We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

WSJ’s Fed Whisperer Nick Timiraos wrote overnight if CPI on Tuesday comes in hot then the Fed could consider another 50bp increase in February.

A new week has reversed a good chunk of what we saw last week with equities down, yields up and the USD stronger. The key driver initially was a WSJ article by Fed whisperer Timiraos in which he hinted the US Fed could see the terminal rate higher than what market currently price (“brisk wage growth or higher inflation in labor-intensive service sectors of the economy could lead more of them to support raising their benchmark rate next year above the 5% currently anticipated by investors ”) and that should Tuesday’s CPI report be strong a 50bp increase in December could be followed by another 50bp in February. A stronger than expected ISM Services (56.5 vs. 53.5 expected and 54.4 previously) also played into this view with equities extending losses and yields lifting further.

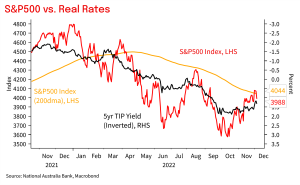

Into the last hour of power, the S&P500 is now -2.1%, almost reversing the 2.7% rise seen last week in the wake of Powell’s speech. It is also back under the 200-day moving average (see chart). Fed terminal pricing has shifted back to 5.0% by mid-2023 after ending last week at 4.92%. Nevertheless, there is also still 42bps worth of cuts priced in H2 2023. Yields are higher with 10yrs up 10.9bps to 3.60%, and 2yrs are up a similar 9.1bps to 4.36%. Moves have been entirely reflected in real yields with the 10yr TIP yield up 16.8bps to 1.21%, while the implied inflation breakeven has fallen by around -5bps to 2.39%. Likely weighing on breakevens is the oil price with WTI -3.4% to $77.23, itself weighed down by the move in yields and from the stronger than expected ISM Services.

The USD meanwhile is up 0.8% on the DXY. It has been a mixed 24 hours for the AUD and NZD with a stronger yuan in Asia (USD/CNH moved by around 1.2% to its low of 6.93, before reversing a little on USD strength to 6.97) supporting the antipodeans, with that support more than fully reversed with both the AUD and NZD -1.4%. USD/Yen is up a sharp 1.8% in sync with the rise in Treasury yields. The other majors were less moved with EUR -0.4% and GBP -0.9%.

First to the WSJ’s Fed Whisperer. Nick Timiraos wrote overnight that while a 50bp increase in December is likely, “…brisk wage growth or higher inflation in labor-intensive service sectors of the economy could lead more of them to support raising their benchmark rate next year above the 5% currently anticipated by investors”. (See WSJ: Fed to Weigh Higher Interest Rates Next Year While Slowing Rises This Month) That was likely read in the context of the Fed’s Bullard recently talking about Taylor Rules that suggest policy should be 5-7% and former Treasury Secretary Summers on the Friday saying a 6% rate “is certainly a scenario we can write…And that tells me that five is not a good best-guess.” Timiraos also notes if CPI on Tuesday comes in hot then the Fed could consider another 50bp increase in February.

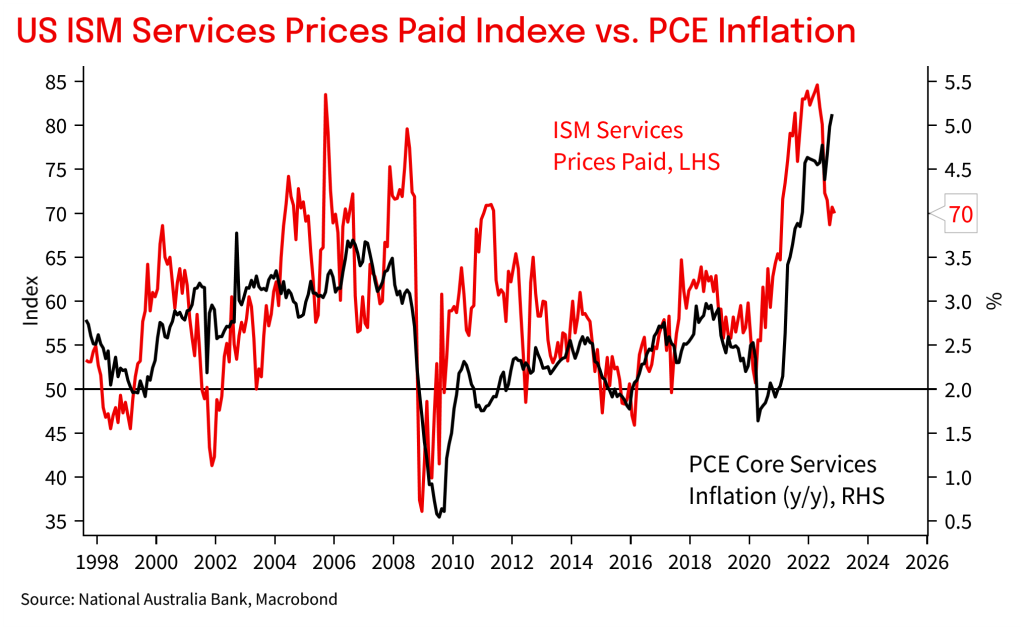

As for the ISM Services, it was still incredibly strong and contrasted sharply to last week’s ISM Manufacturing. The headline index printed at 56.5 vs. 53.5 expected and 54.4 previously. Details showed no slowing in orders with the New Orders Index at 56.0 from 56.5. Of importance to inflation, the Prices Paid Index was only down ever so slightly to 70 from 70.7 and suggesting little relief in services inflation ahead (see chart). On the positive side, supply chains appear to be healing with the Supplier Deliveries Index at 53.8 from 56.2. (see ISM Report for details). Although the ISM Services was very clearly strong, the rival S&P Services PMI came in weak at 46.2 with anecdotes of price pressures easing. It is unclear which measure we should take faith in here, though markets and the Fed tend to look more closely at the ISM.

To give you some perspective of the difference in the ISM Services vs. the S&P Services PMI, this is what S&P’s Chief Business Economist noted about their own survey: “The survey data are providing a timely signal that the health of the US economy is deteriorating at a marked rate, with malaise spreading across the economy to encompass both manufacturing and services in November,”, adding that “the data are broadly consistent with the US economy contracting in the fourth quarter at an annualized rate of approximately 1%, with the decline gathering momentum as we head towards the end of the year.” And interestingly also noted: “ A striking development is the extent to which companies are increasingly reporting a shift towards discounting in order to help stimulate sales…”. (see S&P Report for details).

Against the background of resilience, optimism around China continues. Yesterday, China and Hong Kong’s key equity market benchmarks rose 2% and 4½% respectively and the yuan strengthened following the weekend news that China was undertaking further easing of COVID-related restrictions, a further step away from the strict zero-COVID policy. These included reduced testing requirements which will allow more mobility and increased economic activity – Shanghai joined Beijing, Shenzhen, Guangzhou, Zhengzhou, and other Chinese cities in shifting toward reopening and most places will no longer require PCR results for access to local public transit and many shared spaces. A more comprehensive re-opening though will likely have to wait until after the winter with March/April still favoured by analysts.

Notwithstanding China pivot optimism, it is worth noting US tech names continue to report production interruptions from operations in China and also uncertain demand. Tesla was said to be planning to trim production at its Shanghai factory by around 20% from last month. The WSJ also noted production issues for Apple, with Apple also reportedly telling suppliers to shift some production out of China to Vietnam and perhaps India. Note a larger shift of manufacturing production out of China has the potential to increase costs to the supply chain.

Finally ahead of the RBA today, yesterday’s Business Indicators Survey showed a further acceleration in private sector labour cost growth. The private sector wage bill rose 2.9% q/q after 3.1% in Q2 even as employment growth slowed. Quarterly rates of growth of this magnitude have not been seen since the height of the mining boom back in 2007. Part of the rise in Q3 reflects higher award/minimum wages taking effect, but overall is very strong. Also with the report were consumption indicators which remained very resilient despite the real income hit seen by consumers and the tightening in financial conditions from higher rates. That overall highlights the need for the RBA to continue to hike rates and that it is too early to consider pausing. NAB continues to see the RBA hiking rates by 25bps tomorrow, and again in February and March, taking the cash rate to 3.60%. As for the direct read through to Q3 GDP on Wednesday, inventories were a little stronger giving a contribution of 0.4 to GDP growth, slightly ahead of NAB’s estimate of 0.3% (see NAB note AUS: GDP partials on the strong side, while private sector wages soar).

Chart 1: Macro chart of the day – not much relief in sight for services inflation from the ISM Services Prices Paid overnight

Chart 2: Price action chart of the day – US equities fail to break out of the 200day moving average

NAB Markets Research Disclaimer

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.