On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

US and EU equities rebound overnight with mostly positive Omicron news lifting sentiment while company specific news have also helped the cause.

https://soundcloud.com/user-291029717/looking-ahead-to-a-better-2022?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

This is our last Markets Today for 2021. On behalf of NAB Markets Research we thank you for your readership over the year and hope you are able to enjoy a well-deserved and covid-free break during the festive season. Markets Today will resume on 17-January.

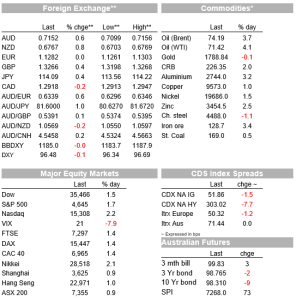

US and EU equities rebound overnight with mostly positive Omicron news lifting sentiment while company specific news have also helped the cause. Core yields push higher with the 5y UST yield up 7bps to 1.238%, a solid 20y UST auction played into a flattening bias in the back end. The USD is little changed with gains in commodity linked currencies offset by a retreat in safe haven pairs. AUD starts the day at 0.7152.

The rebound in equity markets that began during our session yesterday extended overnight with all main European indices ending the day with gains comfortably above 1% while US equity indices look set to end the day with similar gains . As we enter the last hour of NY trading, the S&P 500 is up ~1.6% with Energy and IT leading the gains up 2.67% and 2.2% respectively. Utilities and Consumer Staples are the underperformers, unchanged on the day. Meanwhile the NASDAQ trades at 2.26% currently, more than reversing yesterday’s decline of 1.24%.

Mostly positive Omicron news have helped lift sentiment with South Africa reporting a slump in daily infections to the lowest in two weeks . Inthe UK were Omircon infections continue to rise, but PM Johnson ruled out stricter pandemic rules before Christmas, easing concerns over a potential lock down over the festive season. The PM, however, urged caution noting that “the situation remains finely-balanced” and ministers may yet move to impose further curbs after December 25.

Encouragingly and potentially a game changer in the fight against Covid, the US Food and Drug Administration (FDA) is set to authorised a pair of pills from Pfizer and Merck to treat Covid as soon as this week. The pills are expected to stave off the worst for people who catch the virus.

Omicron news are lifting sentiment, encouraging markets to price a less malicious outcome from the new virus wave. Omicron is and will continue to have an impact on the global economy, but now there is prospect that its impact could be shorter and shallower. Favouring a positive outlook for 2022 with consumers and corporates well placed to support the economy next year, amid high levels of savings and employment.

US company specific news also helped sentiment with Micron Technology shares, the largest US maker of memory chips, surging on an upbeat forecast. Nike also outperformed as revenue in North America increased, offsetting a drop in China. Apple’s long-term credit rating was upgraded by Moody’s to Aaa from Aa1 with the credit agency noting Apples’ “exceptional liquidity, robust earnings that we expect will continue to grow over the next 2 to 3 years”.

The improvement in sentiment has also been reflected in the move up in core global bond yields. UST yields are higher across the curve with the 5y tenor leading the move, up 7bps to 1.238%. 10y UST now trade at 1.4771%, up 6bps over the past 24 hours. The 20y UST auction overnight was very well received stopping 2.3 bps below the market’s expectations, with strong demand across the board. The bid-to-cover ratio rose to 2.59x the highest level since June 2020. The Auction result played into a small flattening bias in the back end of the curve with the 30y bond lagging the move up in yields, up 3.8bps to 1.89%. Early in the session 10y UK gilts closed 10bos higher at 0.8730% while 10y bunds climbed 6bps to -0.3060%.

Moving on to the FX market, the USD is little changed in index terms with the DXY index at 96.498. Commodity linked currencies have outperformed buoyed by the lift in sentiment which has been accompanied by decent gains in oil prices ( ~+4%) while metals ( LMEX +1.6%) and bulk commodities have also gained ( iron ore +2.2%). NOK is up over 1% to 8.9391 while the NZD and AUD are not too far behind, up 0.8% and 06% respectively. The AUD now trades at 0.7154, not too far from our end of the year forecast of 72c, meanwhile NZD is at 0.6768, close to its intraday high. Safe haven pair are the under performers, with JPY down 0.4% (USDJPY at ¥114.10) and CHF down -0.3%.

On relevant news for the NZD, our BNZ colleagues note that overnight wholemilk powder prices fell 3.3% with average prices at $US3,867/T. This was lower than was anticipated by the market. In contrast to recent months, when prices were pushing higher, there were fewer buyers from South East Asia. It is not clear if this is holiday related, in which case little should be read into it as an indicator of what comes next, or if it is a bit more fundamental (SEA did buy a lot of skimmilk powder). Buyers from North Asia, read China, were present – buying well over half of the wholemilk powder sold.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.