Online retail sales growth slowed in May following a fairly strong April

Insight

Fed chair Jay Powell’s address to the Kansas Fed’s Jackson Hole Symposium on Friday was short and as far as equity market investors were concerned, bitter not sweet.

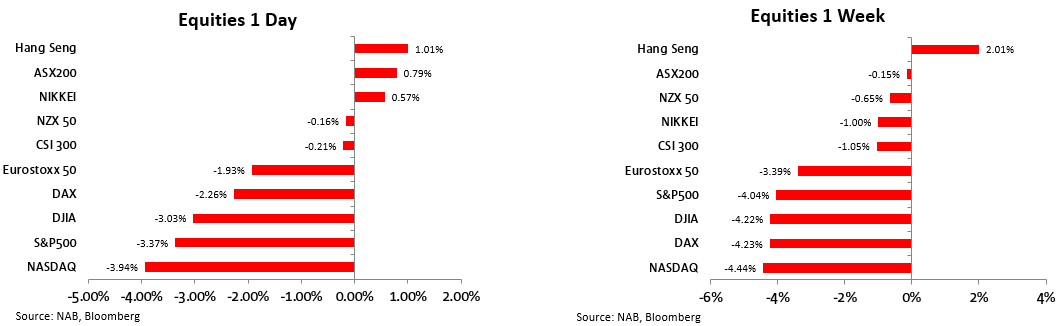

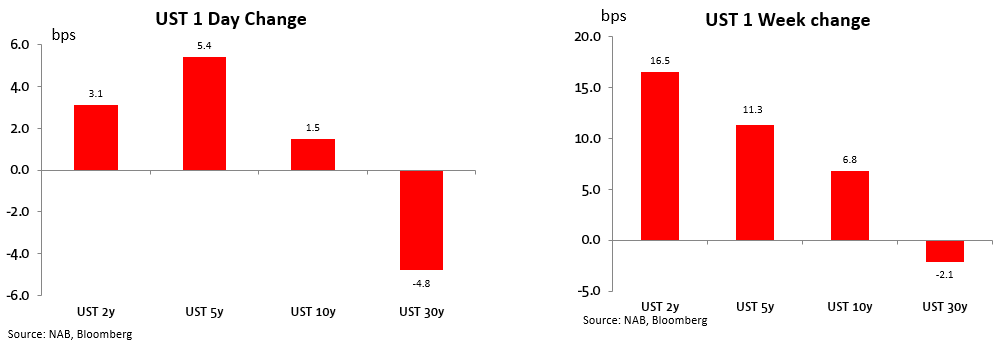

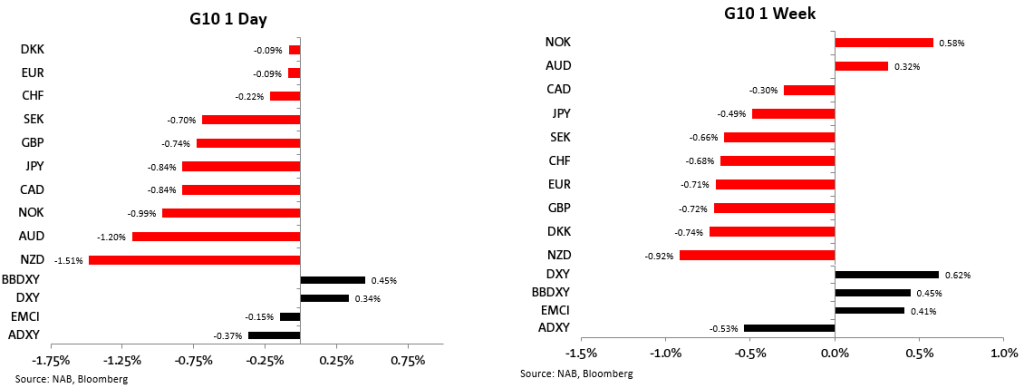

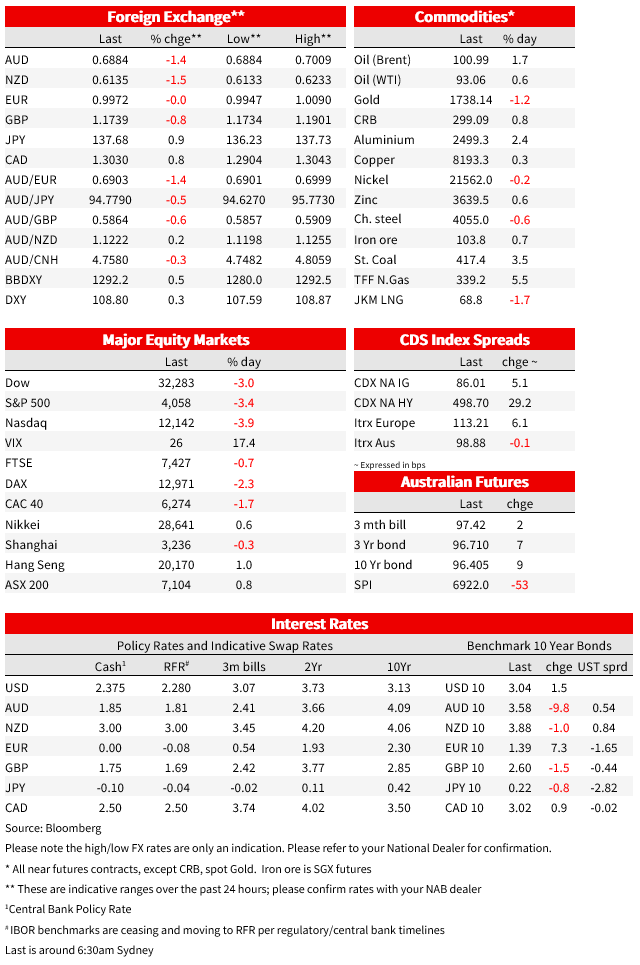

Fed chair Jay Powell’s address to the Kansas Fed’s Jackson Hole Symposium on Friday was short and as far as equity market investors were concerned, bitter not sweet. All three major US stock indices lost more than 3%, led by a 3.9% fall for the NASDAQ (S&P500 -3,4%). It was likely this, rather than what the Fed chair had to say, that limited the post-Powell back up in US Treasury yields to 3bps for 2s and just 1.5bps for the 10-year – albeit with a little bit of assist from incoming US economic data (notably PCE deflators 1/10% less than expected). The USD was stronger across the board, gains led by losses for the most growth sensitive/procyclical currencies, meaning AUD (-1.2%) and NZD (-1.5%). 50bps or 75bps from the Fed on 21 September is still up in the air (highly data dependent, would you believe?) but Jay Powell doesn’t think the Fed will be cutting rates in 2023. Meanwhile in Europe the clamour amongst ECB hawks for a 75bps hike on 8 September has begun.

Fed chair Powell’s Jackson Hole speech ran to less than 1,300 words (it fits on two pages of A4) and ran for no more than 8 minutes, prefaced by Powell saying, ‘My remarks will be shorter, my focus narrower, and my message more direct’ (than prior years). Restoring price stability ‘will take some time’ and ‘is likely to require a sustained period of below trend growth’ and which ‘will also bring some pain to households and businesses, Powell said. ‘But a failure to restore price stability would mean far greater pain’, he added.

After referencing the second successive 75bps rate increase in as many meetings, Powell said that ‘Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook’. Read that to mean that the decision will be between 50bps and 75bps. Markets were priced for 66.5bps of September tightening pre-Powell and finished on Friday virtually unchanged on that (66.9 bps). So still a toss-up. CPI on 13 September, just over a week before the FOMC, is going to be important (in which respect Powell described the lower July inflation readings as ‘welcome’).

There was forward guidance on sorts in the speech, via an implicit push-back against market pricing for rate cuts in 2023. Viz, ‘The historical record cautions strongly against prematurely loosening policy. Committee participants’ most recent individual projections from the June SEP showed the median federal funds rate running slightly below 4 percent through the end of 2023. Participants will update their projections at the September meeting’. (I can bet you they won’t, on average, be lower).

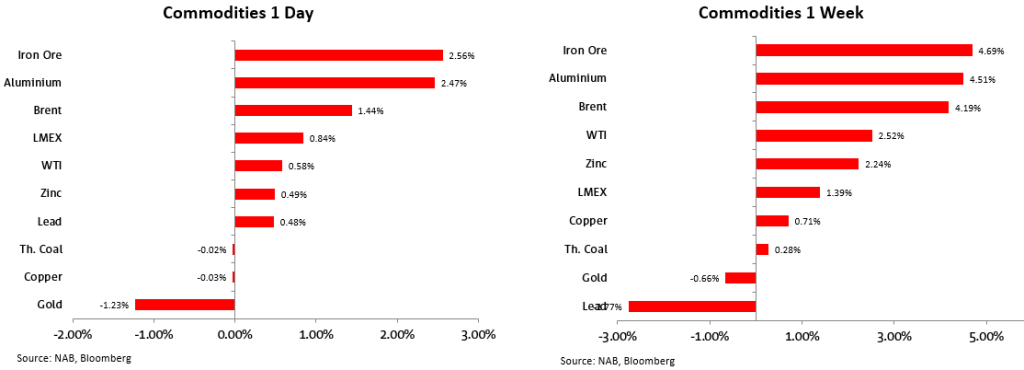

It was pretty much one way traffic down for equities post-Powell, the S&P500 falling from 4,200 to end just above 4,050. IT, the most interest rate sensitive sector, led the overall 3.4% decline (-4.3%) followed by consumer discretionaries (3.9%) with energy faring least bad (-1.1%) thanks to a modest rise in oil prices (Brent crude back above $100) and no letup in gas prices (the European TTF price was off just 3 euros from its prior day’s record high of EUR311 per megawatt hour).

Limited bond market moves post Powell’s doubtless says something about the market being well braced for hawkish commentary, though probably the only small-scale rises in yields across the curve also reflected the supportive influence of the subsequent sharp equity market sell-off (equity investors evidently hadn’t got the hawkish memo ahead of the event). Also at the margin, the bond market drew some support from a 1/10% downside surprise on the July PCE deflators (headline 6.3% from 6.8%, core 4.6% from 4.8%) and too a 1/10% drop in the final University of Michigan’s 5-10year inflation expectations reading, to 2.9% from 3.0%.

Incidentally, the final UoM Consumer Sentiment index came in at 58, well up on the 55.1 preliminary (that’s lower petrol prices for you) while Personal Income (0.2%) and Personal Spending (0.2%) were both a few tenths weaker than expected. Also on the good news side, the Advance July trade balance was almost $10bn smaller than expected at $89.1bn (consensus -$98.5bn) – a positive Q3 GDP contributor, in which respect the Atlanta Fed’s latest GDP Nowcast estimate is currently 1.6%, up from 1.4% prior to Friday’s data.

There was also market sensitive news out of Europe Friday, in particular a Reuters source story saying some ECB Governing Council members want to discuss a 75bps interest rate hike next month. Not to be outdone, Bloomberg ran a report a little later in the day saying some ECB officials want to begin a debate before year-end on quantitative tightening. No prizes for guessing which GC members might have been behind the Reuters report, with known GC hawks Knot and Holtzmann both out giving interviews on Friday saying 75bps should be on the table for discussion at the 8 September meeting. Money market moved from pricing 55bps worth of hikes at Thursday’s close to about 62.5bps Friday.

On top of this, at Jackson Hole ECB GC member Isabel Schnabel (also a known hawk) and Banque de France governor and fellow GC member Villeroy de Galhau, warned that a larger ‘sacrifice’ – in terms of weaker growth and lower job creation – will be needed to tame inflation than in previous bouts of monetary tightening and that price growth risks risks ‘spinning out of control’ if forceful action is ot taken. Villeroy take of the end to get raise rates beyond the neutral level – which he estimates at between 1% and 2% and that it could reach this level ‘before the end of the year’

The UK news of note was the energy price regulator, Ofgem, lifting the price cap on household gas prices to £3,549 from £1,971 per year – up 80% and about where it was expected to be set. On current methodologies, a further lift to ~£4,500 is to be expected next January. Current UK Chancellor Zahawi, speaking soon after the Ofgem news, said the higher cap will “cause stress and anxiety for many people, but help is coming,” pointing to the measures the government has confirmed. “While Putin is driving up energy prices in revenge for our support of Ukraine’s brave struggle for freedom, I am working flat out to develop options for further support,” he added, insisting the new PM will have the tools to “hit the ground running” and deliver support where needed”. Note the election process for the new Tory leader and hence Prime Minister ends on 5 September.

In FX, the USD drew across the board support from Powell’s messaging and the impact it had on risk asset performance more so than directly from the rates market, in which respect ex-gilts, European bond yield rose by much more than in the US (e.g., Bunds +7.3bps). In conjunction with the equity market sell-off, the VIX ended Friday at 25.6 up from 21.8, its highest since mid-July. The DXY USD index rose by 0.3% nd the broader BBDXY by 0.45% (thanks to its smaller EUR weight, EUR/USD drawing some support from the ECB news reports, down just 0.1% on the day). GBP fare much worse than the EUR (-0.7%) but it wa the pro-cyclical CAD (-0.8%) NOK (-1.0%) AUD (-1.2%) and NZD (1.50%) that bore the brunt of the equity market sell off and Powell’ messaging regarding a prolonged period of below trend US growth.

Having (very briefly) revisited levels above 7.00 either side of Powell (high of 0.7007) it finished the day and week just below 0.69 and on the lows of the day (0.6891). On the week, AUD/USD is the second best performing G10 currency after NOK, up 0.3%. In contrast, NZD took the G10 wooden spoon, -0.9% on the week and meaning AUD/NZD punched above 1.12, to its strongest since October 2017.

NAB Markets Research Disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.