Coming in for landing in a heavy cross wind

Insight

USA equities came bouncing back after yesterday’s sharp response to the higher than anticipated CPI numbers.

https://soundcloud.com/user-291029717/fewer-jobless-claims-and-hopes-of-a-faster-recovery?in=user-291029717/sets/the-morning-call

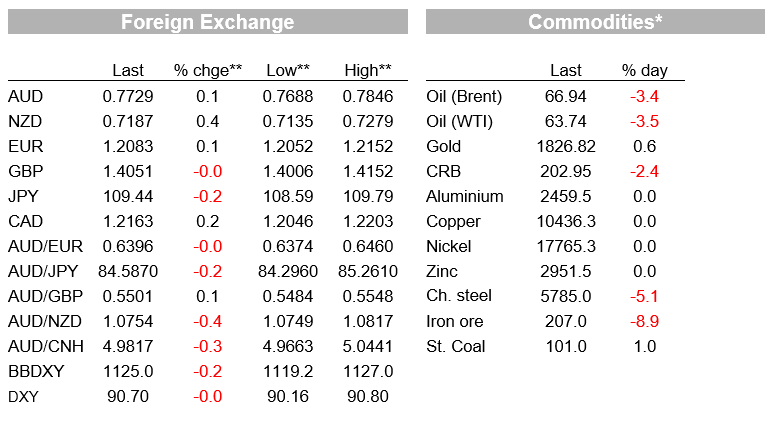

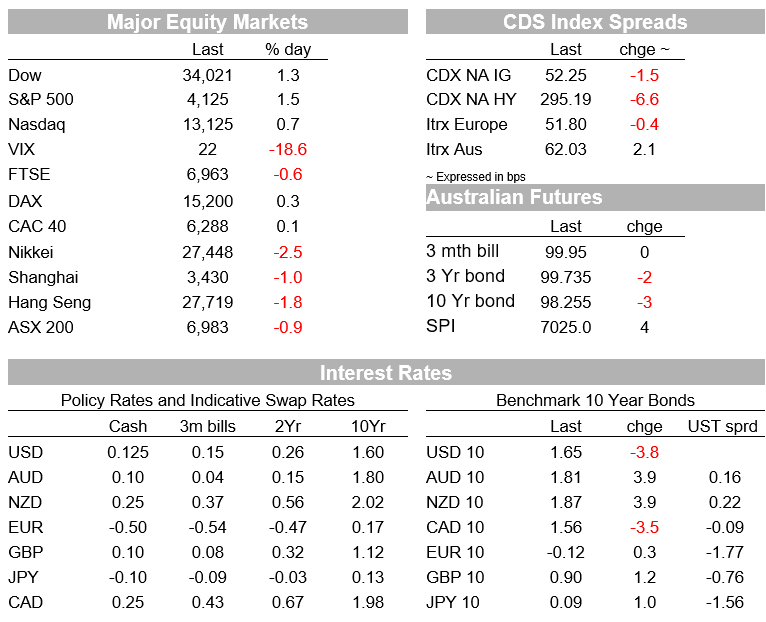

The torpor that set in after the US inflation scare that jolted US markets on Wednesday has dissipated from the NY open overnight. Equities are in the green, US bond yields are somewhat lower, while the part-rally in the USD ran into a road-block, including from some appetite for risk and steadier to higher European and UK bond yields. The AUD has opened in APAC this morning perched at around 0.7725/30, having tested the figure during the London session in the wake of a weak post-CPI APAC session in early trading London time.

Commodity prices were softer overnight, including base metals and iron ore, the former from the general market volatility as an excuse for some retracement from the recent reflation bull run, the latter after the Chinese Premier urged his country to deal with the commodity price surge and its impact. It’ll be interesting to see how the commodity complex trades today and into next week. We also note there are some meaty readings coming tonight on the state of the US consumer from April Retail Sales and the first cut of May Consumer Sentiment from the University of Michigan survey. (More on these further below under Comin Up.)

Fed President Barkin and FRB Governor Waller have been speaking overnight, acknowledging the fast-paced recovery of the US economy and that they also see the inflation surge as transitory. Waller noted for example that the Fed won’t be over-reacting to temporary inflation overshoots and that while he sees inflation above 2% in 2021/2022, he expects it to be back at its goal in 2023. By the same token, on the activity front, he wants to see the May and June jobs report before thinking of tapering. Barkin noted that spending has come back faster than employment, that consumer confidence is skyrocketing, housing is booming. On the inflation front, he noted that long term disinflationary forces may curb expectations.

In the past hour Fed President Bullard has said that inflation is likely to be “meaningfully above” 2% and that some rise in inflationary expectations would be welcome. He expects very strong job reports during the summer. The latest weekly batch of US Jobless claims continue to point to further reduction in jobless numbers and an improving tone in the US labour market, notwithstanding last Friday’s disappointing non-farms report.

The latest NY Fed Weekly Economic Index for the week ended May 13 – configured on high frequency data such as jobless claims, electricity output, fuel sales and the like – indicates annual US GDP growth of 11.45% y/y, pretty much in line with the 12.2% current consensus for Q2 GDP in year to terms. Finally, on the US inflation front, the April PPI exceeded expectations, headline PPI up to 0.6%/6.2% from 1.0%/4.2%, core PPI up to 0.7%/4.1% after 0.7%/3.1%, annual growth boosted by weak prices in the teeth of the pandemic a year ago. The likes of airline passenger services, vehicle rentals, lumber, steel products, food retailing, and hardware retailing and building materials were all adding to the upstream inflation pressure in April.

Yesterday’s REINZ housing data suggested the NZ property market was still firm in April, a month after the government announced new policy measures to dampen investor demand. Sales were the strongest for an April in five years while inventory remained very low. Monthly house price growth moderated somewhat, but only to 2.0% in April, from 2.7% in March, seasonally adjusted. Our BNZ colleagues still think it will take a few months to properly judge how the housing market is responding to the government’s recent policies.

Adding more to the bullish tone of housing in most advanced economies, the latest reading from the respected UK RICS House Price net balance for April soared further to +75% from 62% (forecast 62%), the highest for 33 years, the balance having been at -30% almost a year ago. It’s not only been boosted by low rates but the extension of the stamp duty-free threshold of £500K to the end of June and continuing at a tapered capped rate of £250K to the end of September.

Finally, on the COVID front, the US CDC announced this morning that those fully vaccinated can shed their masks, another reminder of more light and freedom and way out from the well advanced vaccination program.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.