Total spending grew 0.9% in June.

At the FOMC meeting this morning the Fed upped their growth and inflation forecasts, with the dot plots pointing to rate rises as soon as 2023.

https://soundcloud.com/user-291029717/fed-speeds-up-rate-hike-roadmap?in=user-291029717/sets/the-morning-call

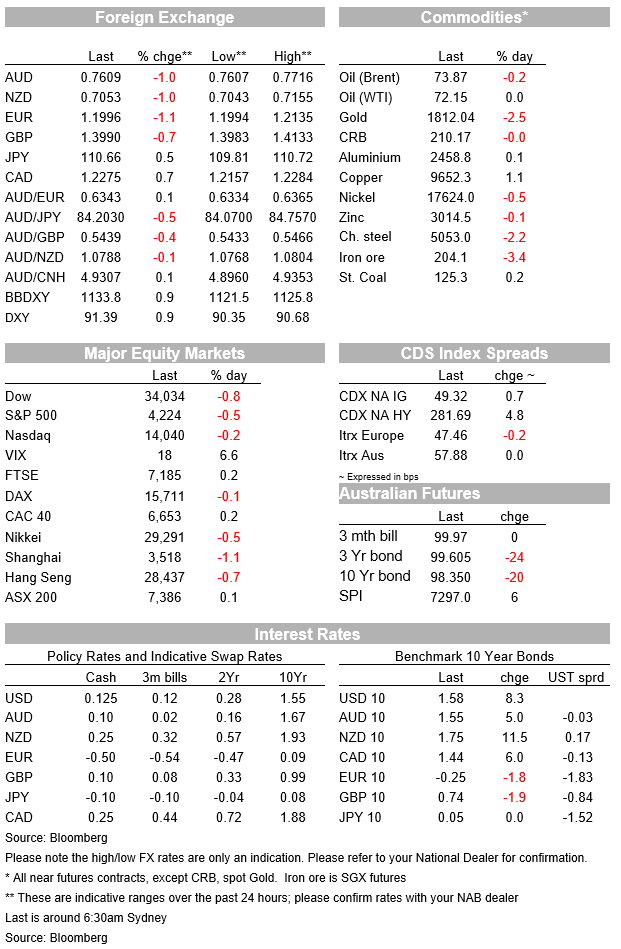

The new Fed ‘dot plot’ indicating that the median FOMC member now forecasts two Fed rate hikes in 2023, versus none in the March iteration, represented the hawkish surprise out of the June Fed meeting and on which most of the subsequent market reaction has turned. This means higher Treasury yields centred on the belly of the yield curve (5s up 11bps versus 8bps for 10s) and even more so in real terms given break-even inflation rates have fallen back smartly as the Fed restores a little of its inflation fighting credibility (by 8bps at 5-years and 6bps for 10s). This has seen a positive double whammy for the USD, where the DXY and BBDXY indices are currently up by 0.9% on Tuesday’s New York closing levels. Equities didn’t like the earlier-than-otherwise Fed rates messaging signal, though indices rallied back smartly in the last ‘hour of power’ to limit losses to 0.2% for the NASDAQ and 0.5% for the S&P500.

The FOMC statement itself didn’t display the clearly hawkish tilt that the Summary of Economic Projections (SEP) accompanying it did, with the Fed merely repeating the April line that ‘inflation has risen’ largely reflecting transitory factors’ and making no change (of course) to the Fed’s key policy rate or its $120b/month bond buying pace. It did make a technical adjustment to its Interest on Excess Reserves Rate (IOER) from 0.10% to 0.15%, something many had expected at some point by way of response to the downward pressure on the Fed Funds rate in recent months from the amount of excess liquidity sloshing around in the money market.

There wasn’t much change to the Fed’s economic projections, except for a substantial upward revision to core PCE inflation this year (from 2.2% y/y to 3%). The Fed’s medium-term projections are consistent with the current inflation pressures proving temporary, as core inflation is projected to fall back to 2.1% in 2022 and 2023 (which already has some observers raising an eyebrow at the Feds rates messaging juxtaposed against inflation projections indicating that all of the current upward pressure is expected to prove transitory). The unemployment rate forecasts are almost identical to March (4.5% at end-2021, 3.8% at end-2022) even as GDP growth for this year was revised up by 0.5% to 7%. In the press conference, chair Powell acknowledged that inflation has increased ‘notably’ and is likely to remain elevated, without saying for how long..

So the market reaction was all about the ‘dots’, showing that 13 of the 18 person FOMC see rates rising in 2023 versus only six previously, and with the median forecasting jumping straight to two hikes from none. For 2022, 7 out of 18 now see first rate hike (two of whom forecast two hikes, from one previously). The ‘long run’ median dot remains at 2.5%.

On the question of tapering of the Fed’s current $120bn QE bond buying programme, in the ensuing press conference Powell said ‘we’re taking a ‘meeting by meeting’ approach to assessing the progress we’re making to the ‘significant further progress’ goal, but which he stressed was ‘still a ways off’ . So the tapering discussion is now a live issue for each meeting, even if tapering itself if not going to begin anytime soon (and still conceivably not until next year – this would still leave plenty of time for tapering to be completed (say within a year) and for there then to be an interval before a first rate hike, as per previous Fed guidance).

Immediate market reaction to the Fed’s new SEP saw the S&P down by about 0.8%, though as noted above a lot of it retraced in the last hour, while in Treasuries 5-yar notes added an immediate 6bps (from 0.78% to 0.84%) before subsequently marching up to nearer 0.90%. The DXY index rose by just shy of 0.5% immediately, gains which have been almost doubled into the New York close. AUD and NZD are both off by a little over 1%, AUD to a low of 0.7607. The best that can be said for it here is that the sell-off hasn’t as yet taken it through the year-to-date low of 0.7532 seen on April Fool’s day. Most other G20 currencies have fared as badly or worse as AUD and NZD, with NOK – the recent currency market darling – down a cool 1.7%. EUR/USD is down by the same amount as AUD.

In other developments prior to the Fed, UK CPI came in higher than expected at 2.1% y/y, with core inflation at 2% so hitting the BoE’s 2% target for the first time since 2018. Inflation was boosted by pressures related to the reopening of the economy, with restaurant meals, clothing and recreational goods amongst the categories adding to inflation pressure last month. The GBP received a short-lived boost from the UK CPI data although there was little reaction in bonds. Canada May CPI was also higher than expected, with the average of Bank of Canada’s three core inflation measures rising to 2.3%, above the 2.1% market consensus and 2.1% in April. Headline CPI was 3.6% up from 3.4% and 3.5% expected. Spot a pattern here? On activity readings, US Housing Starts rose by 3.6% close to the +3.9% but off a sharply downwardly revised April (now put at -12.1% from -9.5%).

Released right on 5pm AEST last night, China’s May activity number disappointed expectations in all respects. Retail Sales came in at 12.4% y/y against 14.0% expected (down from 17.7% in April); Industrial Production was 8.8% down from 9.8% and 9.2% expected; and Fixed asset Investment 15.4% YTD y/y from 19.9% and the 17.0% consensus. The m/m numbers are showing a mixed read with industrial growth normalising but retail still relatively solid. Industrial Production is now 0.5% m/m from April’s 0.5% and March’s 0.6%; prior to the pandemic the m/m numbers were running at 0.8% a month. Retail Sales were 0.8% m/m from April’s 0.3% and March’s 0.9%; prior to the pandemic retail was running at 0.9% a month.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.