a Fed not as hawkish as feared. The US dollar is lower, yields are lower, although the initial rally has been largely retraced, and equities higher.

The FOMC hiked 75bp, taking the target range to 2.25-2.5%. Guidance remained unchanged that ongoing increases in the target will be appropriate with only minor changes to the press statement, but importantly among them was a comment that activity was picking up is dropped in favour of an acknowledgement that “recent indicators of spending and production have softened.”

You could have been forgiven for interpreting Powell’s post-meeting press conference as hawkish. The Fed Chair repeated he was looking to get policy to a ‘moderately restrictive’ stance, where the current level is around neutral. And while generally looking to opt out of forward guidance, did pointed to the June dot plot as the best guide for policy. That implied rates of 3.25-3.5% by year end, or another 100bp over the next three meetings. Powell didn’t rule out another 75 hike in September, but said rate decisions would be data dependent. He also said that failing to deal with inflation would make it harder to deal with later on, growth needed to slow below potential, his own instinct was that the natural rate of unemployment is higher and the job market needed to soften.

For markets, however, the commentary was evidently less hawkish than feared. Powell said “we’re getting closer to where we need to be” after front-loading hikes and that “at some point it will be appropriate to slow down. ” That’s perhaps self-evident as the current pact of hikes can’t be sustained indefinitely, but could also suggest more data dependence in the near-term. Powell said that it’s time to move to a meeting-by-meeting basis, and refrain from specific guidance, leaving space to be reactive to incoming data. Market pricing to year-end is in line with the June dots, but has around 50bp of cuts priced in over 2023. The median FOMC participant projection in June saw the fed funds rates ending 2023 higher than 2022.

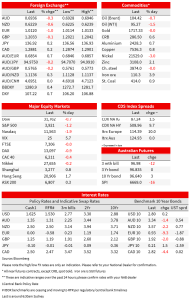

US rates were down sharply on the Fed. The 2yr yield dropped around 10bp and the 10yr was initially off around 6bp. Curves steepened sharply, with the 2yr yield largely holding onto its declines, sitting around 2.98%, while longer end yields reversed higher. 10yr yields bounced off their post-FOMC low of 2.72% to sit around 2.79%, down 2bp on the day but currently above their levels immediately prior to the FOMC.

The more dovish interpretation was also evident in currency markets. The dollar fell on the DXY, down 0.7% and losing ground against all G10 currencies. The euro was 0.8% higher to 1.0199. The AUD was 0.8% higher at 0.6996 after briefly touching above 70c, reaching an intraday high of 0.7012. For the aussie, the USD move on the back of the FOMC dwarfed the reaction to the domestic CPI data (more below).

Equities were higher ahead of the FOMC, helped by better-than-feared earnings from both Microsoft and Alphabet. Microsoft was 6.7% higher, helped by upbeat guidance for the companies full-year outlook. Alphabet gained 7.7% as sales growth slowed less than expected. The S&P500 was up around 1.5% heading into the Fed, the reaction to Fed commentary seeing the rally extend with index closing 2.6% higher. The Nasdaq outperformed, up 4.1%, while the Dow gained 1.4%. Earlier, European equities were also higher, the Euro Stoxx 50 up 0.9%.

Australian inflation data yesterday printed broadly as expected, but importantly failed to provide the upside surprise that the market was fearing. Headline CPI came in at 1.8% q/q and 6.1% y/y (consensus 1.9/6.3) and the more closely watched core trimmed mean measure rose 1.5% q/q which was exactly in line with consensus. There was an upward revision to the past quarter helping push the core y/y rate to 4.9% y/y. Inflation clearly is running hot with trimmed mean inflation at its highest quarterly rate since 1990. This should keep the pressure on the RBA to continue to move quickly towards a more neutral setting of policy. The market reaction suggested markets were braced for an upside surprise. The AUD fell around 0.5% on the data, while RBA pricing, which had been implying around a 30% chance of a larger 75bp hike at the August meeting next week, fell back to just 49bp priced. By the end of the year, market pricing now sits at 3.1%, from 3.42% a day earlier. NAB sees the RBA moving by 50bps in August and September and the cash rate getting to 2.85% by November 2022.

In other data flow, the last batch of GDP partials in the US came in on the strong side of expectations, narrowing the chance of a second consecutive negative quarterly GDP print in tonight’s advanced Q2 GDP read. Durable goods order jumped 1.9%, well above consensus for a 0.4% fall. The surprise was due to a surprisingly resilient aircraft component. Excluding transportation, order were up 0.3% vs consensus of 0.2%. The Advanced goods deficit fell more than expected to $98.2b from $104.3b and $103b expected. Wholesale and retail inventories also came in on the strong side. In contrast, pending home sales fell 8.6% in June as the housing slowdown continues.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.