Firmer consumer and steady outlook

Insight

UK best Eurozone on the PMI front in Thanksgiving- thinned markets

Events round-up

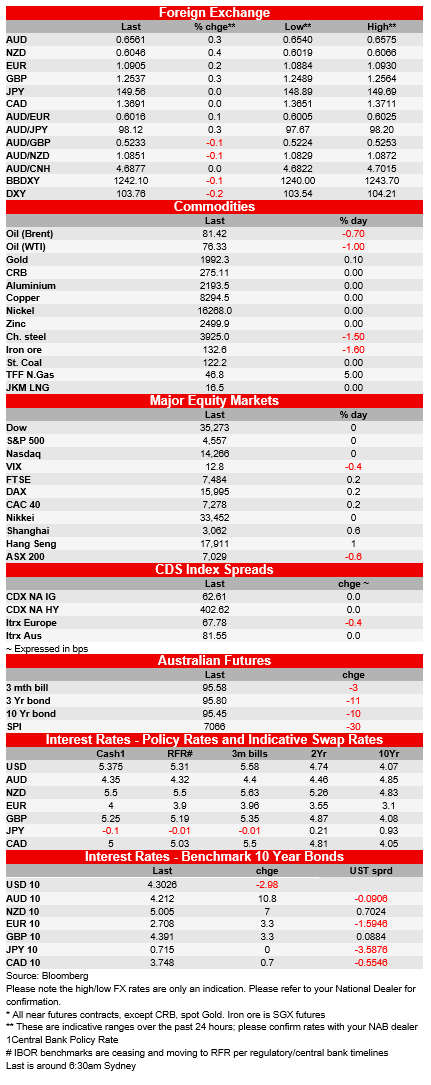

EZ Nov. Services PMI 48.2 from 47.8 vs 46.8 exp.

EZ Nov. Manufacturing PMI 43.8 from 43.1 vs 43.5 exp.

EZ Nov. Composite PMI 47.1 from 46.5 vs 46.8 exp.

Germany Nov. Services PMI 48.7 from 48.2 vs 48.5 exp.

Germany Nov. Manufacturing PMI 42.3 40.8 41.2 exp.

Germany Nov. Composite PMI 47.1 from 45.9 vs 46.3 exp.

France Nov. Services PMI 45.3 from 45.2 vs 45.5 exp.

France Nov. Manufacturing PMI 43.8 from 43.1 vs 43.5 exp.

France Nov. Composite PMI 44.5 from 44.6 vs 44.9 exp.

UK Nov. Services PMI 50.5 from 49.5 vs 49.5 exp.

UK Nov. Manufacturing PMI 46.7 from 44.8 vs 45.0 exp..

UK Nov. Composite PMI 50.1 from 48.7 vs 48.7 exp.

Predictably quiet overnight markets with the US out for Thanksgiving. The USD dollar is a touch softer led by small gains for the EUR and slightly bigger ones for the GBP, the latter following small beats versus consensus for its PMI data. German Bund yields (and the EUR) were higher following news of German government plans to suspend its so-called debt brake in order to circumvent the recent German Court ruling striking down planned off-budget spending (and borrowing). AUD is little changed on where we left it yesterday evening, while oil is off +/-!% ahead of the Hama-Israel temporary truce due to come into place at 7 am local time Friday.

Eurozone and UK PMIs were the main economic data draw last night, and where there were small unders (France) and over (Germany) and, for the Eurozone overall, a mild upside surprise on all readings (see full list above). Only the UK managed to print numbers above the 50 expansion/contraction line though, for both Services and the overall Composite reading. The latter had a more discernible (positive) impact on GBP than the former on the EUR, where EUR/USD fell a little on the French number, recovered off the Germany ones and then a couple of hours later was sharply unchanged on pre-PMI levels.

Of greater influence on Eurozone markets, Germany signalled that it would suspend the “debt brake” on government financing, following last week’s Constitutional Court ruling that it couldn’t use €60b earmarked to tackle the COVID19 pandemic into an off-budget fund to tackle climate change. The ruling also likely affects the use of other off-budget vehicles. The implication is that the government will be borrowing more money – but equally/more important for the economy, spending more money – and the prospect of more bond supply added upside pressure to German bond yields, which were already heading higher following the slightly stronger than expected PMI data. Germany’s 10-year rate is up 6bps to 2.62% while the UK 10-year rate is up 10bps to 4.26%. The US Treasuries market is closed but the 10-year future implies about a 4bps lift in yield to 4.44%. In stocks, European bourses finished the day mostly up +/-0.2%.

ECB October Meeting minutes note the Governing Council saw clear evidence that policy is working as intended but that most of the impact of past hikes had yet to materialize, while at the same time agreeing to keep open the option of another interest rate rise, recognising the need to avoid an unwarranted loosening of financial conditions. In this respect the Minutes noted the weakening EUR was a headwind in the fight against inflation – but which has since strengthened of course in the context of broad-based USD slippage. The main message, though, was to drive home its commitment to achieve 2% inflation which would require keeping rates at levels for sufficiently long duration. The minutes chime with the view rates are sufficiently high saying, “further hikes are not part of the current baseline scenario”. To this point the ECB’s Villeroy has been out in the last hour or so saying ‘The ECB won’t raise rates again, excluding surprises’. Nothing really new here.

Earlier the Riksbank kept rates on hold at 4%, which was in contrast to a Bloomberg poll of economists that had a hike to 4.25% pegged by 13 people against 8 for no change. The Riksbank nevertheless remains joined at the hip with other CB messaging, with governor Thedeen noting, “It is very clear we have not lost the chance to hike again…We will do that again if inflation does not go in the right direction toward 2%. That is a very clear message from us.”

Overall limited moves in currencies beyond the aforementioned GBP and EUR gains, though NZD sits at the top of the G10 leader board over the past 24 hours (+0.4%, 0.3% for GBP) while SEK sits at the bottom (-0.2%) after the Riksbank no-change. CAD is also a little lower as too NOK, consistent with the latest slippage in oil prices where WTI crude is down 86 cents and Brent 54 cents to 76.21 and 81.42 respectively. AUD/USD at 0.6560 is 0.2% up on this time yesterday.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.