Economic and financial market update

Insight

A combination of a US debt ceiling resolution alongside a mixed US jobs report, still favouring a June Fed pause, and news that China may be considering further support to its beleaguered property sector boosted risk sentiment (VIX sub-15), major equity indices closed the week with solid gain.

Where your load is light,Where your heart’s at ease

This is waking up, And feeling good, feeling good -Faithless

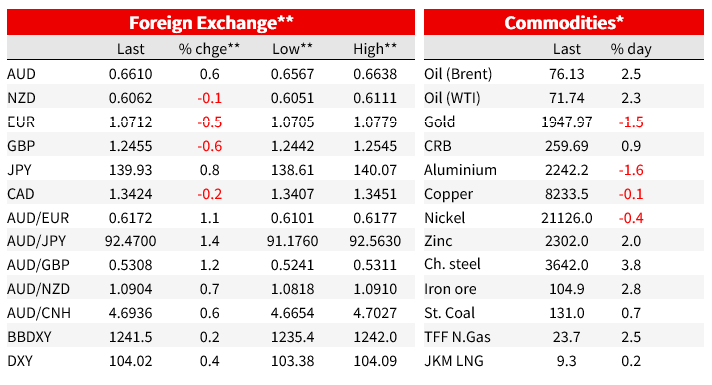

US Treasuries led a rise in core global bond yields with the curve bear flattening. The USD gained around 0.5% in index terms with EUR and JPY notable underperformers while the AUD led a commodity linked outperformance ex NZD. Oil prices spear headed gains within commodities. OPEC+ meeting over the weekend concluded with Saudi Arabia volunteering a million barrels a day cut in production.

The US May jobs report was a mixed bag. The better-than-expected payrolls number at 339k vs 190k expected plus 90k of upwards revisions to the previous two months suggests the US labour market remains in rude health. Of note too, the May’s 339k print was the 14th consecutive payrolls report to beat forecast. In contrast the May household survey provided a more pessimistic assessment of the US labour market with a 3-tick rise in the unemployment rate, from 3.4%-3.7%. Meanwhile, US Average Hourly Earnings (AHE) printed at 0.3%m/m, in line with expectations but below the downwardly revised 0.4% (from 0.5%) in the previous month. AHE is running at 4% annualised rate over the past 3 months, suggesting wages growth are no longer inflationary.

Positivity in the Equity market was also supported by resolution of the US debt ceiling saga, after the passing of the bill in the senate late on Thursday, markets closed the week with the assurance that the US will avoid default on federal government’s debt. On Saturday, with just two days to spare, President Biden signed the legislation lifting the nation’s debt ceiling.

Another piece of positive news on Friday came from China with Bloomberg reporting regulators were looking to provide further support to the country’s beleaguered property sector. According to people familiar with the matter, regulators are considering reducing the down payment in some non-core neighbourhoods of major cities, lowering agent commissions on transactions, and further relaxing restrictions for residential purchases under the guidance of the State Council.

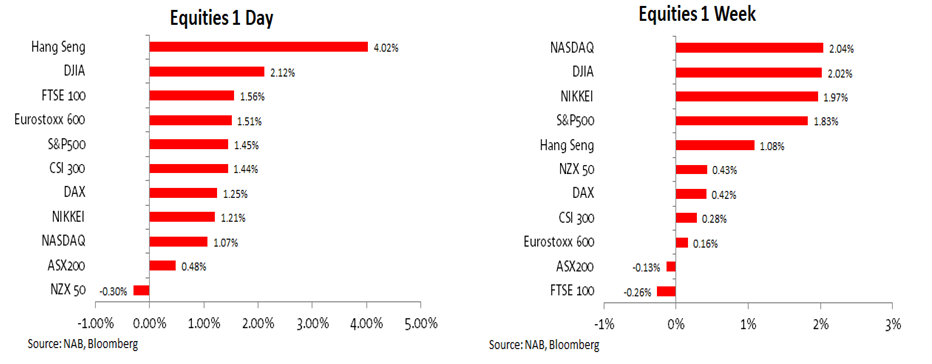

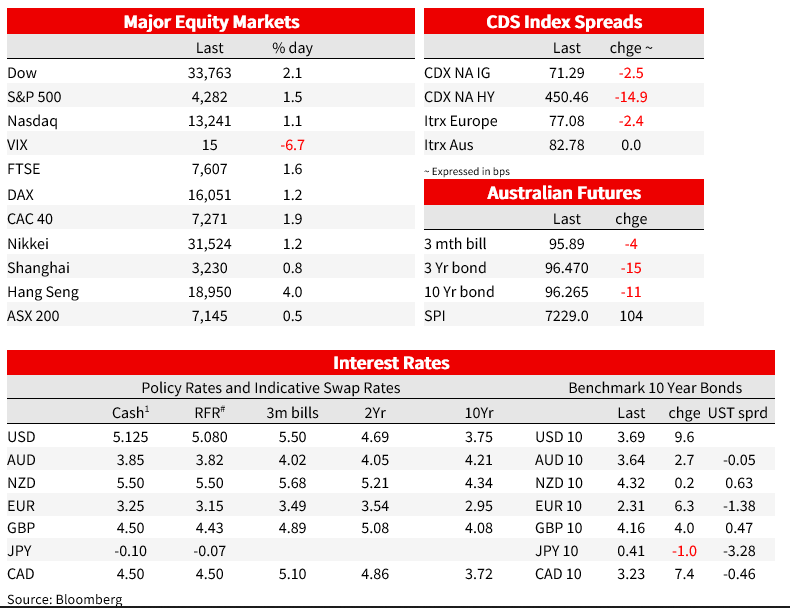

So from macro perspective the prospect of a Fed pause in June (more on this below), evidence of a cooling US labour market (ease in wages pressures) plus China looking to provide further support to its economy, provided a nice positive backdrop for the equity market to perform. Indeed, all major equity indices from Asia, Europe and the US close the week solid gains while the VIX ended the week just below 15..

The Dow spear headed US equity market gains, jumping 2.12% on Friday with the S&P 500 1.45% while the NASDAQ climbed 1.07%. For the week the Dow rose 2.02%; the S&P gained 1.83% and the Nasdaq rose 2.04%. Earlier in the day the Hang Seng closed 4.02% higher with US-listed Chinese equities also making decent gains, as did shares of European companies with strong ties to China, such as luxury goods makers and the mining sector. The Eurostoxx 600 gained 1.51% with Japan’s Nikkei +1.21.

Looking at the weekly performance, the NASDAQ close at the top of the leader board (NVIDIA no doubt a major contributor) at 2,01% with the Nikkei and S&P 500 recording gains just under the mark . Our S&P/ASX200 and the UK FTSE 100 were the week’s underperformers, down 0.13% and 0.26% respectively.

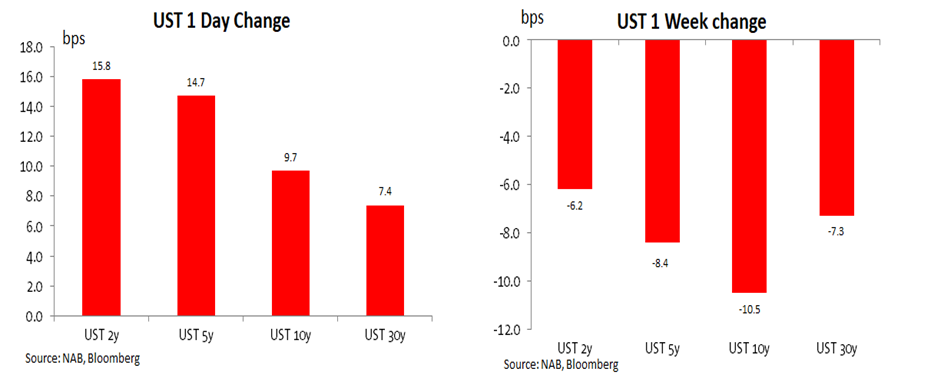

Following the release of the US May jobs report, US Treasuries led a move up in core global bond yield with front end yields recording the biggest gains. The UST curve bear flattened with the 2y Note climbing 16 bps to 4.501% while the 10y rate gained 10bps to 3.695%. In a similar fashion, the German curve also bear flattened on Friday with the two-year Bund yield rising 9bps to 3.54% compared with 6bps on the 10-year rate to 2.95%.

The US jobs data boosted expectations of Fed hikes over coming months. Bets on a hike at the June 13-14 meeting next week rose, although investors still see a bigger chance the Fed will pause. A 25bps hike next week was priced 31% probability on Friday’s close, up from 24% a day earlier. Meanwhile the probability of a 25bps hike in July climbed from 40% to 50%. Of note too, expectations for Fed rate cuts were also pushed out in time with the Fed funds rate seen at 4.99% by the end of the year compared to 4.85% on Thursday.

Notwithstanding the rise in yields on Friday, a look at the weekly chart reveals a broad base decline in core global bond yields over the past five days. 10y UST yields are down 10bps relative to levels a week ago while a reassessment of Europe’s inflation outlook, after the weaker than expected May CPI figures, shows 10y Bunds down 22bps relative to levels a week ago while Italian BTPS are -32bps.

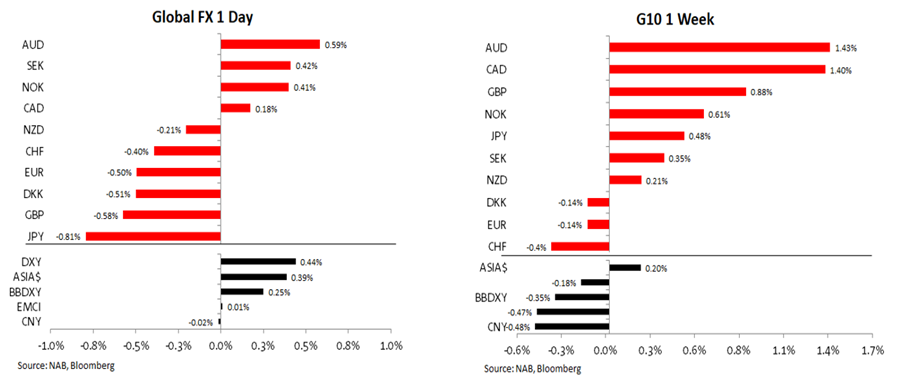

The USD was on the backfoot prior to the US Jobs data release, but the better-than-expected headline numbers and rise in UST yields triggered a reversal in fortunes. In index terms the greenback close between 0.25% to 0.44% stronger on the day with the euro and JPY notable underperformers within G10. The euro fell 0.5% on the day, closing the week at 1.0707 while the move up in UST yields boosted USD/JPY, up 0.84% to just under the ¥140 mark.

The AUD was the top performer on Friday, retaining most of its minimum award wage increase gains recorded during our time zone. On Friday, Australia’s Fair Work Commission determined an increase to minimum award wages of 5.75%. That compares to an increase of 4.6% for most awards in last year’s decision and takes effect on 1 July. The decision triggered an increase in RBA rate hike expectations and boosted the AUD. The market now prices a 40% chance of a 25bps hike this week and 0.89% chance of a hike in July, up from 21% and 44.5% respectively on Thursday. The AUD closed Friday 0.5% higher at 0.6607 and starts the new week at 0.6617. The NZD had a more subdued Friday, closing the week at 0.60585, little changed on the day and indeed on the week too.

Looking at the weekly chart, the AUD was the G10 outperformer over the past 5 days, up 1.43% with CAD close behind, up 1.40%. The RBA and BoC meet this week and in both instances the market is leaning towards a no hike, but with pricing for a hike at around 40% for both, there is still a non-negligible chance the RBA and or the BOC could hike.

The USD lost ground during the week (BBDXY -0.35%) and in addition to gains from AUD and CAD, the greenback also underperformed against GBP with the pound up 0.8% on the week to 1.2459. For the week the EUR/USD eased 0.23% while JPY gained 0.48%.

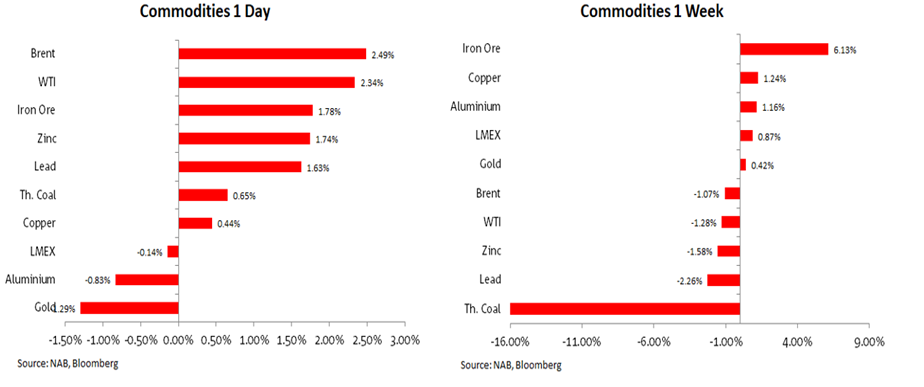

On Friday news that Beijing will likely roll out policy stimulus to reinvigorate a faltering economic recovery, lifted commodities including copper (0.44%) and iron ore (1.78%). Gold fell 1.53% to $1,947 and for the week it was flat. WTI crude rose 2.52% to $71.74 and Brent was +2.49% to $76.40. Oil is expected to rise today after the OPEC+ meeting over the weekend concluded with Saudi Arabia volunteered a million barrels a day cut in production.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Economic and financial market update

Insight

Online retail sales growth slowed in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.