Online retail sales growth slowed in May following a fairly strong April

Insight

A sourer tone took hold over the past 24 hours, with equities lower and haven currencies, including the dollar, stronger.

A sourer tone took hold over the past 24 hours, with equities lower and haven currencies, including the dollar, stronger. But yields continued to push higher as markets await the FOMC, with the outcome of its 2 day meeting published 4am Sydney time tomorrow. Also before the week is out are meetings from the BoE, SNB and Norges Bank. The Riksbank kicked off a full week for central bank meetings, surprising expectations with a full point hike to 1.75%, opting to move urgently away from accommodative settings. In terms of data over the past 24 hours, Japan CPI came in a little stronger than expected, Canadian CPI a little softer. There is risk of further escalation in Ukraine as well, with news that, four regions in Russian-held territories in Ukraine will hold referendums 23-27 September on annexation.

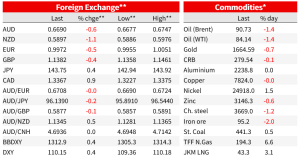

US equities were lower, failing to hold on to gains late in the US session yesterday. The S&P500 dropped 1.1% and the Nasdaq lost 1.0%. Not helping the cause overnight were downbeat earnings. Ford shares dropped over 12% after the auto maker warned that parts shortages and higher costs will hit earnings more than earlier expected in Q3. But losses were broad based, with all 11 sectors in the S&P 500 in the red. In Europe, the Euro Stoxx 50 was 0.9% lower, and the FTSE 100 dropped 0.6% as traders returned from the Monday holiday.

Currency moves also reflected the more skittish tone, with the USD up 0.4% on the DXY to 110.13, back above 110 but below the high reached earlier this month. The yen lost just 0.4% against the dollar and Swiss Franc managed a small gain. Losses were led by SEK and NOK, but the kiwi was not far behind, off another 1.1% against the dollar and falling as low as 0.5886, but now trading around 0.5900. The AUD was 0.6% lower at 0.6690.

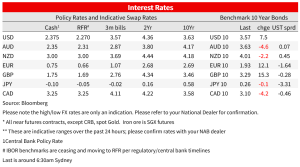

The Riksbank surprised with a supersized 100bp move to 1.75% in clear preference to get out of accommodative territory fast. The strong consensus among analysts was for a 75bp hike. The Riksbank projected rates path also moved higher and sees a peak of 2.5%, up from around 2% at the June meeting. For what its worth it suggests a slowing from here to 50 and then 25 over the next two meetings. Updated forecasts project an economic contraction of 0.7% next year, an 18% decline in house prices and inflation still remaining above target, just over 5%. An initial move lower in EUR/SEK on the announcement was more than reversed as focus shifted to the challenging economic outlook.

The bigger move from the Riksbank didn’t move the dial on Fed expectations for this weeks meeting with markets still pricing 80bp and seemingly well positioned for a 75bps hike alongside a hawkish update. Nonetheless, yields globally continued to push higher. The US 10yr yields was 7bp higher at 3.56%, the curve steepening a little with moves in the 2yr more muted. Larger moves were seen in Europe. The German 10yr was 12bp to 1.93, while the 10yr gilt yields surged 15bp to 3.29%.

Canada was an exception to the global push higher in yields as CPI data for August came in softer than expectations at -0.3% m/m and 7.0% y/y vs -0.1%m/m and 7.3%y/y expected. Negative inflation in the month was helped in large part by a 9.6% drop in fuel prices, but core measures also came in softer the expectations and the detail showed positive signs for a slowing in services inflation. The average of the three core measures watched by the BoC fall from 5.4% y/y to 5.2% y/y. BoC Deputy Governor Beaudry said inflation is still too high, but heading in the right direction. Market pricing did have a 20% chance of a 75bp hike at the next meeting, but pared that back to fully price a 50bp hike. The Canadian 2yr yield plummeted 12bp on the release, and was 5bp lower over the day to 3.75%.

Contrast that with Japan’s CPI, which saw 0.1ppt upside surprises on each of the three prints (headline 3.0% from 2.6%, ex-fresh food 2.8% from 2.4% and ex-food and energy 1.6% from 1.2%). Ex-consumption tax hike impact in 2014, the y/y core rate is highest since 1991. The recent ex-food and energy prints also tell a more inflationary story than the y/y rates. In seasonally adjusted terms, the 6m annualised is running at 2.8%, and the 3m annualised 3.7%. Although the magnitude of the pick up has taken the BoJ by surprise, it is still largely a cost-push story that is concentrated in goods, and so policy makers may still persist with their broader expectation that inflation will slow over 2023 as those factors wane and in the absence of clear domestic demand and wage growth drivers. The data plays to view BoJ may at least tweak its language on inflation this week (further downgrading the ‘temporary’ description of recent strength), though probably still not enough to get them over the line on a YCC shift as early as this meeting. October, when they will update inflation forecast, looks a better bet if something is to happen before Kuroda’s term expires next April (increasingly likely with political pressure on BoJ rising by the day as polls show higher inflation and a weaker yen is very unpopular).

US housing data round out the economic news overnight. US housing starts sharply beat estimates, up 12.2%m/m against forecasts for little change. That beat was largely on the more volatile multi-family dwellings, and so isn’t a signal of a turn in the trend. The more forward looking permits fell sharply, down 10% m/m against expectations for a 4.8% fall. The 3.5% m/m fall in single family permits was the 6th straight monthly decline.

In our time zone yesterday the RBA September Minutes showed the Board sees a clear case that rates still need to go higher amid very tight labour markets, ongoing elevated inflation and clear difficulties for the economy meeting the so far resilient level of demand. They also revealed that though opting for 50bp, the board considered 25bps September and the Minutes ended with the statement that “all else equal, members saw the case for a slower pace of increase in interest rates becoming stronger as the level of the cash rate rises.” That’s a strong signal that the pace of cash rate rises will shift back to the more normal 25bps increments at some stage soon, but the resilience of the data so far make another 50bp very possible in October.

In news overnight, four regions in Russian-held territories in Ukraine will hold referendums 23-27 September on annexation, which the Russian government would support. The NATO secretary general said “Sham referendums have no legitimacy and do not change the nature of Russia’s war of aggression against Ukraine.” The move risks an escalation in the war, enabling the Kremlin to claim that attacks within those regions would amount to an attack on Russia. In addition, Russia’s Parliament approved legislation that clears the way for military mobilisation.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.